- Market has failed to account for excellent resource update in February.

- This resource update gives RIOM the financial flexibility to build Phase II of the La Arena mine without diluting shareholders.

- Phase II feasibility study results this summer offers catalyst for sudden repricing of stock higher.

- The market currently values Phase II at nearly zero. As such, Phase II is a nearly free call option on 4 billion pounds of copper/4 million ounces of gold.

- Existing operations are worth roughly $2/share, limiting downside even if Phase II doesn't work out.

The complaint with Rio Alto has always been that while La Arena is a well-run and highly economic mine, its lifespan would be too short to justify a higher valuation for the company's shares. Whenever I speak with other investors about the company, I hear something along the lines of: "Yeah, great mine, but what happens in 2016 or 2017 when its oxide gold is depleted?"

(click to enlarge)

(La Arena oxide operations. Author's photo from his mine visit. July 2013)

Now, at the current run rate of just over 200,000 ounces of gold production per year, the mine has sufficient supply to run until the end of 2019, and the new resource estimate notes that there are several open faces of gold mineralization. Rio Alto will be doing more drilling this year in hopes of expanding the resource base further.

With a minimum of at least five years of gold production forthcoming from the oxide phase of La Arena, the company should generate something along the order of $400 million in cash flow from the remainder of operations at current gold prices assuming no further exploration upside. Since Rio Alto's current enterprise value is merely $330 million, the company is selling at a significant discount to the cash it will be receiving from its existing operations.

If, unlike in this past year, there is no further gold found in further exploration efforts, and the price of gold fails to advance over the next 5 years, discounting the cash flow that will be generated from operations, you arrive at a value roughly equal to where Rio Alto trades now. So, assuming exploration failure, gold price stagnation, and valuing the company's other assets at zero, the company is more or less fairly valued at the prevailing $2/share price. With the company's all-in mining cost likely to be around $1,000/oz in 2014, the company will remain significantly profitable barring a complete meltdown in the price of gold. And the company's balance sheet remains pristine, with a sizable chunk of cash and almost no debt. While there's obviously no such thing as a low-risk junior mining stock, Rio Alto has about as limited a downside profile as anything you're going to find in the sector.

And for the upside? Simply look to the company's enormous Phase II sulphide project at La Arena, adjacent to the company's existing Phase I oxide operations.

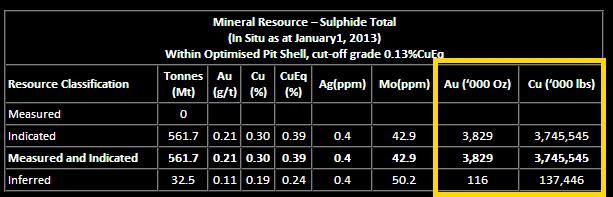

A previous resource estimate shows something along the lines of 4 million ounces of gold and 4 billion pounds of copper there (though to be fair, this estimate assumed $3.50/lb copper, and it's trading closer to $3/lb at the moment).

Source: Rio Alto website

Rio Alto was originally targeting a Phase II that would operate at production levels of 31,000/oz of gold and 60 million pounds of copper a year for 21 years. From the beginning of operations of La Arena, the idea was to use the highly economic but shorter-lifespan Phase I project to fund Phase II, which would be the meat of the operation, with its much greater volume and longer lifespan.

The market initially liked this idea, and Rio Alto shares surged from sub-dollar to nearly $6 by the end of 2012 as investors rewarded the company for consistently beating guidance, controlling costs, and generally running a tight ship. But in 2013, investors fled the gold mining sector in droves, and Rio Alto fared particularly badly, underperforming its sector ETF by a significant margin, despite the fact that Rio Alto remained strongly profitable while many of its peers veered into unprofitably under the burden of sinking gold prices. As one of the lowest-cost gold producers in the world, and sheltered by a strong balance sheet, Rio Alto should be one of the most defensive and resilient names in the sector, instead it was sold with reckless abandon.

