How serious is China’s property slump?

Gavyn Davies

Jun 01 16:26

Fears of a crash in the Chinese property market are widespread in the financial markets. That is nothing new. The domestic real estate sector has been growing at breakneck speed ever since private property ownership was first permitted in 1998, and on several occasions, most recently in 2012, there have been dire warnings from western investors that housing supply was far outstripping demand.

An easing in monetary policy headed off a hard landing two years ago, but this may only have delayed the inevitable. The renewed correction in the market in mid 2013, which now seems to be gathering momentum, is certainly the main downside risk in the global economy in 2014.

Following the devastating global impact of the US property crash of 2005-08, it is little wonder that investors are paranoid that China might be treading the same path. But there are many differences between the US then and China now. The US housing crash was transformed into something far more serious by excesses in the financial sector, and by adverse wealth effects on consumer spending.

Even though China has also built up severe credit excesses in its shadow banking sector, it is hard to make the macro arithmetic add up to a shock comparable in size to the 2008 US/global meltdown.

(Apologies for greater length than usual in this blog – skip to “GDP effects” for the bottom line.)

Overbuilding

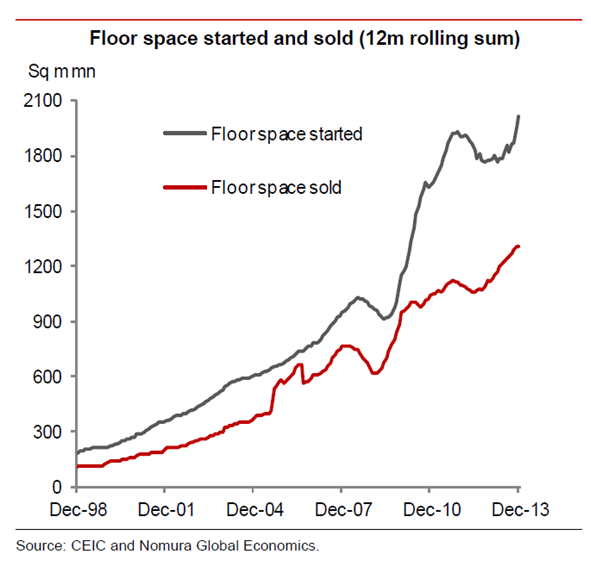

The problem in the Chinese real estate sector can be summarised in one word: overbuilding. Until 2011, construction struggled to keep pace with the demand for new housing caused by China’s rapid urbanisation. House prices rose rapidly, providing households with the best performing asset available to them. This encouraged speculative purchases, increasingly financed by the shadow banking sector. China’s infamous ghost cities were the result. Goldman Sachs estimates that there is now significant over-supply of housing in 30 of the largest 200 cities in China.

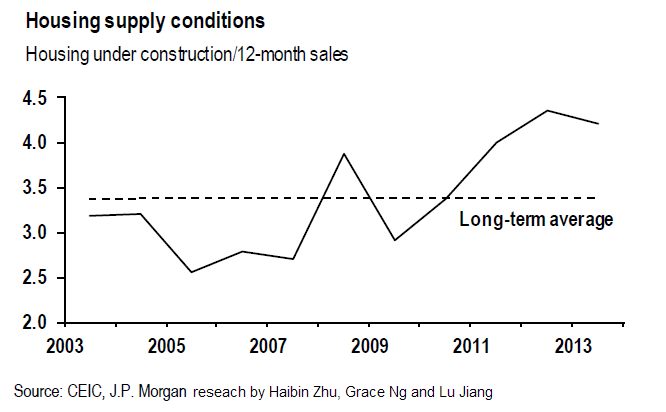

All the available measures of housing supply indicate that it continues vastly to outstrip demand, especially in the stressed end of Tier 2 cities, and to a lesser extent in Tiers 3 and 4. In many of these cities, the already-completed floor space available for sale is equivalent to 3 years of sales at the current rate. Add in floor space now under construction, and current supply across the whole nation is equal to more than four years of normal sales.

Housing starts have fallen by 24.5 per cent in the last 12 months as construction firms have responded to excess supply, and to the tightening of credit conditions that was deliberately imposed by the new administration in 2013.

This drop in construction explains all of the recent slowdown in real GDP growth, from 7.9 per cent in 2012 Q4 to 7.4 per cent now. Furthermore, the latest housing figures suggest that the supply/demand imbalance continues to build, with current construction of new floor space still in excess of new sales, and unsold inventory therefore rising further.

House prices have slowed sharply in response to excess supply, but there is clearly much further to go before equilibrium is restored. J.P. Morgan says that house prices will decline by 2 per cent next year, the first time they have moved into negative territory in modern China. There is clearly a risk that speculative home owners will panic, dumping more empty property onto the market. If so, a severe crash in house prices could ensue, leading to negative wealth effects and a major setback to consumer confidence.

While this is certainly conceivable, it still does not seem to be the most likely scenario. Several factors should protect China from the worst case outcome.

