Why have governments funded in the past?

Andrew Smithers

Jul 11 08:45

While it is sometimes useful to make a distinction between treasuries and central banks, they are fundamentally both part of government. When central banks buy bonds as part of quantitative easing, governments are in practice ceasing to fund, ie, they are issuing short-term rather than long-term debt. If this is potentially harmful, we need to worry; if not, we need to ask why have governments funded in the past?

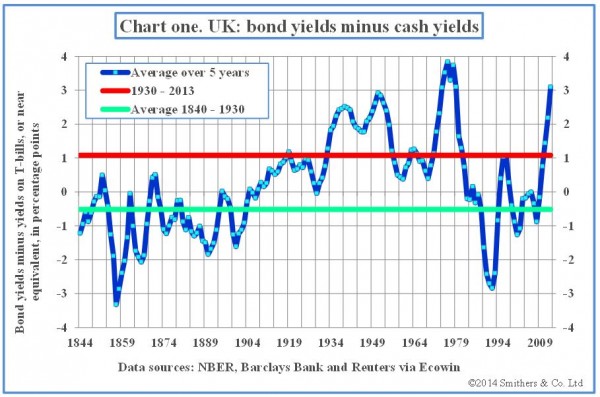

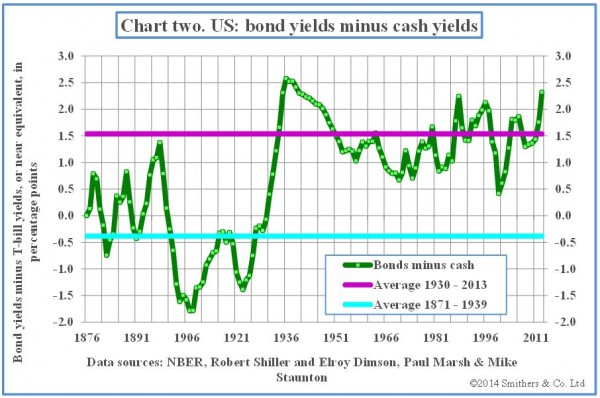

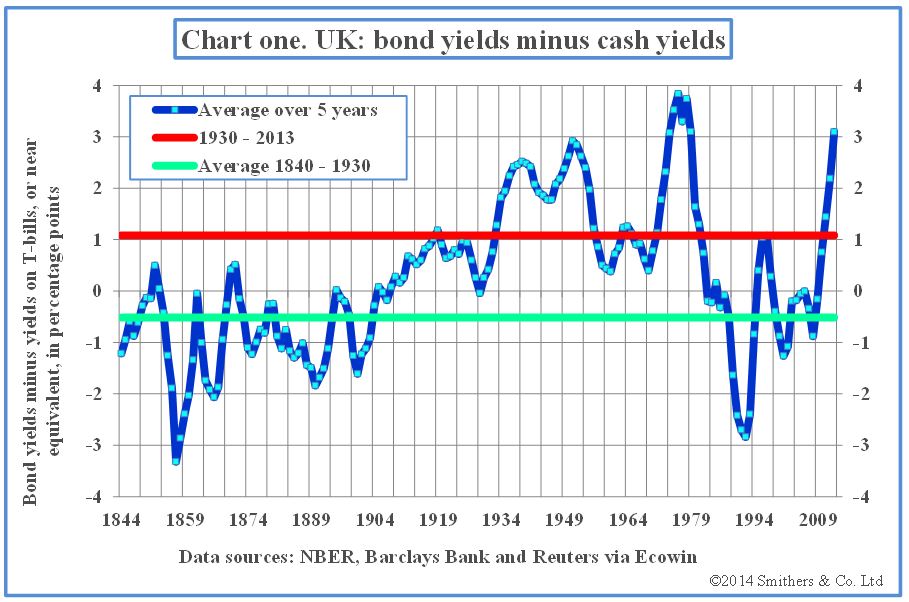

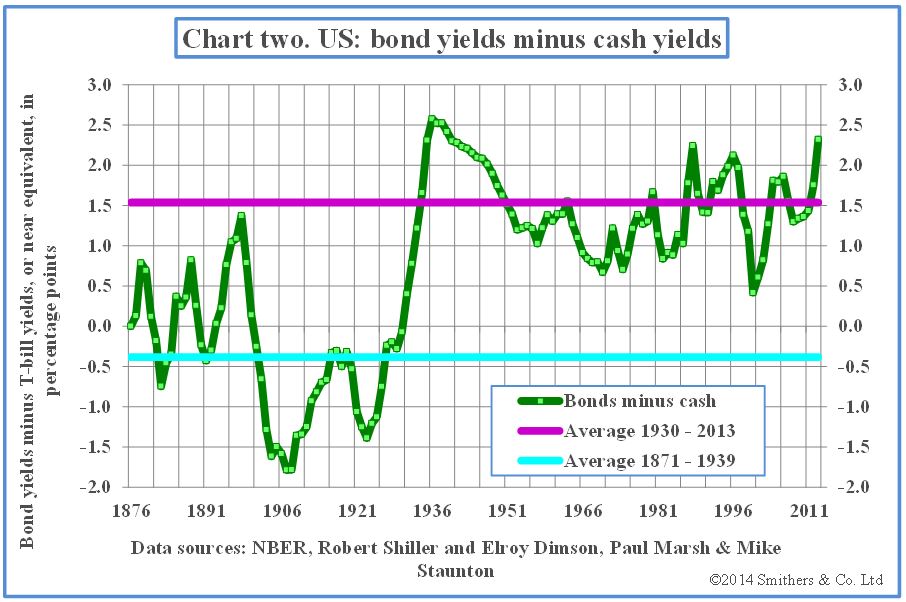

If governments’ sole concern were to raise money as cheaply as possible, they would have funded in the 19th and early 20th centuries, but not for the past 80 years. Chart one (above) shows this for the UK and chart two (below) for the US.

In the 19th century long bonds yielded less than Treasury bills, ie, there was usually a downward sloping yield curve. Today it seems universally accepted that the yield curve will slope upward on a permanent basis.

I see the change in the slope of the yield curve as the rational response of investors to a rise in the likelihood and uncertainty of inflation. If inflation is not expected over the life of a bond, then investors will quite reasonably sacrifice some income for the sake of its greater stability. Despite what is typically taught in finance courses, risk is not well captured by the short-term volatility of total returns. The capital values of bonds are more volatile than those of cash and their income less so. If an investor likes to have a steady income and is unworried by short-term fluctuations in the price of an asset he does not expect to sell, cash is more risky than bonds because the income from it varies.

Bonds are not therefore inherently more risky than short-term deposits and they do not therefore need to produce higher returns. They are, however, more risky when inflation has become uncertain.

We are unlikely to move quickly to a world in which we can rely on inflation being stable. Governments are therefore likely to save money if they do not fund.