(click to enlarge)

Source: Google Finance

Investors lost confidence in Rio Alto's story in particular because of concerns over the development of Phase II of the mine. Bank analysts began speculating that Rio Alto would not be able to fund the development of Phase II with internal cash flow from Phase I, as had been the plan, and instead that the company would be forced to raise debt or do a dilutive offering to fund Phase II. Many investors figured it'd be better to avoid the company's shares until there was some clarity as to the funding of Phase II.

With the new resource update from oxide operations, this concern has been greatly alleviated. Rio Alto needs something along the lines of $200 to $250 million to fund initial construction of Phase II. By contrast, Rio Alto generated $77 million in cash flow from operations in 2013, and with the company's cost-cutting measures including a reduced fleet size for 2014 combined with increased gold production guidance for this year, cash flow from operations is likely to remain stable if not increase to a small degree.

With five years of production left from the mine, (again assuming no more exploration success - in fact there's likely more than five years left) Rio Alto needs to generate just $50 million a year more or less in cash flow to fund Phase II internally. Given that it produced $98 million in cash flow from operations in 2012 and $77 million last year, the company should be able to generate the cash that is needed to fund Phase II with relative ease. Even if gold falls back toward $1200/oz, the company still has a good deal of breathing room thanks to the dramatic increase in its reserve base. And with that, the overhang on the company's shares coming from the expectation of future dilution should have lifted. And yet shares have traded flatly since February, entirely failing to account for this great development.

Best of all, Phase II is being valued at essentially zero by the market at present. As we established previously, if Rio Alto were to do nothing but collect cash from its existing operations until they terminate, the end result is likely to be a pile of cash greater than the company's current enterprise value. As such, downside is quite limited. The upside of a large 21-year lifespan copper/gold mine containing close to 4 million ounces of gold and 4 billion pounds of copper is admittedly hard to pin down exactly. The feasibility study for the project is slated to arrive in the middle of this year, and will greatly help in being able to establish a more precise valuation for Phase II.

Back in 2012-early 2013, various bank analysts pegged Phase II as being worth roughly half of Rio Alto's total value, something along the order of $2.50-$3/share. Obviously its value has fallen a bit with the decline in metals prices, but it hasn't fallen to $0, or to anything close to $0 in fact. Assume conservatively that the remainder of Phase I is worth $2 per share, and that Phase II is also worth $2 per share, and you have the formula for a clean double in Rio Alto shares from their current $2 price.

Again, this is back of the napkin math, and we really need to see the Phase II feasibility study before we can make more precise estimates. Regardless, the market is now valuing Phase II as if it's not going to happen, and as such, the opportunity now exists to buy a virtually free call option on a 21-year lifespan 3 billion plus pound copper/3 million plus ounce gold deposit that sits adjacent to a highly successful and economic operating mine.

What's this call option worth? If the analysts were right, something along the lines of $2.50-$3 a share, in which case the whole of Rio Alto is worth something close to $5/share ($2/share for Phase I, $3 for Phase II). Obviously shares won't be going there in a straight line; until the feasibility study sheds more light on the exact nature of the potential of Phase II, it remains difficult for outsiders to value. But unless Phase II turns out to be a complete bust, shares will be worth more than $2, as Phase II is revalued at something, rather than the near complete zero the market now gives it. And should the feasibility study surprise to the upside and/or gold and copper prices improve, there's the potential for a lot more upside in the value of Phase II beyond the $2.50-$3/share value that analysts had assigned it.

When Rio Alto was developing Phase I, it was originally planning a mine along the lines of 100,000 ounces gold a year. The company dramatically underpromised and overdelivered, as production has grown to twice that, and at better grades than originally anticipated. Since then, the company has beaten its annual guidance every year. In an industry filled with hype, promotions, and swindlers, Rio Alto has established a track record of professionalism and reliability, offering modest guidance and then beating it handily. As such, I have confidence in the management team to exceed the market's expectations should it choose to build Phase II.