Mitigating Factors

Although there have certainly been speculative purchases in recent years, the demand for housing is fundamentally driven by a combination of urbanisation and real income growth in the employed labour force. The shift of the population into the cities has been running at about 1.5 percentage points of the population per annum for two decades, and there has been no slackening yet in this pace of demographic change.

Furthermore, household incomes in the cities continue to rise at close to 10 per cent per annum. The demand for new housing units as households upgrade the standard of their accommodation is huge, at around 5-6 million units a year, which is half of all demand for new houses.

In a more static labour market, such as that in the US in 2005, a period of speculative overbuilding can take many years to eradicate, even if new building declines by half, which is what actually happened in America. The much more dynamic Chinese labour market should result in housing demand that eradicates over supply more rapidly, and with a smaller decline in the pace of new building.

There is scope for policy makers to soften the landing by easing controls over property demand, and that is already happening. Premier Li Keqiang said last week that policy would be fine-tuned if necessary, and this was followed by a cut in reserve requirement ratios for some banks on Friday. There is plenty of room for further cuts in reserve requirements, and for other fiscal and regulatory measures to boost construction.

Although this would slow down the necessary rebalancing of the economy, the authorities would certainly prefer this scenario to a hard landing, given the unpalatable economic and social consequences that would bring.

GDP Effects

Housebuilding, real estate and related sectors accounted for 16 per cent of GDP in 2013. Mainstream economic forecasters seem to be expecting a drop in construction of several percentage points, replicating the experience of earlier slowdowns. A drop of this scale would directly reduce the level of real GDP by only about 0.5 -1.0 per cent. Some economists (eg Qu Hongbin at HSBC) talk of a downside scenario in which GDP might fall by about 2 per cent, but they generally add that this could be substantially offset by policy easing.

While these may be sensible central forecasts, there is clearly a rising probability of a harder landing, given the current imbalance in the market. The lesson from the US crash is that in a downside case the impact of a property crash can be much greater than predicted in advance by mainstream forecasters.

How bad might this be? No-one can be sure, but if we assume for illustration that construction/real estate output in China falls by 25 per cent compared to previous trends over three years, which is roughly half of the decline experienced by overall construction in the US collapse, the total hit to Chinese GDP would be 4 per cent, thus reducing the annual growth rate by 1.3 per cent for three years.

This does not allow for any knock on effects on consumer spending, nor for any collapse in the financial sector. Neither of these effects are likely to be very large. Unlike in the US case, equity withdrawal from the housing market is not permitted in China, so the boost to consumer spending has been much smaller. And Chinese households are required to provide at least 30 per cent equity in any home purchase, so the chances of negative equity and bad debts should be much less than in the US crash.

Shadow Banking

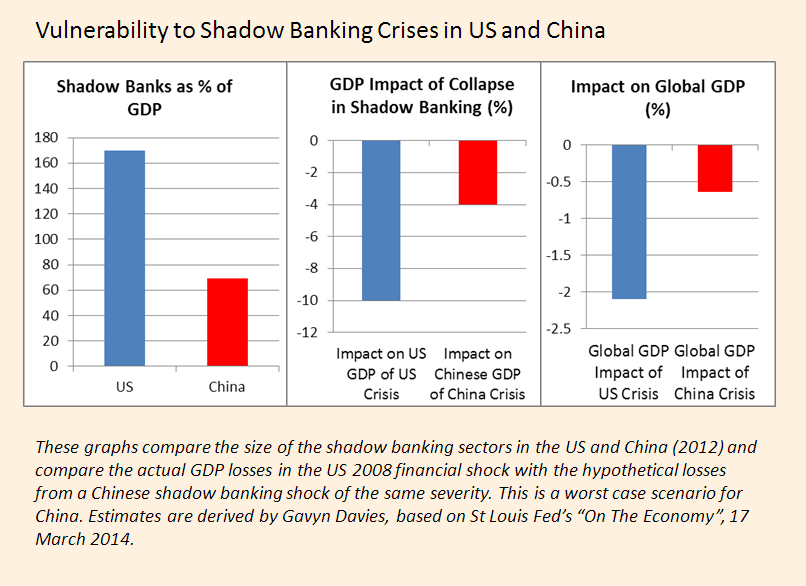

A collapse in the shadow banking sector cannot be ruled out, given the extent of its recent expansion.

The St Louis Fed’s economic blog recently estimated the worst case effects of a collapse in the Chinese shadow banking sector by comparing it directly with the US example. They point out that shadow banking in China is less than half as large as it is in the US, so even if the collapse were as painful in the US case, and the economic effects were as bad, the impact on Chinese GDP would be “only” about 4 per cent. This would probably be spread over several years and would directly reduce global GDP by about 0.6 per cent in total.

Conclusion

These worst case effects, at 4 per cent of Chinese GDP, spread over three years, are certainly not negligible. Admittedly, they are little more than stabs in the dark, and the uncertainty is enormous. But they are not of the same scale as the Great Financial Crash.

And, given the increasingly obvious intention of the Chinese authorities to ease policy further, they are far from inevitable.

0 comments:

Publicar un comentario