American banks

A harsh light

A handful of banks are caught short by the Fed’s annual stress test

Mar 29th 2014

New York

.

THE current mood in America’s financial markets is enthusiasm for companies that can receive investment now with the prospect of using it to make more in the future. The exceptions are banks, for whom the ability to return capital now rather than later is seen as a critical indicator of health. On March 26th the Federal Reserve disclosed the results of its “comprehensive capital analysis and review” determining which of the country’s 30 largest banks could increase their dividends and share buybacks.

The precise criteria are deliberately kept murky to stop banks gaming them, and the results produced some shocks. Most banks had their plans approved but Citigroup and the American operations of HSBC, RBS Citizens and Santander were all rejected while Goldman Sachs and Bank of America passed only by tweaking their submissions. One other institution, Zions Bancorporation, had its plan rejected as well but this had been expected because it had flunked an earlier stage of the test.

For Citi, the results were a disaster. Its shares fell 6% in after-market trading. “We are deeply disappointed”, said Michael Corbat, its chief executive.

Sympathy may be scarce. Mike Mayo, a provocative analyst at CLSA, a stockbroker, urged that someone be held accountable. It is Citi’s second failure. The previous one created the vacancy for Mr Corbat’s current job.

In an 87-page release, the Fed spelled out its objections. In Citi’s case, these included “deficiencies” that had been identified previously, including insufficient ability to produce models on the impact on revenues and losses for “material parts of the firm’s global operations”. HSBC, RBS Citizens and Santander, which were included in the test for the first time, were granted some leeway but were nonetheless still found to have inadequate governance and capacity to evaluate risk.

Zions, Goldman Sachs and Bank of America were all judged to have inadequate capital in the case of a severe crunch under their original plans but Goldman and Bank of America were dexterous and informed enough to make adjustments. Why others did not do the same raises questions about both their regulatory ties and the evaluation process.

HSBC issued a statement suggesting it was surprised by the result, noting that it had done particularly well in the first evaluation based on its current capital position, and that it had been working closely with regulators. If its failure serves any purpose, it is to highlight that regulators seem to keep shifting the goalposts.

Part of the test is based on numbers drawn from a hypothetical crisis such as a 50% drop in the stockmarket and 25% drop in housing prices, along with a sharp increase in unemployment. But new facets of the test go beyond numbers to look at operations. “It is clear standards are being ratcheted up, and the most important part is qualitative—the assessment of the bank’s ability to evaluate its own risks”, said Til Schuermann, a partner at Oliver Wyman, a consulting firms.

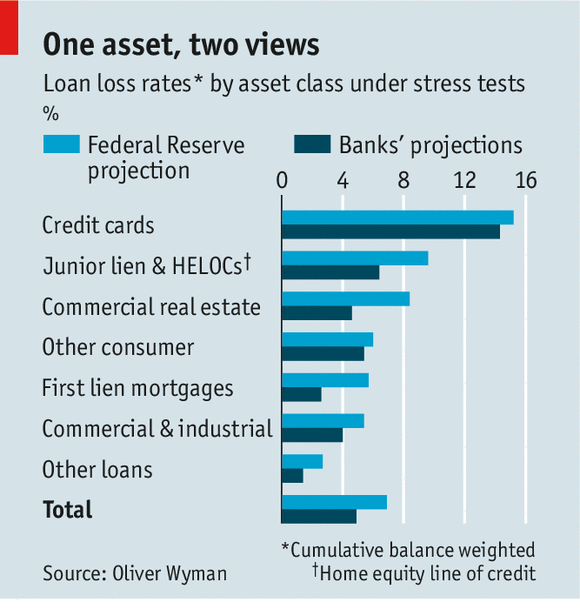

In response to the Fed’s results, 28 of the banks released their own expectations of what would unfold in a crisis. An analysis by Oliver Wyman (see chart) showed that banks and regulators agree that credit cards will suffer the most severe losses, and their estimates are similar. There are, however, sharp divergences elsewhere, particularly property. Banks reckon the impact will only be one-third to one-half as severe as the Fed believes.

