Three big macro questions for 2014

by Gavyn Davies

December 30, 2013 2:10 pm

As we enter 2014, the five-year bull market in developed market equities remains in full swing. Recently, I argued that equities now look overvalued, but not egregiously so, and that the future of the bull market could depend on when the level of global GDP started to bump up against supply side constraints, forcing a genuine tightening in global monetary conditions.

Today, this blog offers a year end assessment of three crucial issues that relate to this: the supply side in the US; China’s attempt to control its credit bubble; and the ECB’s belief that there is no deflation threat in the euro area. At least one of these questions is likely to be the defining macro issue of 2014 and beyond.

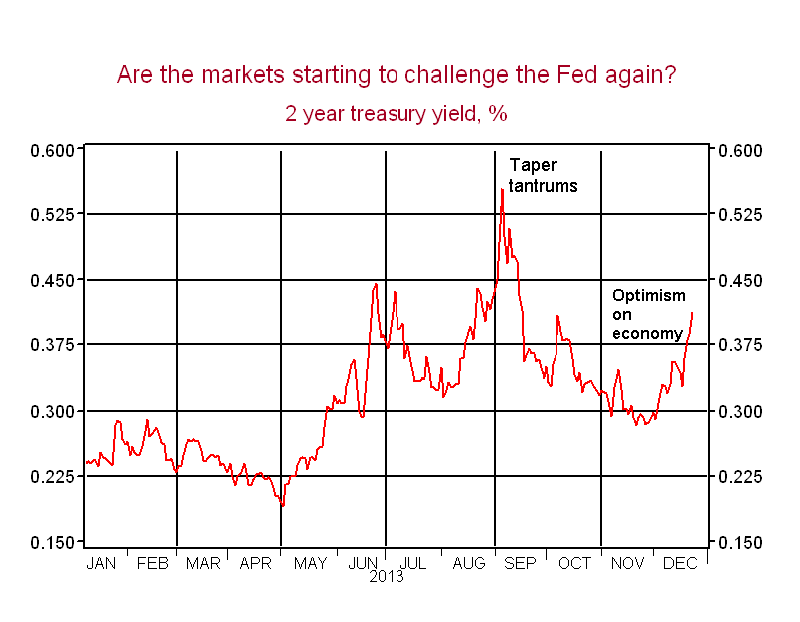

1. When will the Fed start to worry about supply constraints in the US?

Until now, the main worry in the US has been that demand would be inadequate to generate an acceptable rate of GDP growth, given the 1.5 per cent of GDP tightening in American fiscal policy in 2013. But now this seems to be changing. The US fiscal stance will tighten by only 0.4 per cent of GDP this year, and GDP growth is widely expected to exceed 3 percent, well above the current CBO estimate of about 2 per cent for the growth in potential output.

Many economists are suggesting that potential output, or “supply”, has been at least temporarily depressed by the effects of the recession, via early retirement of unemployed workers, and low levels of capital spending. In fact, the distinction between the aggregate demand (AD) and supply (AS) sides of the economy has become increasingly confused.

This development has dismayed Keynesian economists like Paul Krugman, who argue that it is still critical to retain a clear analytic distinction between the AD and AS curves. Most economists of my generation, trained during the stagflationary 1970s, strongly agree with them on this point. Paul’s camp also believes that, in the long run, supply potential will prove to be a very long way above the present level of GDP.

The CBO estimates that potential GDP is about 6 percent above the actual level of output. This of course implies that the Fed could afford to delay the initial rise in short rates well beyond the 2015 timescale that the vast majority of FOMC participants now deem likely. The very low and falling rates of inflation in the developed world certainly support this.

