Limiting leverage at American banks

Beyond Basel

America raises capital requirements for banks, widening the gulf with Europe

Apr 12th 2014

“I ALWAYS have concerns about banks,” laments one European finance minister, “It’s part of my job description.” As Europe’s economies drag themselves back out of recession, a common refrain from politicians and industrialists is that their economies are being slowed by ailing banks. Mountains of bad debts, many not yet written off, and the resulting shortage of capital are restricting the flow of credit to the rest of the economy. The response of many European bank regulators has been to look the other way in the hope that forbearance and time will revive their banks.

In America, by contrast, regulators are ratcheting up the levels of capital (mainly equity and retained profits) they demand of banks, convinced that it will lead not just to a safer banking system but also one better able to lend to companies. On April 8th the different agencies that supervise American banks agreed to impose a minimum ratio of capital to assets (usually called the leverage ratio) of 5% on the country’s biggest banks. At the units that qualify for deposit insurance, the minimum will be 6%.

As a result, big American banks will have to raise about $22 billion in capital. A proposed modification to the methodology used to calculate the leverage ratio could add another $46 billion to the total. These figures appear large. Yet if set against the profitability of American banks, they are manageable. JPMorgan Chase, for instance, earned almost $18 billion last year.

The new rule underscores a loss of faith by bank supervisors in a once-revered concept: risk weighting. This was the notion that banks should be allowed to vary the amount of capital on their balance-sheets depending on the riskiness of their lending. Although elegant in theory, it proved badly flawed in practice: the crisis revealed that banks and their overseers had vastly underestimated the risks that had built up in the financial system.

Leverage is a simpler, if cruder, measure of banks’ riskiness and is meant to provide a backstop to more sophisticated risk-weighting measures. Yet American regulators are going far beyond the minimum leverage ratio of 3% set by the Basel Committee, which draws up international rules for banks.

This will further widen a gulf that has emerged since the crisis between the capitalisation and health of America’s banks and those in Europe. Officials at the Federal Reserve reckon that America’s biggest banks have added some $500 billion in high-quality capital to their balance-sheets since the financial crisis. Banks in the euro area, by contrast, have added only €235 billion ($324 billion), even though they are far larger relative to GDP than America’s, so their capital needs are greater.

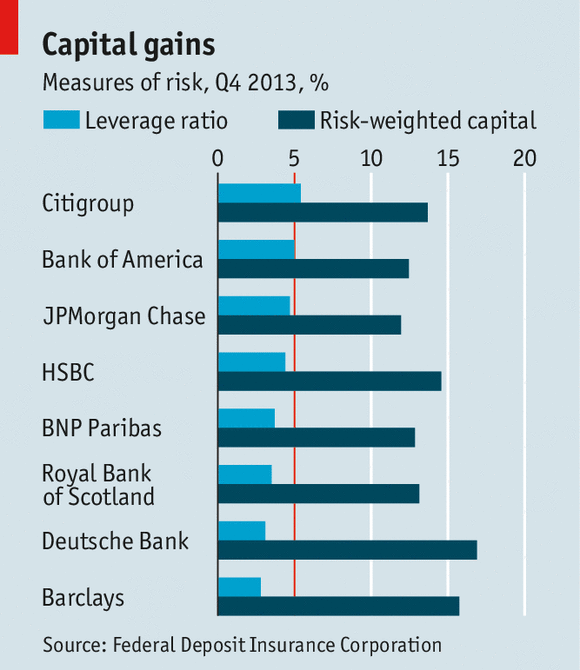

The two banking systems are not completely comparable, largely because European banks hold large portfolios of mortgages on their balance-sheets. The differences are nevertheless striking. Whereas most big American banks are close to their new leverage target of 5%, many European banks are struggling to meet the lower Basel threshold (see chart). And this gap is likely to widen as senior American regulators press for an even higher leverage ratio.

In America, by contrast, regulators are ratcheting up the levels of capital (mainly equity and retained profits) they demand of banks, convinced that it will lead not just to a safer banking system but also one better able to lend to companies. On April 8th the different agencies that supervise American banks agreed to impose a minimum ratio of capital to assets (usually called the leverage ratio) of 5% on the country’s biggest banks. At the units that qualify for deposit insurance, the minimum will be 6%.

As a result, big American banks will have to raise about $22 billion in capital. A proposed modification to the methodology used to calculate the leverage ratio could add another $46 billion to the total. These figures appear large. Yet if set against the profitability of American banks, they are manageable. JPMorgan Chase, for instance, earned almost $18 billion last year.

The new rule underscores a loss of faith by bank supervisors in a once-revered concept: risk weighting. This was the notion that banks should be allowed to vary the amount of capital on their balance-sheets depending on the riskiness of their lending. Although elegant in theory, it proved badly flawed in practice: the crisis revealed that banks and their overseers had vastly underestimated the risks that had built up in the financial system.

Leverage is a simpler, if cruder, measure of banks’ riskiness and is meant to provide a backstop to more sophisticated risk-weighting measures. Yet American regulators are going far beyond the minimum leverage ratio of 3% set by the Basel Committee, which draws up international rules for banks.

This will further widen a gulf that has emerged since the crisis between the capitalisation and health of America’s banks and those in Europe. Officials at the Federal Reserve reckon that America’s biggest banks have added some $500 billion in high-quality capital to their balance-sheets since the financial crisis. Banks in the euro area, by contrast, have added only €235 billion ($324 billion), even though they are far larger relative to GDP than America’s, so their capital needs are greater.

The two banking systems are not completely comparable, largely because European banks hold large portfolios of mortgages on their balance-sheets. The differences are nevertheless striking. Whereas most big American banks are close to their new leverage target of 5%, many European banks are struggling to meet the lower Basel threshold (see chart). And this gap is likely to widen as senior American regulators press for an even higher leverage ratio.

0 comments:

Publicar un comentario