The future for real interest rates

by Gavyn Davies

April 6, 2014 11:25 am

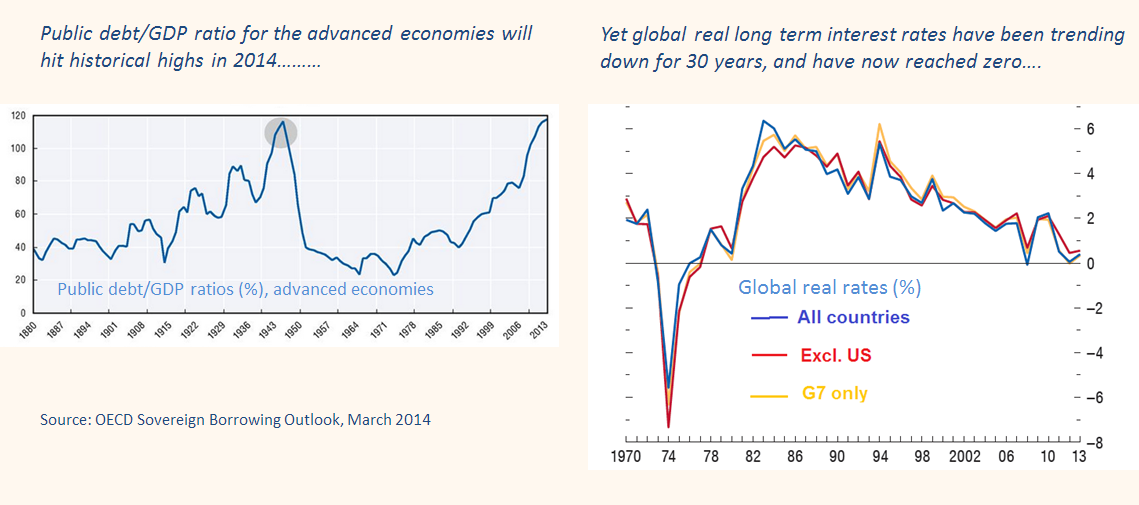

The OECD pointed out last week that the ratio of public debt/GDP will reach all time historic highs in 2014, at about 120 per cent. Taken in isolation, this could certainly viewed as a worrying fact, with bad implications for the future of real interest rates and possibly inflation. A couple of days later, however, the IMF published a fascinating chapter in its latest World Economic Outlook (WEO) on global real interest rates, showing that the global real rate has fallen from about 6 per cent in the early 1980s to about zero today.

Both of these facts are of course very well known, but placed side-by-side, they still represent a stark contrast:

They also present a conundrum for policy makers and investors. Why has the surge in public debt not resulted in a large rise in real borrowing costs for the government, and for the wider economy? And what does this tell us about the future of the risk free real rate in the global economy?

The risk free rate is the bedrock of asset valuation, and is often presented as one of the great “constants” in economic models. But in the past few decades, it has been anything but constant.

Mainstream macro-economic theory assumes that the global real interest rate is determined in the market for capital or “loanable funds”. An upward shift in the demand for capital (from higher investment or more public debt) will raise real rates, and a rise in the supply of capital (from higher savings) will reduce them.

Empirical studies generally confirm that the positive association between public debt and real rates, expected in theory, does indeed exist (though this is controversial and not well pinned down). Therefore the strongly negative relationship between the two variables since 1983 is certainly a prima facie puzzle.

The solution lies in the “ceteris paribus”, or other things equal, clause implicitly inserted into all economic models. Other things, in this case, have certainly not been equal. While the rise in public debt, taken on its own, would probably have increased real rates, other economic forces have worked more powerfully in the opposite direction.

The IMF says that the main reason for the drop in real rates in the 1980s and 1990s is obvious: the easing in monetary policy that occurred after the 1979-82 Volcker tightening. After 2000, the IMF identifies other forces, each of which is associated with a different school of economic thinking:

The IMF has been rather coy in presenting its overall findings in a coherent summary table, presumably for internal political reasons. (Paul Krugman complains of IMF “euphemisms”.) I have therefore tried to summarise the research in the table above, piecing together various statements in the paper, along with the video summary presented by the IMF’s Andrea Pescatori last week (well worth watching here).

Note that the causes of the drop in real rates vary through the different eras, but together they exert downward forces which swamp any upward impact from the rise in public debt. Note also that quantitative easing by the central banks is hardly mentioned at all among the forces that have held real rates down, which is interesting in view of the amount of attention it has received from investors since 2008. It seems odd that the IMF has assigned almost no importance whatever to QE, but it certainly cannot be the main factor, since two-thirds of the fall in real yields occurred before QE even started.

All this has clear implications for the future. The IMF has been too cautious to highlight its projected path for real rates in the published chapter of the WEO, but the graph above appears briefly in the video.

It shows the global real rate rising from 0.5 per cent now to only 0.5-2.0 per cent by 2018. Even at the high end of this band, this means that the global real rate will remain well below the growth rate of global real GDP throughout the medium term horizon.

Conclusion

The full implications of this research are profound, and they require a more complete treatment in a later blog. But three conclusions are obvious:

1) If the global real long term rate rises to only 1.25 per cent in 2018, the equilibrium nominal bond yield (with inflation expectations at the 2 per cent target) will be only 3.25 per cent, suggesting that any further bear market in bonds will be limited in scale from here.

