Will Yellen follow Carney’s hawkish surprise?

Gavyn Davies

Jun 15 11:40

Mark Carney delivered a substantial hawkish surprise to the markets in his Mansion House speech on Thursday. After appearing to be a convinced dove ever since he became BoE Governor in July 2013, he now says that the first UK interest rate rise could come “sooner than expected”, with the decision on the timing of the first rise “becoming more balanced”. Market expectations of forward short rates in 2015 immediately jumped by 20 basis points.

Although the Governor is still talking about a very gradual rise in UK rates, he appeared to have changed the dovish tone of the forward guidance given by the BoE last year. This has made investors nervous, with many asking whether Fed Chair Janet Yellen may do the same in her press conference on Wednesday.

This seems unlikely, because the US economic recovery is still lagging that in the UK. Nevertheless, the parameters within which investors view forward guidance, including the Fed’s “dots” showing the future path for interest rates, may have been somewhat shaken.

The BoE will no doubt argue that they never gave the markets any cast iron reason to believe that the first rate rise would be delayed far into 2015 or 2016. “When conditions change, I change my mind”, was the gist of what Mr Carney said at the Mansion House. But the central banks do seem to want it both ways: the main point of forward guidance, according to many economists, was to pre-commit to policies that would not change when conditions changed.

Everyone knew all along that forward guidance suffered from a serious problem of time inconsistency. What was convenient for the BoE and the Fed to say when they were at their most dovish in 2012/13 may not be convenient to deliver when the situation has changed in 2015/16. The BoE has now reminded the markets that the fine print in forward guidance needs to be read very carefully indeed.

What are the similarities, and the differences, between the UK and US situations?

Differences between the US and UK

At first blush, the differences look to be dominant. The rate of expansion in economic activity suddenly surged in the UK about a year ago, and the Fulcrum “nowcasts” have been consistently showing UK activity growth in the 4-5 per cent region ever since then. In the most recent Inflation Report, the Bank said that it expected the growth rate to slow in the imminent future, but this has certainly not happened. If anything, the reverse is occurring.

In the US, meanwhile, official data for real GDP growth actually turned negative in 2014 Q1, and growth in the first half of the year has remained well below trend. US “nowcasts” have been somewhat firmer than the official GDP data, touching 4 per cent in the last few weeks, but the Fed is unlikely to be very impressed by such a short-term shift after such a long period of below-trend growth. There is a possibility that the sudden catch-up in spending on consumer durables and housing, which has driven the UK recovery, might one day be a relevant lesson for the US, but it has not happened yet.

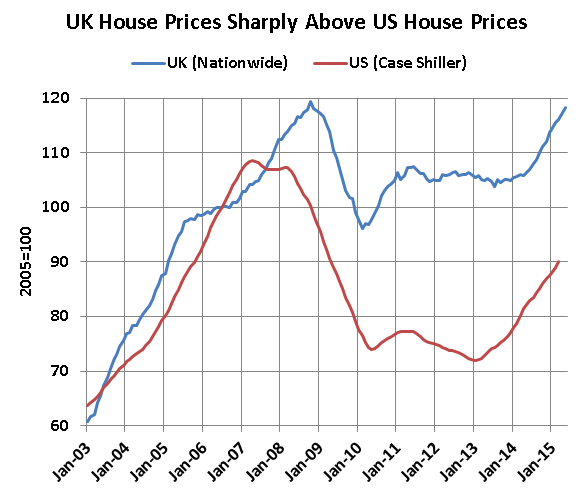

Nor is the behaviour of housing very similar between the two economies. The recent strength of the UK housing market, which is “showing the potential to overheat” according to Mark Carney, has left the level of prices far higher in Britain than in America. Only recently, Chair Yellen has expressed concerns that the US housing market might be too weak, not too strong. And she does not seem at all troubled by signs of bubbles in other asset prices either.

So should we simply forget about the UK example when thinking about Fed policy? There are three reasons why there might be some relevance in the comparison.

Similarities

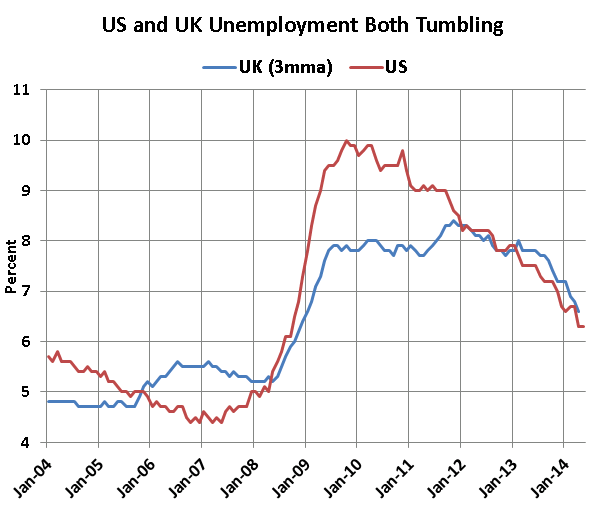

First, the unemployment rate is falling markedly in both countries, while inflation is only a little below the 2 per cent target. Wages remain subdued but, according to Bruce Kasman at J.P. Morgan, a standard Taylor Rule would suggest that interest rates in both countries should be 200 basis points higher by the end of this year. In the minds of the hawks on both sides of the Atlantic, this is beginning to undermine the “lower for longer” forward guidance offered last year.

The second reason relates to the supply side. In the UK, the BoE has said repeatedly that it expects labour productivity growth to bounce back as the economy recovers, thus allowing the productive capacity of the economy to expand alongside demand. This has not happened so far, and it is one of the key reasons why several members of the MPC are clearly getting jumpy.

