Summary

- The stock market is facing mounting economic and geopolitical risks as we move through 2014.

- As a result, the threat of a major stock market correction is rising.

- Four particular asset classes provide investors with the ability to not only hedge against a stock market decline but capitalize on it.

Storm clouds continue to accumulate on the stock market horizon. Following an impressive five-year rally that saw stocks not only rebound from its financial crisis lows but also explode to new highs, signs are continuing to emerge that a change may soon be coming. So while the skies remain generally sunny over the U.S. stock market today with the major averages continuing to set new highs amid notably persistent investor bullishness, it may not be long before markets find themselves confronted with the final judgment when the markets are ultimately forced to begin truly working through all of the excesses that were accumulated first leading up to the financial crisis and then even more so in its aftermath. It may be a few months, a couple of years or perhaps even longer before we finally arrive at this inflection point. Then again, it may have just now gotten underway. Only time will tell. But regardless of the timing, as long as the global economy continues to languish, debt continues to accumulate, and geopolitical tensions continue to mount, such a judgment day is coming. Fortunately, for those investors concerned about such an outcome, investment markets provide not only a way to protect against potential losses but also to achieve impressive rewards for those that are best prepared.

So exactly, how close are we to any potential major U.S. stock market (SPY) apocalypse like we saw from 2000 to 2002 and again from 2007 to 2009? At this point, no such correction appears imminent. In fact, it remains incredibly resilient in its ability to continuously rise despite the fact that economic and corporate fundamentals have stalled over the past two years and nearly every other major global investment class that is traditionally highly correlated with the U.S. stock market has fallen by the wayside including some that have registered notable losses in recent years. Thus, the reasonable strategy for now is to remain net long the stock market at least until we begin to see signs that the uptrend is poised to break, which is a topic I recently explored in detail in a previous article.

(click to enlarge)

Unfortunately, for the bulls, the further the stock market continues to levitate without any meaningful fundamental support beneath it, the more painful the final correction is likely to be. Conversely, while the last few years have been relentlessly painful for the bears, the further stocks continue to soar only increases the robustness of the opportunity set if and when the U.S. stock market finally succumbs. Only time will tell how it all plays out, but for those that are prepared for such a downside outcome, the potential upside could be absolutely enormous once it all begins to play out.

So how exactly can investors position for a potential stock market apocalypse?

The notion of portfolio diversification as we have come to know it from our mutual fund and ETF investment product providers as well as our 401(k) and 403(b) benefit packets is woefully insufficient to do the job. This is due to the fact that correlations across style, size and geography within the global stock market at +0.80 to +1.00 are far too high to provide any reasonable protection once judgment day finally arrives (note: correlations range from -1 to 0 to +1 with -1 meaning two holdings move completely opposite of each other (perfect negative correlation), +1 implying that two holdings move in complete alignment with each other (perfect positive correlation) and 0 suggesting that two holdings are completely unaffected by the price movement of the other (uncorrelated)). In short, regardless of whether you own U.S. small cap value stocks (IWN) or frontier markets (FM), if the stock market breaks, it is almost certain to take everything down with it to varying degrees.

Diversification across other well-known and commonly held asset classes is also inadequate. For example, many investors may have access to categories like high yield bonds (HYG) or REITs (VNQ) in their retirement plans that are designed to provide for allocations that will move in different directions than stocks over time. But with correlations still in the +0.70 to +0.90 range, these too would likely be brought down along with the stock market under any major correction scenario.

What about core bonds? While it is positive that core investment grade bonds (AGG) have a very low positive correlation with stocks since the outbreak of the financial crisis at +0.15, they lack the returns potential to provide a meaningful portfolio returns offset in the event of a major stock market decline. For example, while core investment grade bonds did provide a nice portfolio offset during the financial crisis with a +10% gain over the duration of the crisis period, when incorporated in a traditional 60% stock and 40% bond strategy it still resulted in an overall portfolio decline of roughly -30%. Even a more conservative 40% stock and 60% bond strategy was down over -22% during this same crisis period. And given the fact that short-term interest rates have been pinned at effectively zero in the years since the financial crisis and many investment grade spreads have returned toward historically tight levels, the core bond market may be more limited today in its offset potential versus what it has exhibited during past bear markets.

Instead, investors must identify securities with certain distinct characteristics if they hope to not only effectively hedge their portfolio but also capitalize on any future major stock market correction. These characteristics include the following. First, they must be securities that trade like a stock. In other words, they have price volatility that is sufficiently high that it is comparable if not greater than the price movements exhibited by the stock market. Second, their price movements must be uncorrelated to negatively correlated with the stock market. This way, if the stock market is moving sharply in one direction, the alternative security in question either is largely unaffected or is responding by moving in the opposite direction. Third, they must have the demonstrated ability to perform well during sustained bear markets in stocks. Lastly, any such security in this category must be highly liquid and easily traded, for these are holdings that in some cases may be short term in nature and require the ability to both readily enter into and exit out of positions as warranted by market conditions.