But the suspicion that labour force participation, and therefore supply potential, may have been permanently damaged by the recession is gaining ground in some unexpected parts of the Fed, and the unemployment rate is likely to fall below the 6.5 percent threshold well before the end of 2014 (see Tim Duy’s terrific blog on this here)

This is the nub of the matter: will Janet Yellen’s Fed want to delay the initial rate rise beyond the end of 2015, and will they be willing to fight the financial markets whenever the latter try to price in earlier rate hikes, as they did in summer 2013? I believe the answer to both these questions is “yes”, but there could be several skirmishes on this front before 2014 is over. Indeed, the first may be happening already.

2. Will China bring excess credit growth under control?

Everyone now agrees that the long run growth rate in China has fallen from the heady days when it exceeded 10 per cent per annum, but there are two very different views about where it is headed next. The optimistic version, exemplified by John Ross’ widely respected blog, is that China has been right to focus on capital investment for several decades, and that this will remain a successful strategy. John points out that, in order to hit the official target of doubling real GDP between 2010 and 2020, growth in the rest of this decade can average as little as 6.9 per cent per annum, which he believes is comfortably within reach, while the economy is simultaneously rebalanced towards consumption. This would constitute a very soft landing from the credit bubble.

The pessimistic view is well represented by Michael Pettis’ writing, which has been warning for several years that the re-entry from the credit bubble would involve a prolonged period of growth in the 5 per cent region at best. Repeated attempts by the authorities to rein in credit growth have had to be relaxed in order to maintain GDP growth at an acceptable rate, suggesting that there is a conflict between the authorities’ objective to allow the market to set interest rates, and the parallel objective to control the credit bubble without a hard landing.

As I argued recently, there is so far no sign that credit growth has dropped below the rate of nominal GDP growth, and the bubble-like increases in housing and land prices are still accelerating. The optimistic camp on China’s GDP has been more right than wrong so far, and a prolonged soft landing still seems to be the best bet, given China’s unique characteristics.

But the longer it takes to bring credit under control, the greater the chance of a much harder landing.

3. Will the ECB confront the zero lower bound?

Whether it should be described as secular stagnation or Japanification, the euro area remains mired in a condition of sluggish growth and sub-target inflation that will be worsened by the latest bout of strength in the exchange rate. Mario Draghi said this week that

This does not seem fully consistent with the ECB’s inflation target of “below but close to 2 per cent”. Meanwhile, the Bundesbank has just published a paper which confidently denies that there is any risk of deflation in the euro area, and says that declining unit labour costs in the troubled economies are actually to be welcomed as signs that the necessary internal rebalancing within the currency zone is taking place.

The markets will probably be inclined to accept this, as long as the euro area economy continues to recover. This seems likely in the context of stronger global growth.

But a further rise in the exchange rate could finally force the ECB to confront the zero lower bound on interest rates, as the Fed and others have done in recent years. Mr Draghi has repeatedly shown that he has the ability to navigate the tricky politics that would be involved here, but a pre-emptive strike now seems improbable. In fact, he might need a market crisis to concentrate some minds on the Governing Council.

So there we have the three great issues in global macro, any one of which could take centre stage in the year ahead. For what it is worth, China currently seems to me by far the most worrying.

Today, this blog offers a year end assessment of three crucial issues that relate to this: the supply side in the US; China’s attempt to control its credit bubble; and the ECB’s belief that there is no deflation threat in the euro area. At least one of these questions is likely to be the defining macro issue of 2014 and beyond.

1. When will the Fed start to worry about supply constraints in the US?

Until now, the main worry in the US has been that demand would be inadequate to generate an acceptable rate of GDP growth, given the 1.5 per cent of GDP tightening in American fiscal policy in 2013. But now this seems to be changing. The US fiscal stance will tighten by only 0.4 per cent of GDP this year, and GDP growth is widely expected to exceed 3 percent, well above the current CBO estimate of about 2 per cent for the growth in potential output.

Many economists are suggesting that potential output, or “supply”, has been at least temporarily depressed by the effects of the recession, via early retirement of unemployed workers, and low levels of capital spending. In fact, the distinction between the aggregate demand (AD) and supply (AS) sides of the economy has become increasingly confused.