2) The equilibrium real short rate in the next era should be well below the 2 per cent built into conventional monetary policy rules prior to 2008. This will restrict the extent of central bank tightening up to 2018 (assuming that Ms Yellen et al believe this research, as they probably do).

3) Those of us who have been worried about the rise in public debt in Japan, the UK and the euro area periphery (not the US or the euro area as a whole) may have been exaggerating the risks that budgetary policy in these regions is in imminent danger of becoming unsustainable. More on this another time.

Both of these facts are of course very well known, but placed side-by-side, they still represent a stark contrast:

They also present a conundrum for policy makers and investors. Why has the surge in public debt not resulted in a large rise in real borrowing costs for the government, and for the wider economy? And what does this tell us about the future of the risk free real rate in the global economy?

The risk free rate is the bedrock of asset valuation, and is often presented as one of the great “constants” in economic models. But in the past few decades, it has been anything but constant.

Mainstream macro-economic theory assumes that the global real interest rate is determined in the market for capital or “loanable funds”. An upward shift in the demand for capital (from higher investment or more public debt) will raise real rates, and a rise in the supply of capital (from higher savings) will reduce them.

Empirical studies generally confirm that the positive association between public debt and real rates, expected in theory, does indeed exist (though this is controversial and not well pinned down). Therefore the strongly negative relationship between the two variables since 1983 is certainly a prima facie puzzle.

The solution lies in the “ceteris paribus”, or other things equal, clause implicitly inserted into all economic models. Other things, in this case, have certainly not been equal. While the rise in public debt, taken on its own, would probably have increased real rates, other economic forces have worked more powerfully in the opposite direction.

The IMF says that the main reason for the drop in real rates in the 1980s and 1990s is obvious: the easing in monetary policy that occurred after the 1979-82 Volcker tightening. After 2000, the IMF identifies other forces, each of which is associated with a different school of economic thinking:

- A drop in investment demand in the advanced economies. This is very similar to the secular stagnation hypothesis, recently advanced by Larry Summers and Paul Krugman. On this view, real rates have been reduced by low rates of investment, which are in turn due to the global recession post 2008 and to the IT revolution. The latter has cut the prices of investment goods (think more computers and less steel mills), and this has cut the demand for loanable funds. The IMF says that these effects are unlikely to be reversed very rapidly in the years ahead. In fact, they expect the investment ratio in the advanced economies to stay well below pre-crash levels, while the savings ratio begins to rise moderately. Overall, this might even exert some downward pressure on real rates from here.

- An excess of savings in the emerging economies. This view is mainly associated with Ben Bernanke, who warned of a global savings glut in 2005. This shifts the supply of loanable funds to the right, also reducing real rates. The IMF says that this factor was particularly important from 2002-07, and warns that it may reverse somewhat in the next few years, exerting some upward pressure on real rates.

- A portfolio shift towards bonds and away from equities. This view, associated with John Campbell and others, suggests that the increased volatility of equities after the 2000 crash, along with a drop in the inflation risk premium on bonds as monetary policy credibility has improved, has increased the demand for bonds and depressed the real rate. Many investors seem to think that this shift will be reversed in the year ahead, with a “great rotation” away from bonds. But the riskiness of equities is not declining, and the inflation risk premium on bonds is not rising, so the chances of a major reversal in this factor also look to be limited.

- There is much more on each of these forces in the WEO chapter, but the major point is that together they are capable of explaining why the rise in public debt has been contemporaneous with a major drop in real rates, not just recently, but progressively for three solid decades.

The IMF has been rather coy in presenting its overall findings in a coherent summary table, presumably for internal political reasons. (Paul Krugman complains of IMF “euphemisms”.) I have therefore tried to summarise the research in the table above, piecing together various statements in the paper, along with the video summary presented by the IMF’s Andrea Pescatori last week (well worth watching here).

Note that the causes of the drop in real rates vary through the different eras, but together they exert downward forces which swamp any upward impact from the rise in public debt. Note also that quantitative easing by the central banks is hardly mentioned at all among the forces that have held real rates down, which is interesting in view of the amount of attention it has received from investors since 2008. It seems odd that the IMF has assigned almost no importance whatever to QE, but it certainly cannot be the main factor, since two-thirds of the fall in real yields occurred before QE even started.

All this has clear implications for the future. The IMF has been too cautious to highlight its projected path for real rates in the published chapter of the WEO, but the graph above appears briefly in the video.

It shows the global real rate rising from 0.5 per cent now to only 0.5-2.0 per cent by 2018. Even at the high end of this band, this means that the global real rate will remain well below the growth rate of global real GDP throughout the medium term horizon.

Conclusion

The full implications of this research are profound, and they require a more complete treatment in a later blog. But three conclusions are obvious:

1) If the global real long term rate rises to only 1.25 per cent in 2018, the equilibrium nominal bond yield (with inflation expectations at the 2 per cent target) will be only 3.25 per cent, suggesting that any further bear market in bonds will be limited in scale from here.

2) The equilibrium real short rate in the next era should be well below the 2 per cent built into conventional monetary policy rules prior to 2008. This will restrict the extent of central bank tightening up to 2018 (assuming that Ms Yellen et al believe this research, as they probably do).

3) Those of us who have been worried about the rise in public debt in Japan, the UK and the euro area periphery (not the US or the euro area as a whole) may have been exaggerating the risks that budgetary policy in these regions is in imminent danger of becoming unsustainable. More on this another time.

0 comments:

Publicar un comentario