The Four Horsemen Of The Stock Market Apocalypse

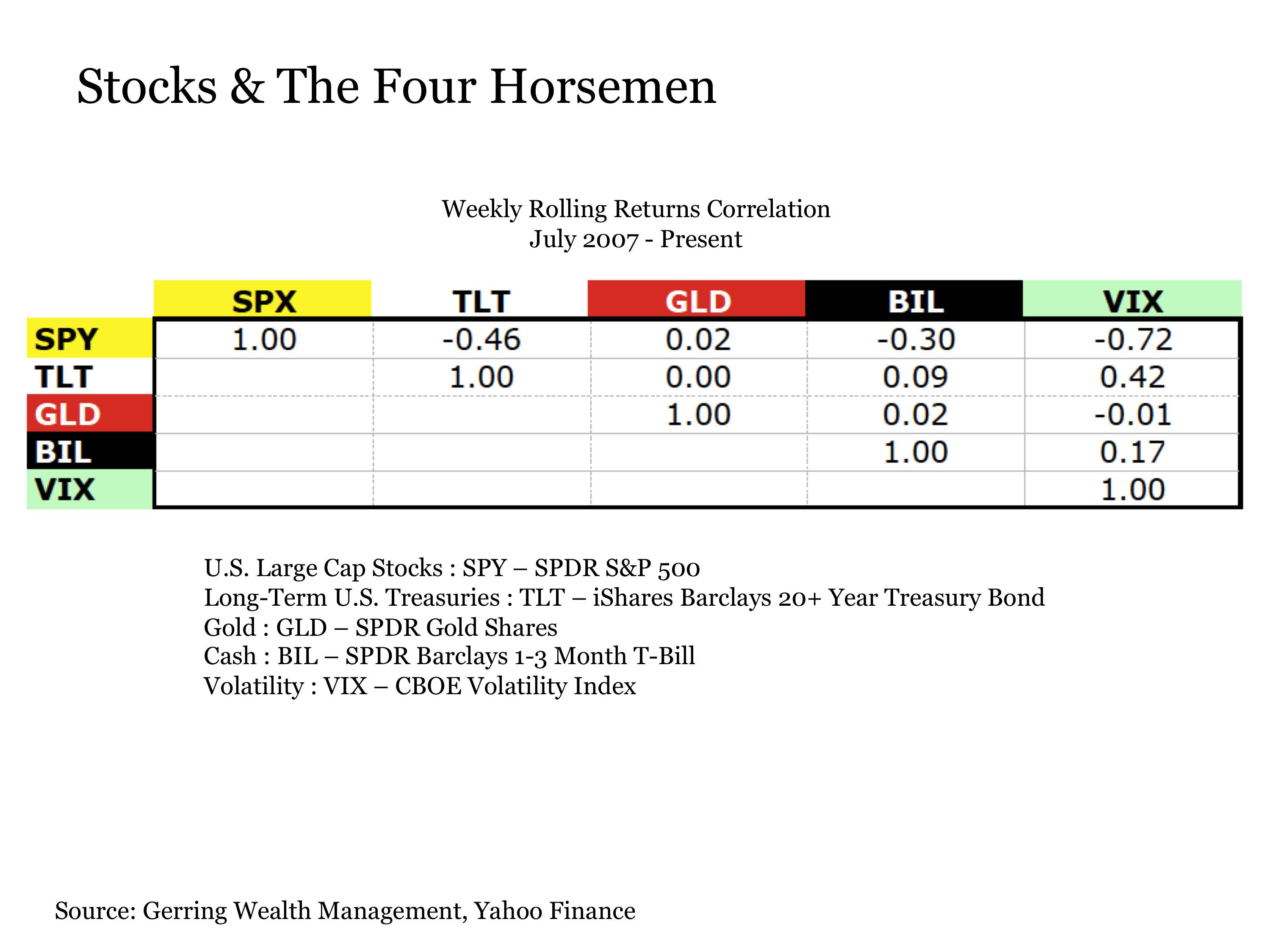

Across investment markets, four specific categories stand out as satisfying the prerequisites listed above in serving the role not only as hedges against a stock market decline but also as investments that can rise strongly in value in the process.These are Long-Term U.S. Treasuries, Gold, Cash and Volatility. Each is shown in the table below with their correlations relative not only to the U.S. stock market but also to each other. What is notable right from the start is that these investments not only have a low to negative correlation with the U.S. stock market, they also have a low to negative correlation with each other, only adding to the diversification benefit of considering each in the broader portfolio context.

(click to enlarge)

Before going any further, it is important to note the following. All of these are positions that should be viewed as tactical positions being undertaken with the intent of trying to not only protect against but also capitalize on a potential stock market correction. While the holding periods may vary for each of the securities mentioned below, these may be short-term allocations in many cases.

Moreover, the timing of when each of these positions is initiated is important along with when these positions are exited. In short, this is information that should not be viewed as a complete buy-and-hold strategy to initiate today. Instead, it is something that should be tactically managed with care and close attention over time.

The White Horse: Long-Term U.S. Treasuries

Long-term U.S. Treasuries (TLT) have served as an ideal way to hedge against a stock market correction, particularly since the outbreak of the financial crisis several years ago. And despite the concerns associated with a sustained outbreak of inflation given the extraordinarily aggressive monetary stimulus applied by the U.S. Federal Reserve along with other major central banks over the last several years, the fact that these threats continue to be conquered by deflationary forces suggest that the potential for further upside continues to exist for long-term U.S. Treasuries during a future stock market correction.

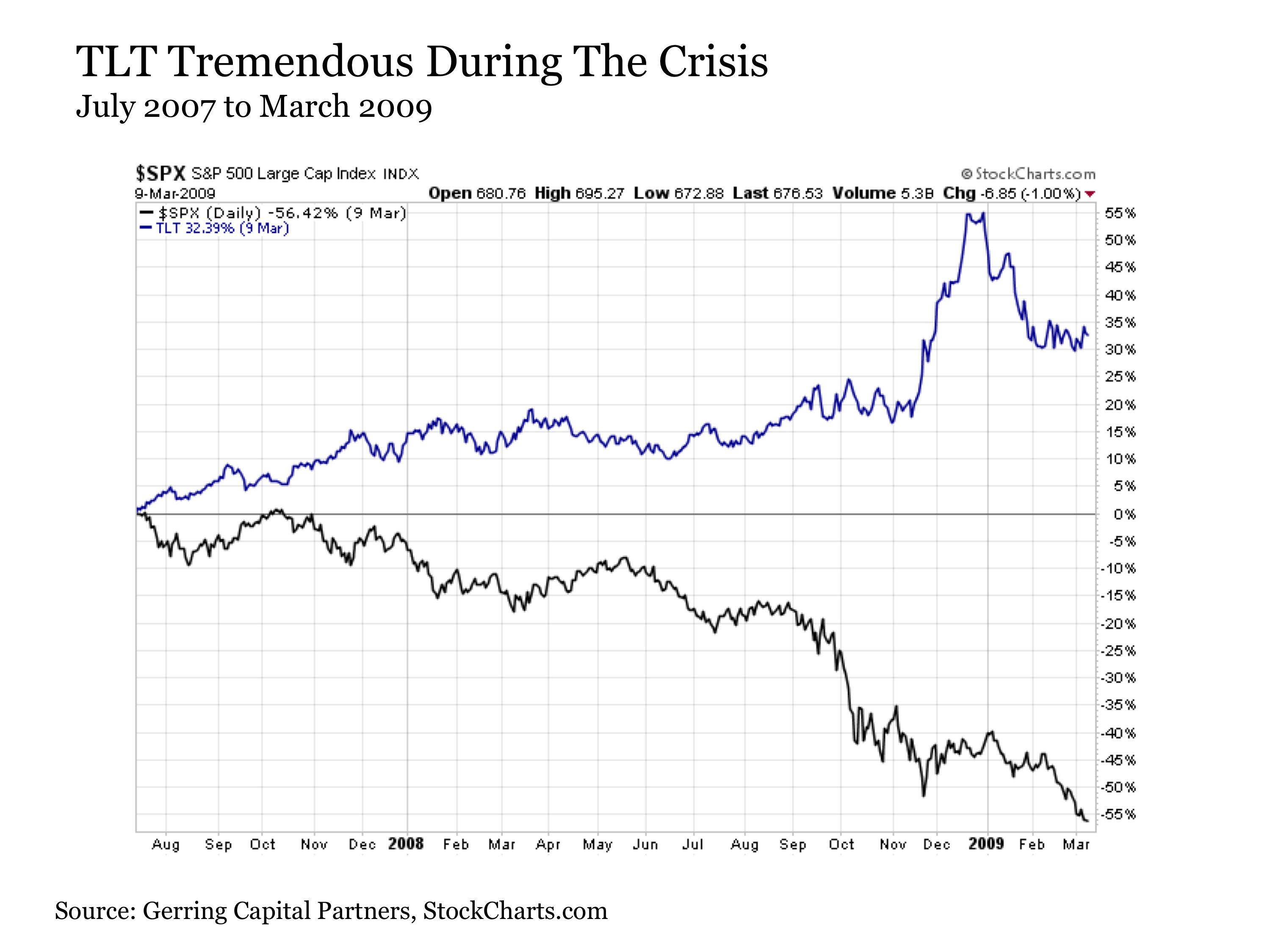

The performance of long-term U.S. Treasuries was tremendous during the financial crisis from July 2007 to March 2009. While the stock market as measured by the S&P 500 Index was in the process of falling by nearly -60%, the TLT was up by as much as +55% over the same time period.