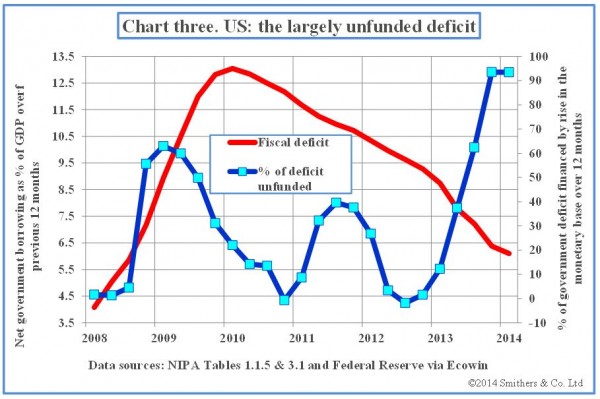

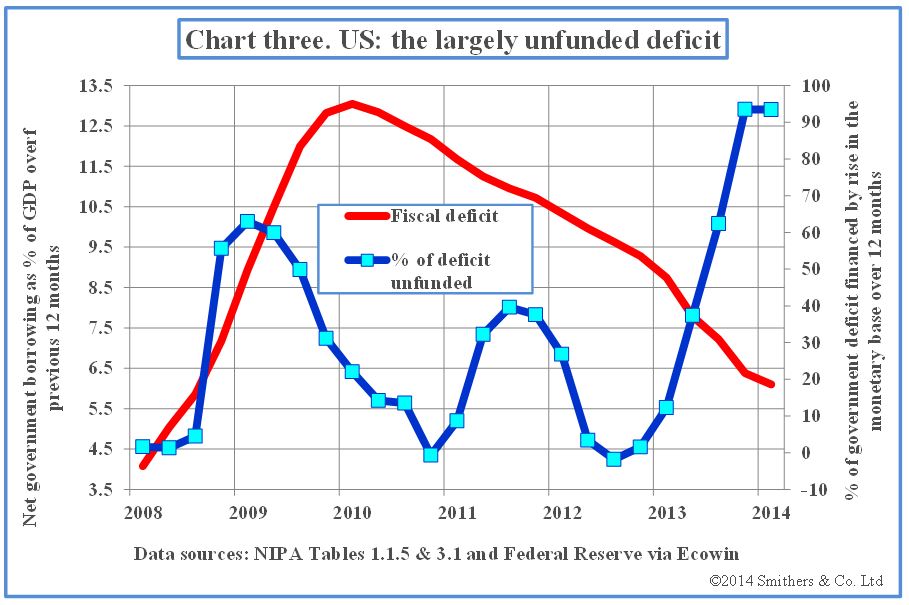

It is of course possible, and in my view likely, that funding involves other issues than just the cost of borrowing. Failing to fund may be risky for the economy. Chart three (above) shows that, if underfunding is risky, then the risks would seem to be growing rapidly. The deficit has fallen from 11 per cent to 6 per cent of gross domestic product while QE has expanded. Over the past 12 months the expansion of the US Federal Reserve’s balance sheet has covered more than 90 per cent of the deficit.

If underfunding does not pose risks for the economy, bond markets are presumably doomed to extinction. If it does, the nature and scale of those risks is clearly very important. I think most readers will share my view that the demise of the bond market is unlikely. It follows that there is widespread agreement that avoiding the risks of underfunding is, normally at least, sufficiently important to make the additional costs of doing so worthwhile. I therefore plan to write soon about the dangers that have arisen as a result of QE.

If governments’ sole concern were to raise money as cheaply as possible, they would have funded in the 19th and early 20th centuries, but not for the past 80 years. Chart one (above) shows this for the UK and chart two (below) for the US.

In the 19th century long bonds yielded less than Treasury bills, ie, there was usually a downward sloping yield curve. Today it seems universally accepted that the yield curve will slope upward on a permanent basis.

I see the change in the slope of the yield curve as the rational response of investors to a rise in the likelihood and uncertainty of inflation. If inflation is not expected over the life of a bond, then investors will quite reasonably sacrifice some income for the sake of its greater stability. Despite what is typically taught in finance courses, risk is not well captured by the short-term volatility of total returns. The capital values of bonds are more volatile than those of cash and their income less so. If an investor likes to have a steady income and is unworried by short-term fluctuations in the price of an asset he does not expect to sell, cash is more risky than bonds because the income from it varies.

Bonds are not therefore inherently more risky than short-term deposits and they do not therefore need to produce higher returns. They are, however, more risky when inflation has become uncertain.

We are unlikely to move quickly to a world in which we can rely on inflation being stable. Governments are therefore likely to save money if they do not fund.

It is of course possible, and in my view likely, that funding involves other issues than just the cost of borrowing. Failing to fund may be risky for the economy. Chart three (above) shows that, if underfunding is risky, then the risks would seem to be growing rapidly. The deficit has fallen from 11 per cent to 6 per cent of gross domestic product while QE has expanded. Over the past 12 months the expansion of the US Federal Reserve’s balance sheet has covered more than 90 per cent of the deficit.

If underfunding does not pose risks for the economy, bond markets are presumably doomed to extinction. If it does, the nature and scale of those risks is clearly very important. I think most readers will share my view that the demise of the bond market is unlikely. It follows that there is widespread agreement that avoiding the risks of underfunding is, normally at least, sufficiently important to make the additional costs of doing so worthwhile. I therefore plan to write soon about the dangers that have arisen as a result of QE.

0 comments:

Publicar un comentario