In the US, the equivalent issue is the puzzle about labour force participation. Chair Yellen has been very clear that she believes that a significant proportion of the decline in participation will be reversed if the economic expansion is maintained, but recent data have shown no sign whatsoever that this is happening. If not Ms Yellen herself, then several other members of the FOMC are likely to start worrying about this before too long. In fact, James Bullard has already led the way on this.

The third reason relates to the way the markets might view the risks surrounding the Fed’s decisions. Even if the controlling members on the FOMC remain inclined towards dovishness, as they almost certainly do, there must be a risk that they will change their minds in response to incoming economic data, in the same way that the BoE has done.

There is no risk premium protecting against this possibility built into the path for US forward short rates. In fact, following the bond rally that has occurred this year, the market seems vulnerable to a sudden re-assessment of the Fed’s basic dovishness, just as it was before the taper tantrum last year.

Conclusion

I do not expect these similarities to become apparent at the FOMC meeting and the press conference this week. The committee is still in the phoney war phase (or perhaps it should be called the phoney peace), in which tapering is continuing along a pre-ordained path, almost regardless of economic events.

That will not change until tapering ends in October. After that, the hawkish surprise administered by the BoE last week might become a great deal more relevant for Fed watchers.

Although the Governor is still talking about a very gradual rise in UK rates, he appeared to have changed the dovish tone of the forward guidance given by the BoE last year. This has made investors nervous, with many asking whether Fed Chair Janet Yellen may do the same in her press conference on Wednesday.

This seems unlikely, because the US economic recovery is still lagging that in the UK. Nevertheless, the parameters within which investors view forward guidance, including the Fed’s “dots” showing the future path for interest rates, may have been somewhat shaken.

The BoE will no doubt argue that they never gave the markets any cast iron reason to believe that the first rate rise would be delayed far into 2015 or 2016. “When conditions change, I change my mind”, was the gist of what Mr Carney said at the Mansion House. But the central banks do seem to want it both ways: the main point of forward guidance, according to many economists, was to pre-commit to policies that would not change when conditions changed.

Everyone knew all along that forward guidance suffered from a serious problem of time inconsistency. What was convenient for the BoE and the Fed to say when they were at their most dovish in 2012/13 may not be convenient to deliver when the situation has changed in 2015/16. The BoE has now reminded the markets that the fine print in forward guidance needs to be read very carefully indeed.

What are the similarities, and the differences, between the UK and US situations?

Differences between the US and UK

At first blush, the differences look to be dominant. The rate of expansion in economic activity suddenly surged in the UK about a year ago, and the Fulcrum “nowcasts” have been consistently showing UK activity growth in the 4-5 per cent region ever since then. In the most recent Inflation Report, the Bank said that it expected the growth rate to slow in the imminent future, but this has certainly not happened. If anything, the reverse is occurring.

In the US, meanwhile, official data for real GDP growth actually turned negative in 2014 Q1, and growth in the first half of the year has remained well below trend. US “nowcasts” have been somewhat firmer than the official GDP data, touching 4 per cent in the last few weeks, but the Fed is unlikely to be very impressed by such a short-term shift after such a long period of below-trend growth. There is a possibility that the sudden catch-up in spending on consumer durables and housing, which has driven the UK recovery, might one day be a relevant lesson for the US, but it has not happened yet.

Nor is the behaviour of housing very similar between the two economies. The recent strength of the UK housing market, which is “showing the potential to overheat” according to Mark Carney, has left the level of prices far higher in Britain than in America. Only recently, Chair Yellen has expressed concerns that the US housing market might be too weak, not too strong. And she does not seem at all troubled by signs of bubbles in other asset prices either.

So should we simply forget about the UK example when thinking about Fed policy? There are three reasons why there might be some relevance in the comparison.

Similarities

First, the unemployment rate is falling markedly in both countries, while inflation is only a little below the 2 per cent target. Wages remain subdued but, according to Bruce Kasman at J.P. Morgan, a standard Taylor Rule would suggest that interest rates in both countries should be 200 basis points higher by the end of this year. In the minds of the hawks on both sides of the Atlantic, this is beginning to undermine the “lower for longer” forward guidance offered last year.

The second reason relates to the supply side. In the UK, the BoE has said repeatedly that it expects labour productivity growth to bounce back as the economy recovers, thus allowing the productive capacity of the economy to expand alongside demand. This has not happened so far, and it is one of the key reasons why several members of the MPC are clearly getting jumpy.

In the US, the equivalent issue is the puzzle about labour force participation. Chair Yellen has been very clear that she believes that a significant proportion of the decline in participation will be reversed if the economic expansion is maintained, but recent data have shown no sign whatsoever that this is happening. If not Ms Yellen herself, then several other members of the FOMC are likely to start worrying about this before too long. In fact, James Bullard has already led the way on this.

The third reason relates to the way the markets might view the risks surrounding the Fed’s decisions. Even if the controlling members on the FOMC remain inclined towards dovishness, as they almost certainly do, there must be a risk that they will change their minds in response to incoming economic data, in the same way that the BoE has done.

There is no risk premium protecting against this possibility built into the path for US forward short rates. In fact, following the bond rally that has occurred this year, the market seems vulnerable to a sudden re-assessment of the Fed’s basic dovishness, just as it was before the taper tantrum last year.

Conclusion

I do not expect these similarities to become apparent at the FOMC meeting and the press conference this week. The committee is still in the phoney war phase (or perhaps it should be called the phoney peace), in which tapering is continuing along a pre-ordained path, almost regardless of economic events.

That will not change until tapering ends in October. After that, the hawkish surprise administered by the BoE last week might become a great deal more relevant for Fed watchers.

0 comments:

Publicar un comentario