(click to enlarge)

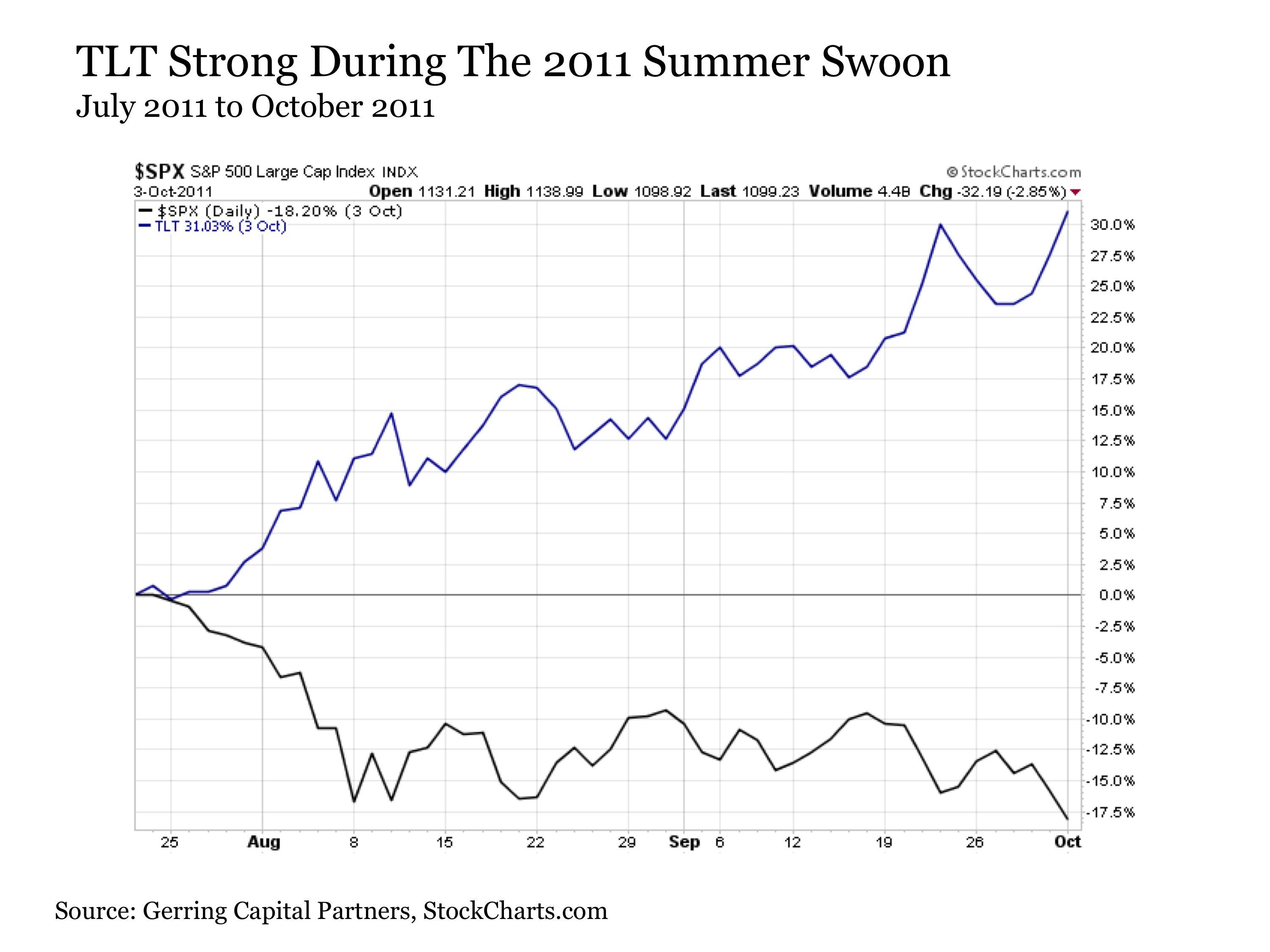

During the sharp stock market correction during the summer of 2011, we witnessed the similar strong outperformance of long-term U.S. Treasuries, as they advanced by +31% at a time when the stock market was falling by as much as -18%. Similar outcomes also held true during the stock market pullbacks in the summer of 2010 and the spring of 2012.

(click to enlarge)