I also have confidence that CEO Alex Black will make a wise decision on the construction of Phase II. When I met with him at the company's Lima offices in December 2013, he emphasized that Rio Alto will not build Phase II if the feasibility study does not show a robust internal rate of return (IRR). Rio Alto is looking at various other projects around Peru and Latin America to continue the company's mining operations post Phase I. With the mining sector in the dumps and many junior mining and exploration companies struggling to fund their ongoing operations, there is great opportunity for cash-rich companies such as Rio Alto to acquire assets at fire sale prices.

And CEO Alex Black has done it before. Remember that he acquired La Arena for a measly $49 million in cash from Iamgold (IAG). Not a bad purchase price for a mine that would go on to produce more than $100 million in net income during its first year of operations. Even should Phase II be uneconomic at current metals prices, there is good reason to have confidence that Rio Alto will wisely use its cash to pursue other profitable ventures. And even in that case, Phase II retains value to the degree that 4 million ounces of gold and 4 million pounds of copper sitting in the ground hold option value should metals prices increase in the future. Rio Alto can shelve Phase II and come back to it if copper picks back up toward $4/lb should it find other better uses of its capital.

Talking with Mr. Black in December, it was clear that he is confused and frustrated by the company's current share price. He has built the company from the beginning, acquired La Arena in a shrewd deal at an excellent price, built Phase I on time and within budget and operated it far more successfully than analysts had anticipated prior to the mine commencing operations. Insiders own a large chunk of the company, Black himself owns close to 4% of the company, and he hasn't been selling even as shares have fallen sharply over the past year.

(click to enlarge)

Source: Company presentation

Management has done everything right running the company up to this point, it is following a logical development plan for Phase II while aggressively pursuing other opportunities should Phase II not pan out, and yet the company is being valued at less than the residual cash flow of its already existing operations, discounting any upside from exploration, higher metals prices, Phase II, or a deserved premium for its excellent CEO. And shares have lagged its sector ETF, despite Rio Alto being a much higher-quality and more defensive name than many of its sector peers.

In short the market is pricing Rio Alto as if it is a bust, on its last legs mining out what's left of Phase I. In truth, Phase I is still a dynamic asset, as this year's 50% upgrade to resource life showed, and Phase II on its own has the potential to be worth more than the company's entire market cap. With the catalyst coming this summer in the form of a new feasibility study for that asset, Rio Alto shares could reprice dramatically higher as investors suddenly remember the value of a now seemingly forgotten asset.

And even if Phase II doesn't lead to dramatic upside this summer, Phase I provides plenty of stability to sustain the current $2 share price. In 2013, not exactly a banner year for the average gold miner, Rio Alto produced $285 million of revenue, of which it turned $109 million into gross profit, $93 million of operating earnings, and $30 million of net income. Even despite the low gold price, Rio Alto still cranks out a more than respectable 38% gross margin, and trades at 3.5x forward operating earnings and roughly 6x forward PE.

In the past, people have said Rio Alto was cheap with a reason - as the mine was going to run out of gold in 2016 or 2017. But now, with gold production likely to run on into the next decade, it's getting harder and harder to ignore the incredible value proposition Rio Alto represents at its current $2 share price. And should Phase II's feasibility study show a strongly economic mine, look out: what the market has currently valued at near zero will appreciate in a hurry. Phase II is easily worth $2-$3/share should the feasibility study turn out all right, in which case Rio Alto shares would likely double over the coming year or two.

I'm not the only person getting excited, three separate bank analysts have raised their Rio Alto price targets since February, and the consensus analyst opinion is a buy and C$3.37 price target, offering 50% upside from the present price. With limited downside, Rio Alto represents a most attractive way to play a potential rebound in the mining sector generally with the kicker that Phase II represents a virtually free call option on a gigantic 21-year copper/gold project that has the potential to revalue the company's shares way higher later on this summer.

0 comments:

Publicar un comentario