China and Asia

Winners and losers in the great Chinese rebalancing

Slowing investment and resilient consumption in China are changing Asia’s economic order

Jul 26th 2014

JAMBI PROVINCE, INDONESIA

.

NEAR the centre of Sumatra, an Indonesian island once blanketed by forest, a gash in the ground reveals the wealth that lies just beneath its surface. Large yellow diggers prise out coal and tip it into 60-tonne lorries that huff their way to the top of the open-cast mine in Pauh subdistrict.

Five years of constant traffic, propelled by China’s hunger for fuel, has formed deep ruts in the dirt road. Recently, however, the lorries have stopped moving at midday. China’s appetite for coal has plateaued, the coal price has sagged and Minemex, the firm that operates the mine, has given workers longer lunch breaks, without pay. “We have no choice. We must endure,” sighs Demak, a sun-weathered 38-year-old.

Enduring might seem an apt word for Asian economies that had come to rely on ever-stronger exports to China. After averaging 10% annual growth for 30 years, the Chinese economy has managed only 7.5% over the past two years—enviable for most countries but a clear downshift for China. The lull has rippled through the region. Taiwanese machine-tool makers have seen exports to China fall by more than 20% since 2012.

Australian iron ore for delivery to China recently hit its lowest price in 21 months. Jewellery sales in Hong Kong have fallen by 40% this year, in part due to China’s crackdown on corruption.

But enduring is not the right word for all those doing business with China. Analysts refer to milk as New Zealand’s “white gold”, such is China’s thirst for it. The number of Chinese visitors to Sri Lanka more than doubled in the first half of the year. Chinese women in their 30s are now the biggest group of foreign buyers on the website of Lotte, a big South Korean retailer, snapping up cosmetics.

These contrasting fortunes stem from profound, if gradual, changes to Chinese growth. Consumption is at last edging out investment as the economy’s main engine.

Household consumption has been inching up of late as a proportion of GDP, rising from 34.9% in 2010 to 36.2% last year, according to official data. Some economists think the true share could be ten percentage points higher. This year even with the government’s “mini-stimulus”—a burst of spending on railways and public housing unveiled in April—consumption has still accounted for over half of Chinese growth.

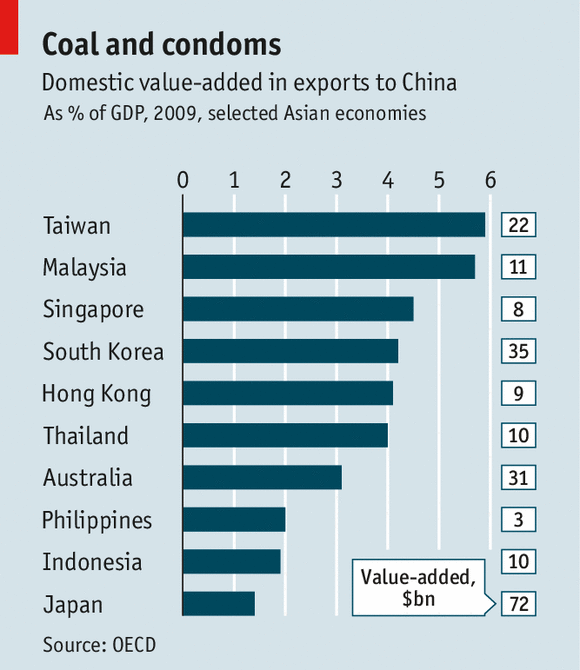

Limited though it has been, this rebalancing is beginning to make itself felt beyond China’s borders. First, there is the question of what China buys. With $1.95 trillion in imports in 2013, it is the world’s second-biggest importing nation, behind only America (although almost half of those imports are parts that are assembled and re-exported). Taiwan is more exposed to China’s appetites than any other Asian economy, with sales to China constituting about 6% of its GDP (see chart). But many of its exports, such as mobile phones, are geared towards consumption rather than investment. These are still faring well: Taiwan’s export orders to China were up by 15% in June from a year earlier.

More at risk are those that mainly export commodities and capital goods such as heavy machinery to China. The most exposed is Australia, which could lose about 0.8 percentage points of growth if Chinese investment slows to a crawl, according to Capital Economics, a consulting firm. That has not yet happened, but the fading of Australia’s mining boom has sent unemployment to a decade-high of 6%, hinting at its vulnerability.

Even those countries that do not export much to China will feel the effects of its rebalancing via commodity markets. More tepid Chinese demand means lower prices for many raw materials: witness the nearly 50% fall in Indonesian coal prices since 2011.

Compounding the impact of China’s slowdown are government measures to steer power companies away from the cheapest, most-polluting coal, like that found in Pauh. “You can’t make money mining that coal anymore unless you’re located next to the coastline where you can bring it to ships,” says Gatut Adisoma of the Indonesian Coal Mining Association.

But it is not all gloom for commodities. Metals that are used mainly in consumer goods, such as zinc, much of which goes into cars, are outpacing those tied to China’s old growth model such as iron ore, the precursor to all the steel in China’s vast housing developments. And the pain of commodity producers spells relief for their customers. Most Asian economies from South Korea to Thailand are big importers of metals and energy. If Narendra Modi, India’s prime minister, is to kick-start spending on infrastructure, weaker investment in China forms a propitious backdrop.