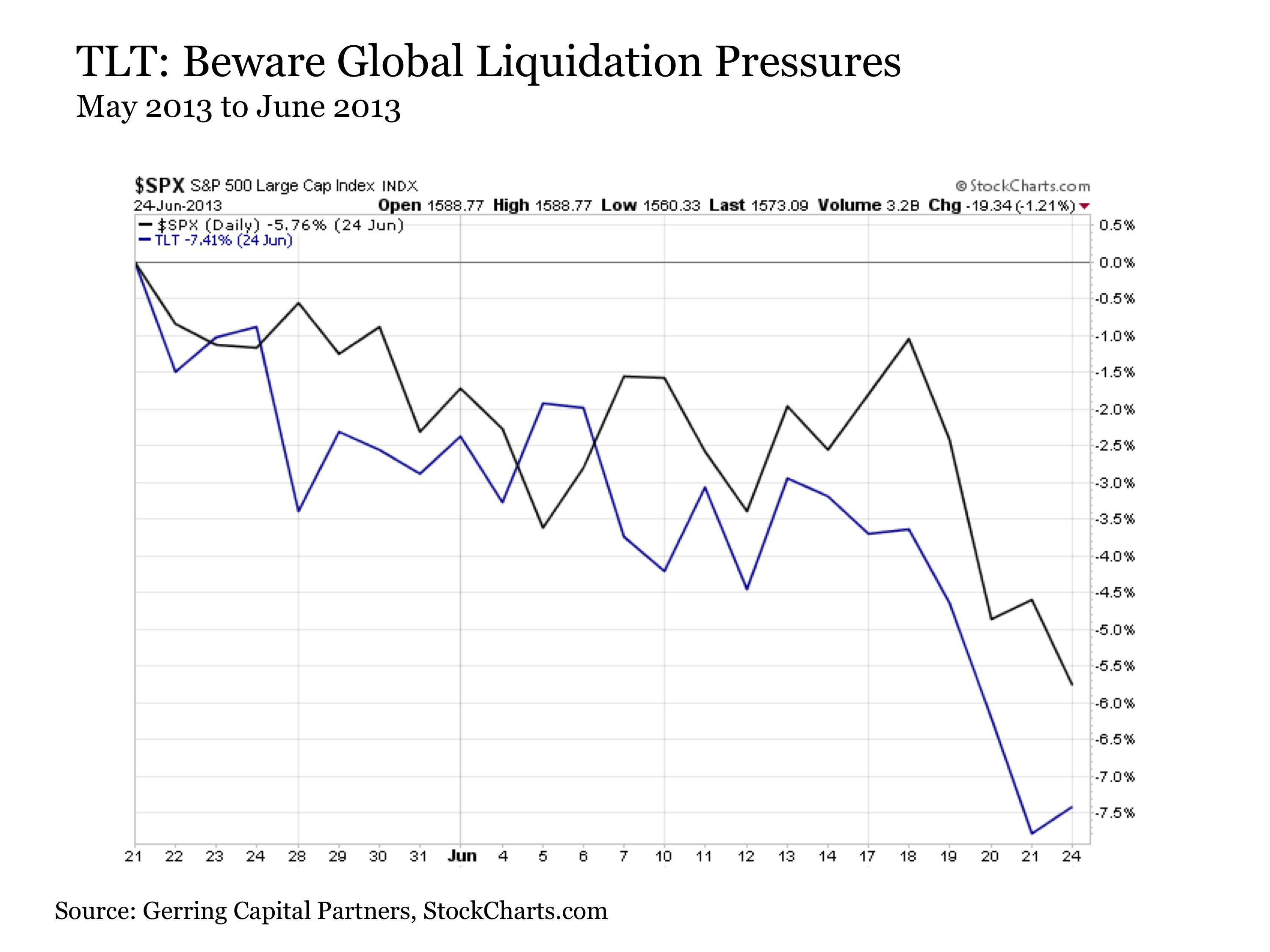

Despite this recently strong track record of performance during stock market corrections, a recent development warrants close attention and potential concern from a risk standpoint. During the sharp stock market decline from May 2013 to June 2013, the TLT did not burst to the upside. Instead, it actually underperformed U.S. stocks to the downside. This outcome was particularly notable, as it coincided not only with the Fed revealing its intention to scale back on asset purchases, which is something that I view as a positive for Treasuries given their historical performance during the QE era, but also with the earliest efforts by Chinese policy makers and the People's Bank of China to tighten liquidity and curb speculative activity. In short, if the reform efforts in China or actions in any other part of the world lead to heightened liquidation pressures, all bets are off not only for U.S. stocks but also U.S. Treasuries. Such is a risk that investors must stay attuned to when positioning in this category.

(click to enlarge)

With that being said, long-term U.S. Treasuries were once again a strong performer during the most recent stock market pullback from late January to early February, gaining +4% while the U.S. stock market was down -6% over the same time period.

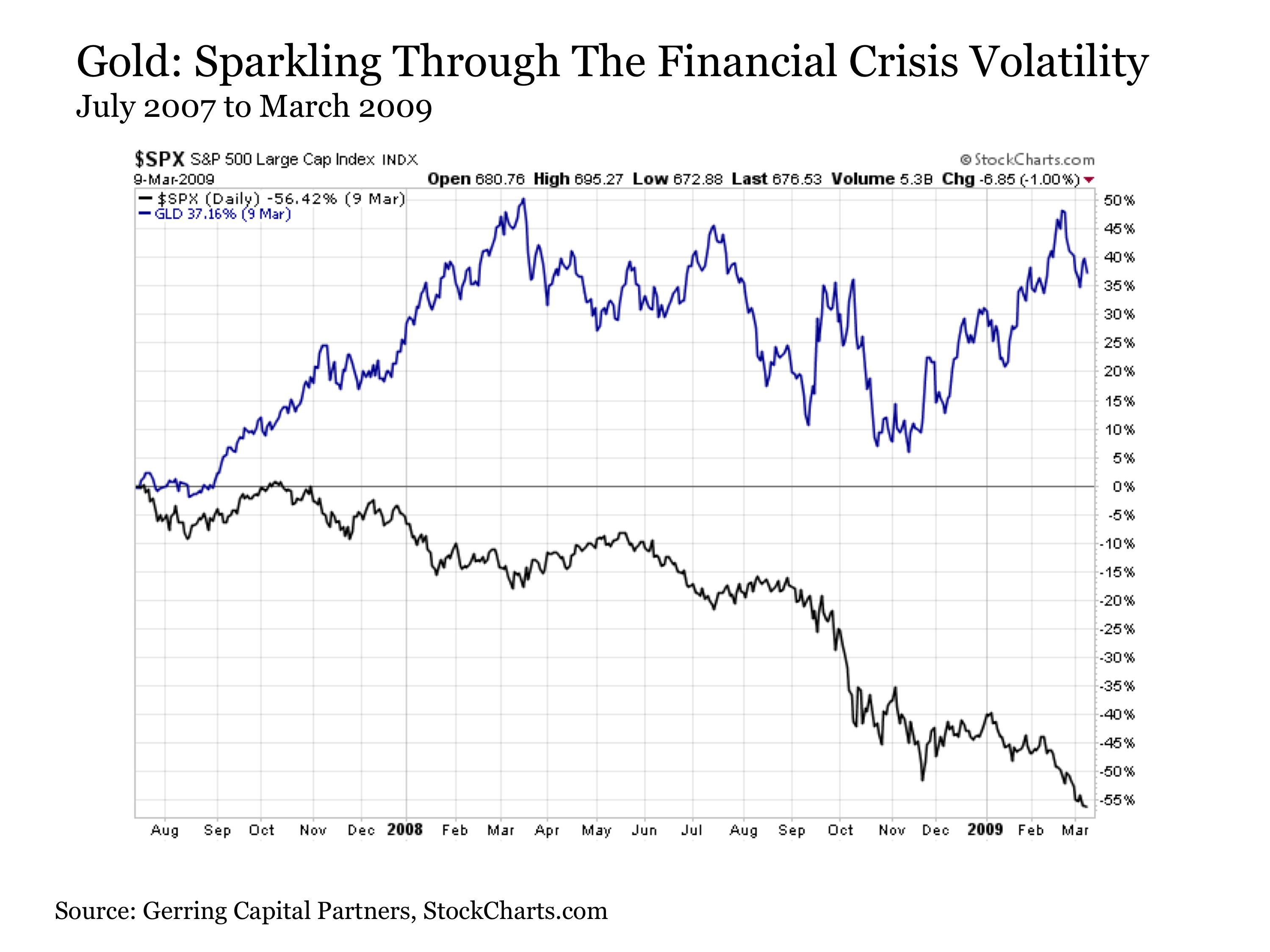

The Red Horse: Gold

During periods of stock market and geopolitical instability including the threat of war, gold (GLD) is an asset class that has demonstrated itself to perform well over time. But in comparison to the other horsemen, it has shown itself to be far wilder in its ways, particularly in recent years. More specifically, it has been a very heavily sentiment driven holding over the last few years and has endured some trading activity that can best be described as notably curious since peaking in late 2011. Moreover, gold like U.S. Treasuries may be subject to short-term liquidation pressures that may add to any sharp price swings along the way. Thus, any investment in the precious metal as a hedge against the stock market should be undertaken with close attention to these risks in mind.