This development has dismayed Keynesian economists like Paul Krugman, who argue that it is still critical to retain a clear analytic distinction between the AD and AS curves. Most economists of my generation, trained during the stagflationary 1970s, strongly agree with them on this point. Paul’s camp also believes that, in the long run, supply potential will prove to be a very long way above the present level of GDP.

The CBO estimates that potential GDP is about 6 percent above the actual level of output. This of course implies that the Fed could afford to delay the initial rise in short rates well beyond the 2015 timescale that the vast majority of FOMC participants now deem likely. The very low and falling rates of inflation in the developed world certainly support this.

But the suspicion that labour force participation, and therefore supply potential, may have been permanently damaged by the recession is gaining ground in some unexpected parts of the Fed, and the unemployment rate is likely to fall below the 6.5 percent threshold well before the end of 2014 (see Tim Duy’s terrific blog on this here)

This is the nub of the matter: will Janet Yellen’s Fed want to delay the initial rate rise beyond the end of 2015, and will they be willing to fight the financial markets whenever the latter try to price in earlier rate hikes, as they did in summer 2013? I believe the answer to both these questions is “yes”, but there could be several skirmishes on this front before 2014 is over. Indeed, the first may be happening already.

2. Will China bring excess credit growth under control?

Everyone now agrees that the long run growth rate in China has fallen from the heady days when it exceeded 10 per cent per annum, but there are two very different views about where it is headed next. The optimistic version, exemplified by John Ross’ widely respected blog, is that China has been right to focus on capital investment for several decades, and that this will remain a successful strategy. John points out that, in order to hit the official target of doubling real GDP between 2010 and 2020, growth in the rest of this decade can average as little as 6.9 per cent per annum, which he believes is comfortably within reach, while the economy is simultaneously rebalanced towards consumption. This would constitute a very soft landing from the credit bubble.

The pessimistic view is well represented by Michael Pettis’ writing, which has been warning for several years that the re-entry from the credit bubble would involve a prolonged period of growth in the 5 per cent region at best. Repeated attempts by the authorities to rein in credit growth have had to be relaxed in order to maintain GDP growth at an acceptable rate, suggesting that there is a conflict between the authorities’ objective to allow the market to set interest rates, and the parallel objective to control the credit bubble without a hard landing.

As I argued recently, there is so far no sign that credit growth has dropped below the rate of nominal GDP growth, and the bubble-like increases in housing and land prices are still accelerating. The optimistic camp on China’s GDP has been more right than wrong so far, and a prolonged soft landing still seems to be the best bet, given China’s unique characteristics.

But the longer it takes to bring credit under control, the greater the chance of a much harder landing.

3. Will the ECB confront the zero lower bound?

Whether it should be described as secular stagnation or Japanification, the euro area remains mired in a condition of sluggish growth and sub-target inflation that will be worsened by the latest bout of strength in the exchange rate. Mario Draghi said this week that

We are not seeing any deflation at present… but we must take care that we don’t have inflation stuck permanently below one percent and thereby slip into the danger zone.

This does not seem fully consistent with the ECB’s inflation target of “below but close to 2 per cent”. Meanwhile, the Bundesbank has just published a paper which confidently denies that there is any risk of deflation in the euro area, and says that declining unit labour costs in the troubled economies are actually to be welcomed as signs that the necessary internal rebalancing within the currency zone is taking place.

The markets will probably be inclined to accept this, as long as the euro area economy continues to recover. This seems likely in the context of stronger global growth.

But a further rise in the exchange rate could finally force the ECB to confront the zero lower bound on interest rates, as the Fed and others have done in recent years. Mr Draghi has repeatedly shown that he has the ability to navigate the tricky politics that would be involved here, but a pre-emptive strike now seems improbable. In fact, he might need a market crisis to concentrate some minds on the Governing Council.

So there we have the three great issues in global macro, any one of which could take centre stage in the year ahead. For what it is worth, China currently seems to me by far the most worrying.

0 comments:

Publicar un comentario