Inflation and interest rates

Up, up and away

Higher inflation may be needed to leave extra-low interest rates behind

Mar 29th 2014

.

AT FIRST glance, rich-world central banks are going their separate ways. Cheered by sturdy growth figures, the Bank of England and the Federal Reserve are shuffling toward an exit from easy monetary policy; markets found Janet Yellen’s first Fed statement unexpectedly hawkish.

The European Central Bank, in contrast, is tacking looser. On March 25th Jens Weidmann, president of the Bundesbank, suggested that the ECB might need to be more forceful in order to keep the euro-area economy out of the grips of deflation.

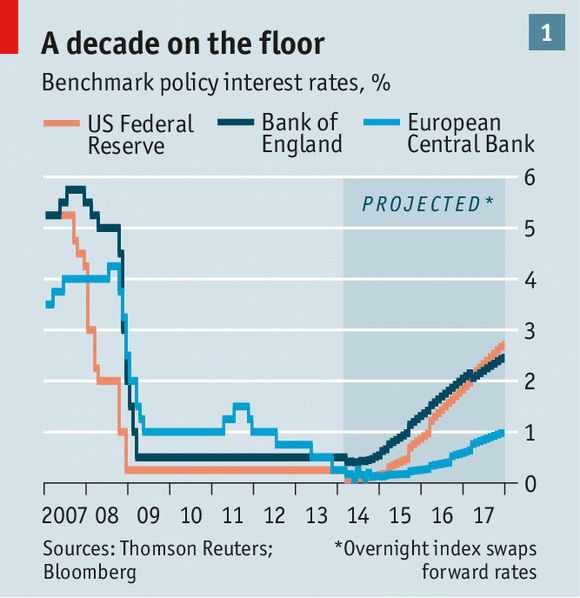

Look again, however, and the path forward appears similar across the rich world: low interest rates stretch off into the visible distance. The outlook is clearest in Europe, where the ECB may toy with negative rates as a means to fend off deflation. But even in America and Britain “normal” rates are a distant prospect. In February Mark Carney, the Bank of England’s governor, promised that eventual rate rises would happen gradually, and would level off below the pre-crisis norm. On March 19th Ms Yellen offered similar guidance. Markets project that short-term rates in both economies will still be just 2% in early 2017 (see chart 1), a level the euro zone will not hit until 2020.

As normalisation recedes toward the horizon, central bankers moan publicly about the costs of low rates. In February Daniel Tarullo, a Fed governor, said that they might encourage investors to take dangerous risks as they “reach for yield”. Even more worrying, low rates leave little cushion against future shocks. The Fed’s main policy rate was just 2% when Lehman Brothers failed in 2008, compared with 5% at the start of the 2001 recession and 8% when the downturn of 1990 began.

Yet rates are low for good reason: economies cannot withstand dearer credit. Central banks are battling against two sources of downward pressure on their main policy rates. One is the rock-bottom level of the real (ie, inflation-adjusted) interest rate needed to keep economies running at full tilt. This “natural” rate has been dragged down by long-term structural trends. A global savings glut is partly to blame: export powerhouses like the OPEC countries and China buy vast quantities of rich-world debt, depressing borrowing costs in the process. Rising inequality also adds to the pool of underused savings, since the rich save more of their income. Leaden real rates were reinforced by the financial crisis. Tumbling asset prices forced households to repay debts rapidly. As they struggled to deleverage, their interest in new borrowing and spending evaporated.

0 comments:

Publicar un comentario