(click to enlarge)

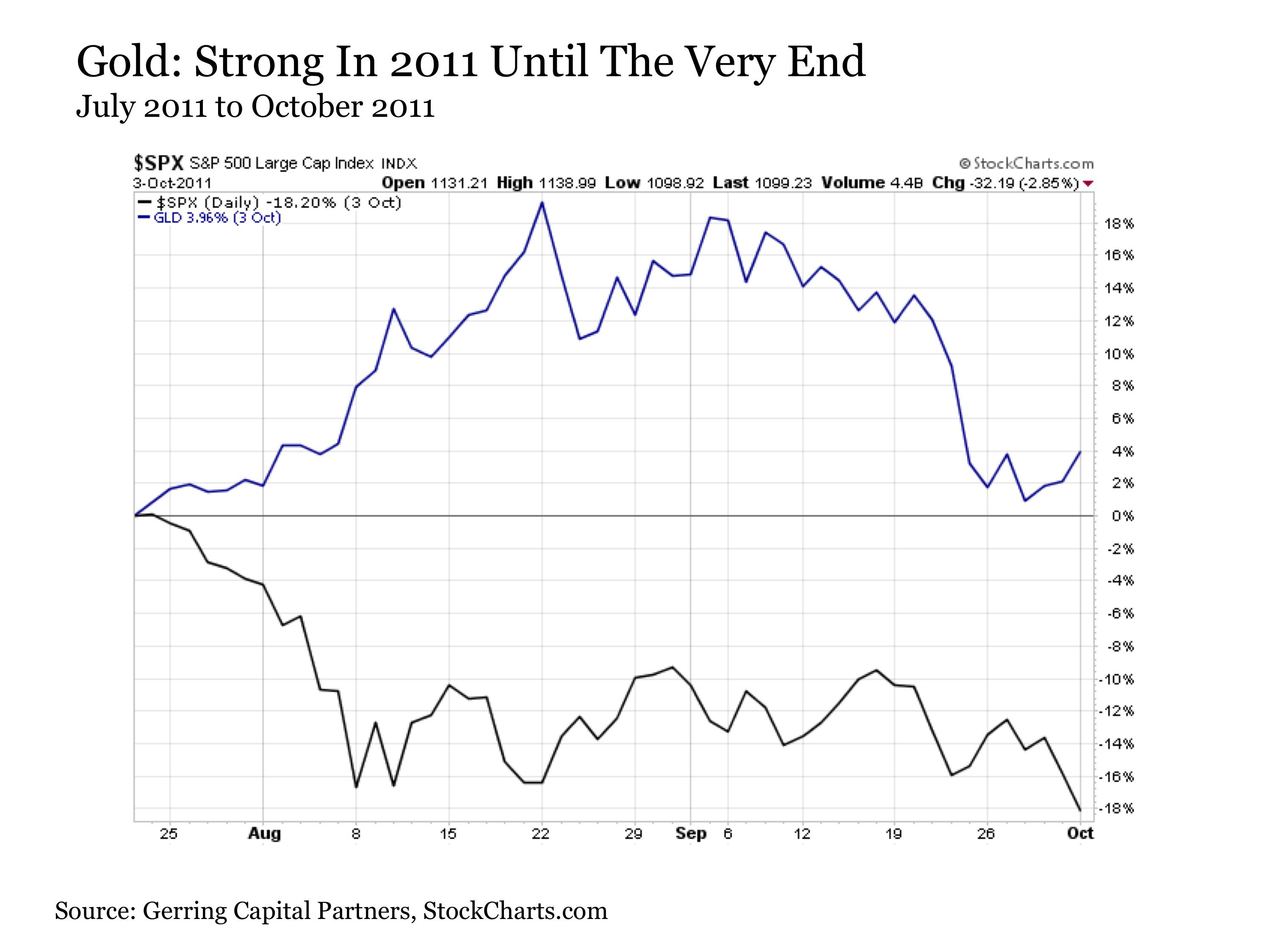

Gold's performance during the stock market correction in 2011 was even more notable, as it advanced by as much as +19% while stocks were falling by -16% over the same time period. These gains remained largely intact until the Fed's official announcement of Operation Twist in late September.

(click to enlarge)