Across the Strait of Malacca from the coalmines of Pauh, Karex, a Malaysian firm that is the world’s biggest producer of condoms, has been boosted both by the shifting composition of China’s imports and by the resulting movement in commodity prices. Condom use tends to track consumption more broadly, growing along with urbanisation, income and education, as well as leisure time. Chinese condom imports almost tripled from 2007 to 2013, to 3.4m kg. Meanwhile, the price of their main ingredient, rubber, has nearly halved since 2011 thanks to plunging demand for supersized tyres from the mining and construction industries. As whirring glass tubes dip into latex baths, Goh Miah Kiat, Karex’s CEO, expresses optimism about China, currently just a tenth or so of its sales. “There’s a perception that imports are better than local products,” he says. From condoms to milk and cars, it is a bias that augurs well for countries that make what Chinese shoppers want to buy.

NEAR the centre of Sumatra, an Indonesian island once blanketed by forest, a gash in the ground reveals the wealth that lies just beneath its surface. Large yellow diggers prise out coal and tip it into 60-tonne lorries that huff their way to the top of the open-cast mine in Pauh subdistrict.

Five years of constant traffic, propelled by China’s hunger for fuel, has formed deep ruts in the dirt road. Recently, however, the lorries have stopped moving at midday. China’s appetite for coal has plateaued, the coal price has sagged and Minemex, the firm that operates the mine, has given workers longer lunch breaks, without pay. “We have no choice. We must endure,” sighs Demak, a sun-weathered 38-year-old.

Enduring might seem an apt word for Asian economies that had come to rely on ever-stronger exports to China. After averaging 10% annual growth for 30 years, the Chinese economy has managed only 7.5% over the past two years—enviable for most countries but a clear downshift for China. The lull has rippled through the region. Taiwanese machine-tool makers have seen exports to China fall by more than 20% since 2012.

Australian iron ore for delivery to China recently hit its lowest price in 21 months. Jewellery sales in Hong Kong have fallen by 40% this year, in part due to China’s crackdown on corruption.

But enduring is not the right word for all those doing business with China. Analysts refer to milk as New Zealand’s “white gold”, such is China’s thirst for it. The number of Chinese visitors to Sri Lanka more than doubled in the first half of the year. Chinese women in their 30s are now the biggest group of foreign buyers on the website of Lotte, a big South Korean retailer, snapping up cosmetics.

These contrasting fortunes stem from profound, if gradual, changes to Chinese growth. Consumption is at last edging out investment as the economy’s main engine.

Household consumption has been inching up of late as a proportion of GDP, rising from 34.9% in 2010 to 36.2% last year, according to official data. Some economists think the true share could be ten percentage points higher. This year even with the government’s “mini-stimulus”—a burst of spending on railways and public housing unveiled in April—consumption has still accounted for over half of Chinese growth.

Limited though it has been, this rebalancing is beginning to make itself felt beyond China’s borders. First, there is the question of what China buys. With $1.95 trillion in imports in 2013, it is the world’s second-biggest importing nation, behind only America (although almost half of those imports are parts that are assembled and re-exported). Taiwan is more exposed to China’s appetites than any other Asian economy, with sales to China constituting about 6% of its GDP (see chart). But many of its exports, such as mobile phones, are geared towards consumption rather than investment. These are still faring well: Taiwan’s export orders to China were up by 15% in June from a year earlier.

More at risk are those that mainly export commodities and capital goods such as heavy machinery to China. The most exposed is Australia, which could lose about 0.8 percentage points of growth if Chinese investment slows to a crawl, according to Capital Economics, a consulting firm. That has not yet happened, but the fading of Australia’s mining boom has sent unemployment to a decade-high of 6%, hinting at its vulnerability.

Even those countries that do not export much to China will feel the effects of its rebalancing via commodity markets. More tepid Chinese demand means lower prices for many raw materials: witness the nearly 50% fall in Indonesian coal prices since 2011.

Compounding the impact of China’s slowdown are government measures to steer power companies away from the cheapest, most-polluting coal, like that found in Pauh. “You can’t make money mining that coal anymore unless you’re located next to the coastline where you can bring it to ships,” says Gatut Adisoma of the Indonesian Coal Mining Association.

But it is not all gloom for commodities. Metals that are used mainly in consumer goods, such as zinc, much of which goes into cars, are outpacing those tied to China’s old growth model such as iron ore, the precursor to all the steel in China’s vast housing developments. And the pain of commodity producers spells relief for their customers. Most Asian economies from South Korea to Thailand are big importers of metals and energy. If Narendra Modi, India’s prime minister, is to kick-start spending on infrastructure, weaker investment in China forms a propitious backdrop.

Across the Strait of Malacca from the coalmines of Pauh, Karex, a Malaysian firm that is the world’s biggest producer of condoms, has been boosted both by the shifting composition of China’s imports and by the resulting movement in commodity prices. Condom use tends to track consumption more broadly, growing along with urbanisation, income and education, as well as leisure time. Chinese condom imports almost tripled from 2007 to 2013, to 3.4m kg. Meanwhile, the price of their main ingredient, rubber, has nearly halved since 2011 thanks to plunging demand for supersized tyres from the mining and construction industries. As whirring glass tubes dip into latex baths, Goh Miah Kiat, Karex’s CEO, expresses optimism about China, currently just a tenth or so of its sales. “There’s a perception that imports are better than local products,” he says. From condoms to milk and cars, it is a bias that augurs well for countries that make what Chinese shoppers want to buy.

0 comments:

Publicar un comentario