Buttonwood

Sound the retreat

Profits in America may have peaked for this cycle

Apr 26th 2014

.

ARE corporate profits at last running out of steam? The lead-up to the first-quarter results season on Wall Street was marked by an unusually large number of profit warnings, such as that from Chevron, an oil group. According to Morgan Stanley, an investment bank, earnings estimates for S&P 500 companies were revised down by 4.4 percentage points in the first quarter.

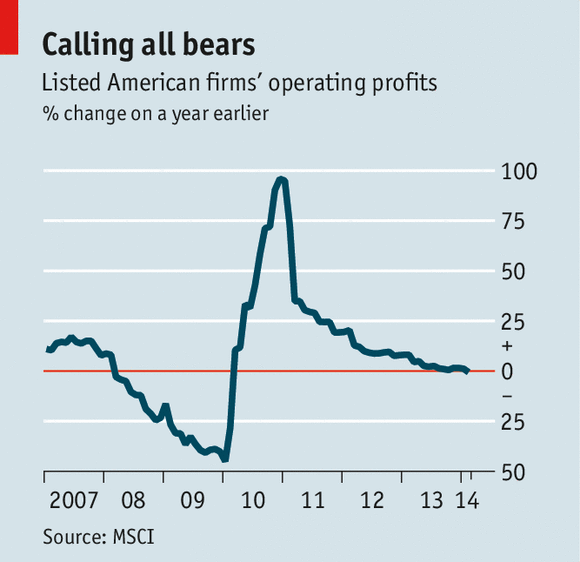

As is the custom, having lowered the bar, companies will now beat those revised forecasts, allowing Wall Street analysts to proclaim a “successful” results reason. But when one removes the effect of exceptional items (such as writedowns the year before), American profits are now falling, not rising, according to data from MSCI (see chart).

In a sense, this is about time. The recovery in American corporate profits since the recession has been remarkable: they are close to a post-war high as a proportion of GDP. Bulls have a number of arguments why this is a lasting, not cyclical, phenomenon. Economic power has shifted from labour to capital thanks to globalisation, they say; companies can move production to parts of the world where wages are lower. But if that effect is so strong, why aren’t profits as high elsewhere? In Britain the return on corporate capital is below its post-1997 average.

An alternative, but related, line of reasoning is that foreign profits have boosted the earnings of companies in the S&P 500, making the relationship with domestic GDP less relevant. America may still be running a trade deficit but its global champions, the argument runs, are raking in the money overseas. Research by Audit Analytics found that the amount of profits held abroad and not repatriated nearly doubled to $2.1 trillion between 2008 and 2013.

But where will American multinationals make so much money in future? Not in either Europe or Japan, where the economies have barely grown in recent years. Emerging markets might seem more promising, but their economies have been slowing, as companies like Diageo, a drinks producer, and Cisco, a tech-components group, have reported. Several developing economies have seen their currencies fall sharply too. It seems unlikely that American multinationals are going to get a further spurt of profits from this source.

In any case, the global data do not bear out the overseas-profit argument. Just as in America, there have been regular disappointments. In 2012, according to Citibank, global profits growth was just 2%, compared with initial forecasts of 11%. At the start of 2013 profits were forecast to rise by 12%; the actual increase was 7%.

The stockmarket has been remarkably resilient in the face of these setbacks. In 2012 global equities rose by 13%; last year they managed 24%. In part, that is due to optimism about the economy’s future trajectory. The euro-zone crisis has disappeared from the headlines while the American economy has been showing signs of returning to healthy growth.

But it is also down to supportive monetary policy. Short-term interest rates have not budged for the past two years (in the developed world) and government-bond yields have been close to historic lows. Investors have accordingly turned to the stockmarket in search of higher returns. Low interest rates have also played their part in keeping profits high, by reducing borrowing costs and by encouraging companies to use their spare cash to buy back stock, thereby increasing earnings per share.

However, buying back shares suggests a certain lack of imagination on the part of chief executives, or a lack of profitable projects to back. That remains an odd aspect of the profits boom: in theory, if the return on capital is high, one would expect a lot of capital to be invested. The resulting competition would eventually cause profits to fall. The process acts as a natural check on profits growth, but has yet to occur this cycle.

Instead, chief executives are turning to that old device for boosting sluggish profits: takeovers. According to Thomson Reuters, the global value of mergers and acquisitions in the first quarter was 36% higher than in the same period of 2013. The right takeover can result in cost cuts through economies of scale—although in the long run, the academic evidence in favour of takeovers is mixed.

A takeover boom is a classic signal of the final stages of a bull market, a sign that financial engineering has taken over from genuine business expansion. And that is hardly a surprise: the current rally is already the fourth-largest and the fifth-longest-running since 1928.

0 comments:

Publicar un comentario