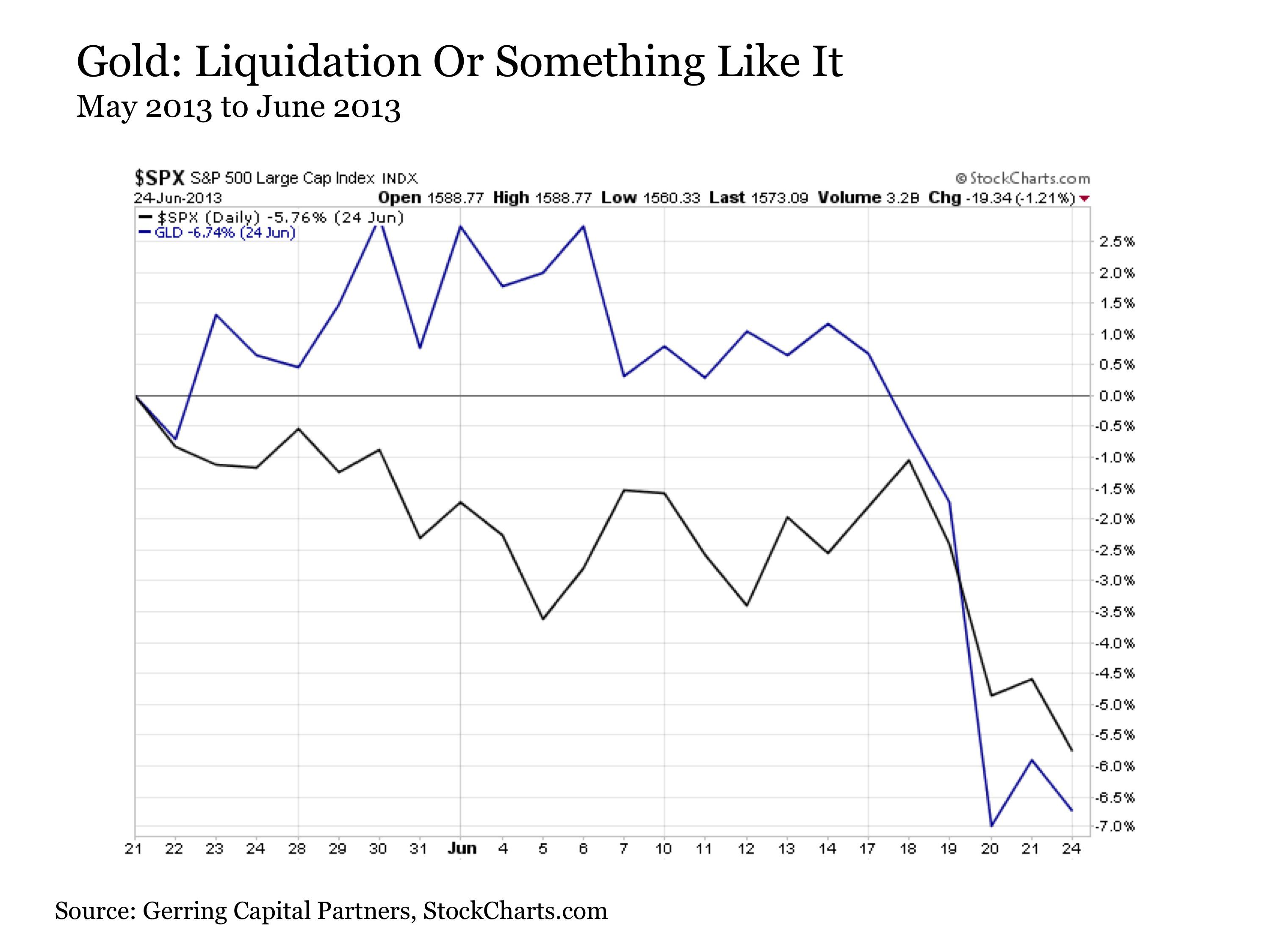

Much like long-term U.S. Treasuries, gold is also exposed to potential liquidation pressures as witnessed during the May 2013 to June 2013 correction. Whether this was the specific reason that sent gold plunging in late June 2013 is subject to debate, but the outcome was the same with gold underperforming U.S. stocks to the downside by the end of this episode.

(click to enlarge)

Again like long-term U.S. Treasuries, gold regained its hedging chops during the most recent stock market correction in late January into early February, advancing by as much as +2% at a time when stocks were falling by -6% to build on its already solid performance thus far in 2014.

In terms of establishing any positions in gold for the purposes of hedging against a stock market decline, offerings such as the Central GoldTrust (GTU) or the Sprott Physical Gold Trust (PHYS) may be worth a look.

The Black Horse: Cash

(click to enlarge)

Of course, holding cash also does not need to be as mundane as it sounds, as the opportunity exists even in this category to generate stock like returns while still hedging against a stock market decline. The key here is exactly what currency in which you decide you hold your cash and suddenly holding cash has been made much more interesting. This is a topic that I will be revisiting in more detail in a separate article in the coming days.

The Pale Horse: Volatility

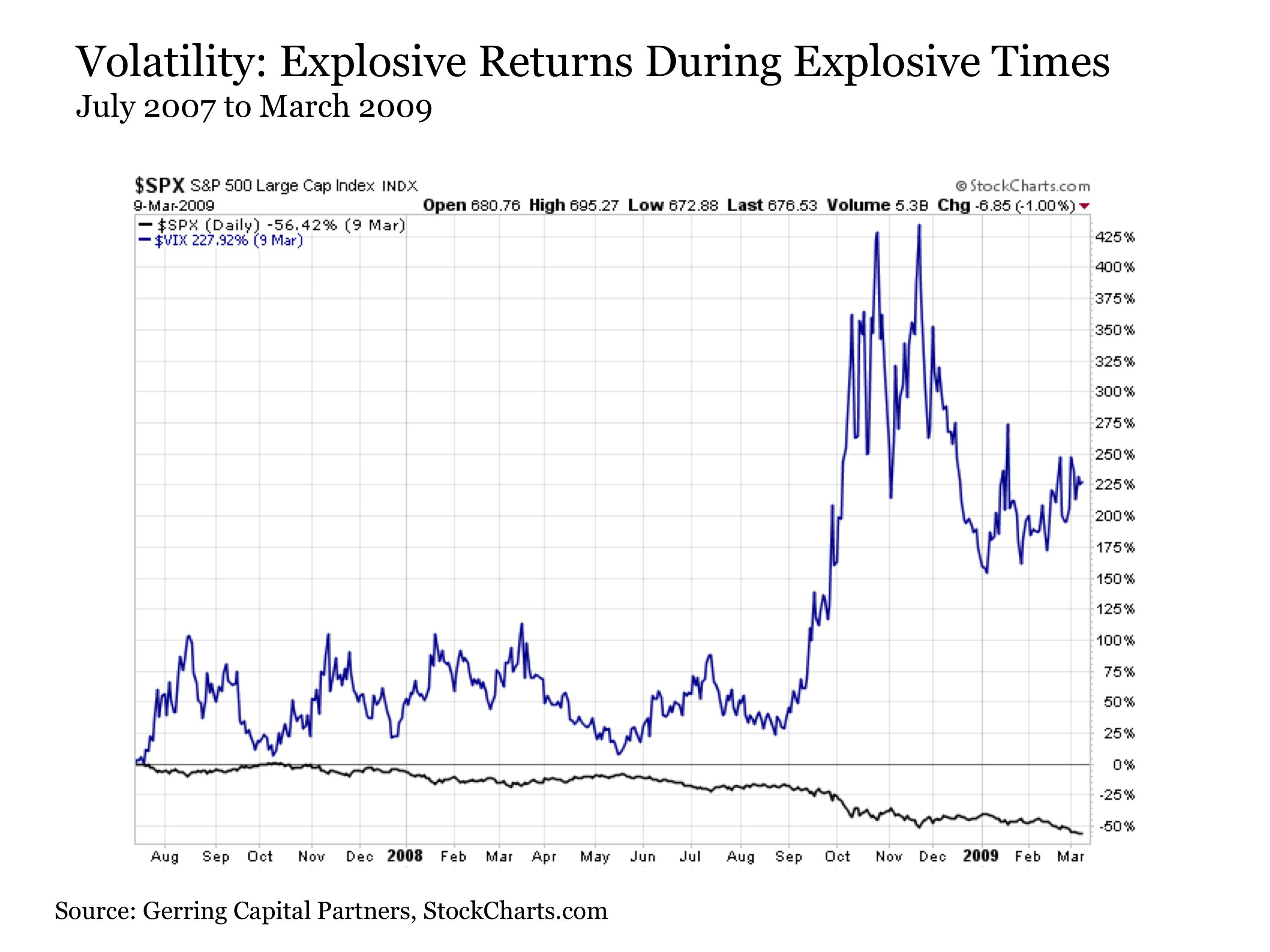

Volatility is the pale rider of capital markets. When most other asset classes including U.S. stocks are facing death, volatility as measured by the CBOE Volatility Index (VIX) is almost always exploding to the upside. And the performance of volatility during recent market corrections highlights the magnitude.During the financial crisis, volatility exploded higher by as much as +430% during the peak stress periods before ending more than three times higher from where it started.