Stress tests of the sort imposed in America are influential elsewhere, with regulators in London and Frankfurt keen to emulate them. Yet many in the banks themselves believe they provide only an illusion of safety. Revenue projections, for example, are now required for the evaluation. These numbers are essential for internal planning but are inherently squishy. Requiring them may do nothing for accuracy. The tests may also have a large impact on the opportunities banks pursue. At some point, the tests not only evaluate, they manage. That is a risk in itself.

THE current mood in America’s financial markets is enthusiasm for companies that can receive investment now with the prospect of using it to make more in the future. The exceptions are banks, for whom the ability to return capital now rather than later is seen as a critical indicator of health. On March 26th the Federal Reserve disclosed the results of its “comprehensive capital analysis and review” determining which of the country’s 30 largest banks could increase their dividends and share buybacks.

The precise criteria are deliberately kept murky to stop banks gaming them, and the results produced some shocks. Most banks had their plans approved but Citigroup and the American operations of HSBC, RBS Citizens and Santander were all rejected while Goldman Sachs and Bank of America passed only by tweaking their submissions. One other institution, Zions Bancorporation, had its plan rejected as well but this had been expected because it had flunked an earlier stage of the test.

For Citi, the results were a disaster. Its shares fell 6% in after-market trading. “We are deeply disappointed”, said Michael Corbat, its chief executive.

Sympathy may be scarce. Mike Mayo, a provocative analyst at CLSA, a stockbroker, urged that someone be held accountable. It is Citi’s second failure. The previous one created the vacancy for Mr Corbat’s current job.

In an 87-page release, the Fed spelled out its objections. In Citi’s case, these included “deficiencies” that had been identified previously, including insufficient ability to produce models on the impact on revenues and losses for “material parts of the firm’s global operations”. HSBC, RBS Citizens and Santander, which were included in the test for the first time, were granted some leeway but were nonetheless still found to have inadequate governance and capacity to evaluate risk.

Zions, Goldman Sachs and Bank of America were all judged to have inadequate capital in the case of a severe crunch under their original plans but Goldman and Bank of America were dexterous and informed enough to make adjustments. Why others did not do the same raises questions about both their regulatory ties and the evaluation process.

HSBC issued a statement suggesting it was surprised by the result, noting that it had done particularly well in the first evaluation based on its current capital position, and that it had been working closely with regulators. If its failure serves any purpose, it is to highlight that regulators seem to keep shifting the goalposts.

Part of the test is based on numbers drawn from a hypothetical crisis such as a 50% drop in the stockmarket and 25% drop in housing prices, along with a sharp increase in unemployment. But new facets of the test go beyond numbers to look at operations. “It is clear standards are being ratcheted up, and the most important part is qualitative—the assessment of the bank’s ability to evaluate its own risks”, said Til Schuermann, a partner at Oliver Wyman, a consulting firms.

In response to the Fed’s results, 28 of the banks released their own expectations of what would unfold in a crisis. An analysis by Oliver Wyman (see chart) showed that banks and regulators agree that credit cards will suffer the most severe losses, and their estimates are similar. There are, however, sharp divergences elsewhere, particularly property. Banks reckon the impact will only be one-third to one-half as severe as the Fed believes.

Stress tests of the sort imposed in America are influential elsewhere, with regulators in London and Frankfurt keen to emulate them. Yet many in the banks themselves believe they provide only an illusion of safety. Revenue projections, for example, are now required for the evaluation. These numbers are essential for internal planning but are inherently squishy. Requiring them may do nothing for accuracy. The tests may also have a large impact on the opportunities banks pursue. At some point, the tests not only evaluate, they manage. That is a risk in itself.

0 comments:

Publicar un comentario