(click to enlarge)

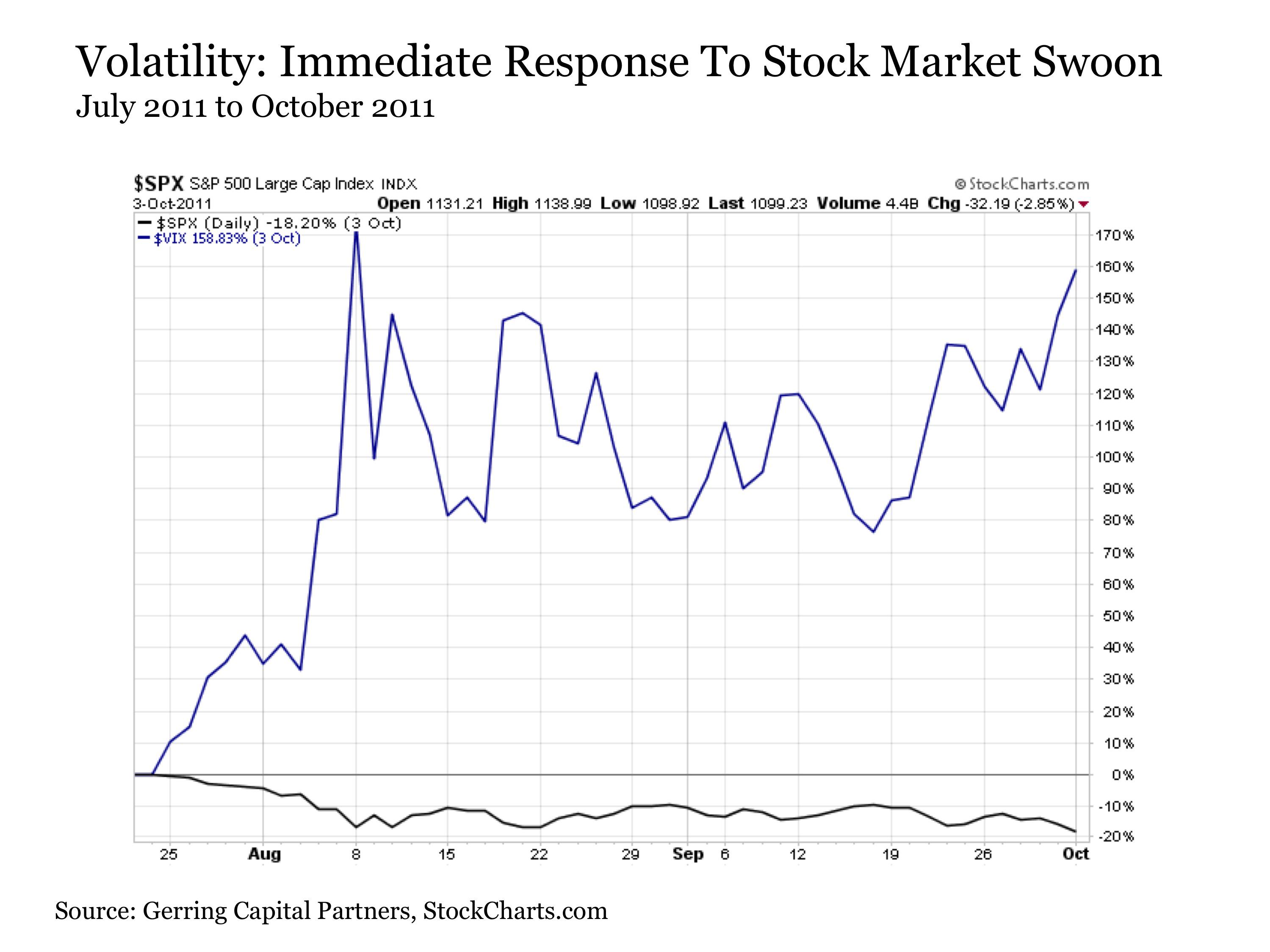

As for the stock market swoon during the summer of 2011, it spiked higher by as much as +170% in less than three weeks when the stock market was plunging lower.

(click to enlarge)

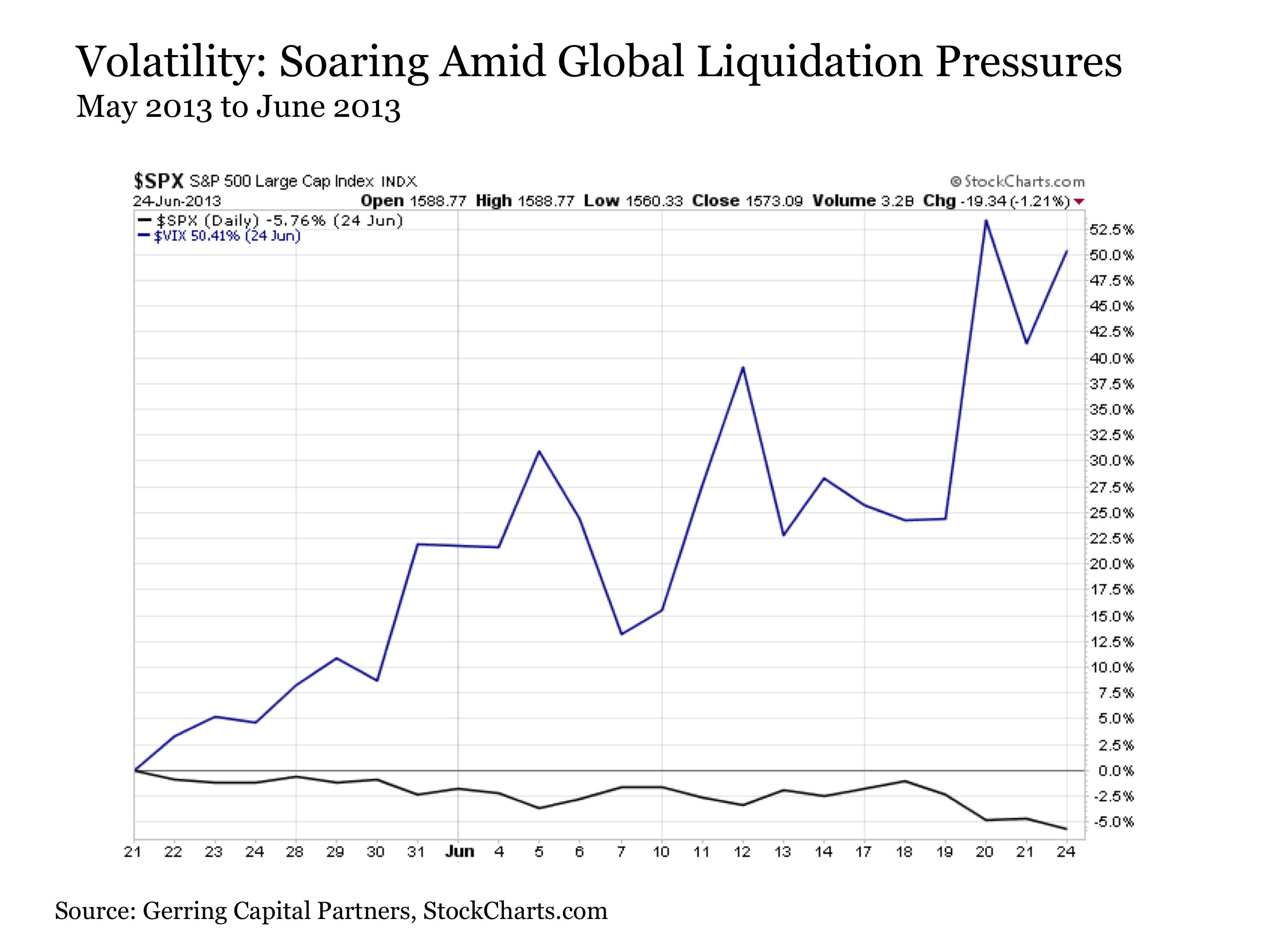

And during the market correction in the spring of 2013 that took the other horses down, the pale rider still pushed higher by +50% over this time period.

(click to enlarge)

These are the good stories associated with volatility. But just like any dealings with the capital market Grim Reaper, this is a category that is not without its extreme risks, challenges and important points of caution.

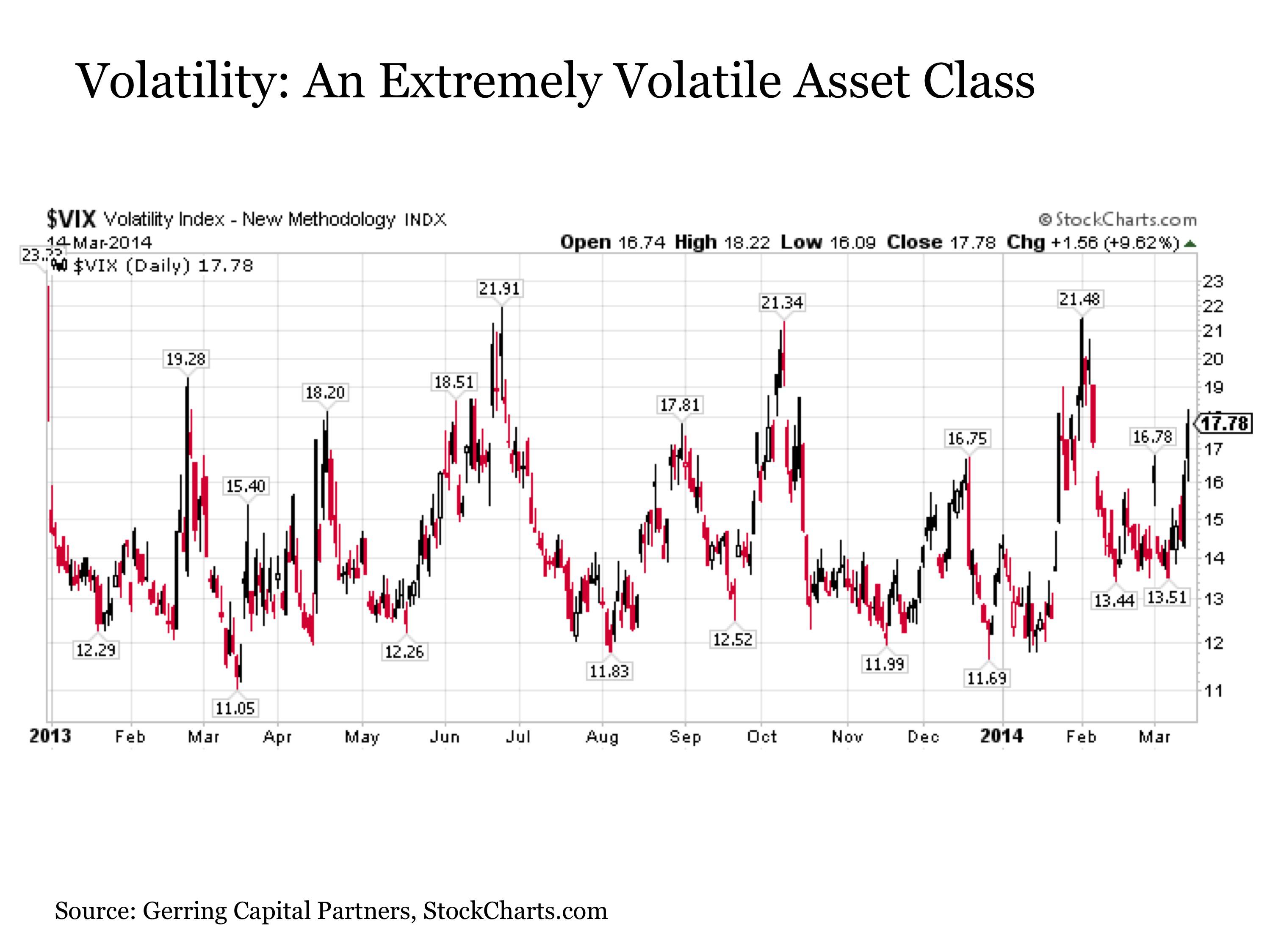

The first point to highlight is that the VIX is extremely volatile. While the gains shown during these periods are more than impressive, the losses incurred by any such positions can be equally devastating if the stock market turns in the other direction.

(click to enlarge)

The second issue associated with the VIX is that one cannot directly invest in it. Exchange traded products such as the iPath S&P 500 VIX Short-Term Futures ETN (VXX) are available that are designed with the intent of tracking the VIX, but these are far from perfect given the limitations associated with how they are constructed. It should be noted that options are another way to gain exposure to volatility.

Lastly and perhaps most importantly, any volatility related positions should be rented, not owned in many cases. In fact, they should be visited briefly instead of even rented. Any position undertaken here should be done with the intent of trying to capture the upside associated with what is believed to be a sudden and sharp move to the downside in stocks. If and when this event has taken place, it is likely in many cases that it will be time to exit the trade to lock in the gains. This principle is not necessarily true when it comes to options, but it is absolutely the case when it comes to many of the volatility related exchange traded products available today.

So when looking ahead to the stock market and the potential for a major market correction along the way, a number of tools are available to not only protect investors against the threat of a stock market correction but also with the ability to capitalize to the upside. I will be revisiting each of these horsemen in more detail in the coming weeks in future articles.

0 comments:

Publicar un comentario