Free exchange

This time is worse

Leading American economists argue that desperate times call for desperate measures

Jan 11th 2014

ON JANUARY 2nd Philadelphia was not only blanketed with four to six inches of snow, but five to six feet of economists. Almost 12,000 descended on the City of Brotherly Love to attend the annual meeting of the American Economic Association. If the chill in the air failed to dampen their spirits, it seemed to tinge the outlook of many presentations. Financial markets may have rung in 2014 with high hopes, but macroeconomists spy danger as far as the eye can see.

The worst of the recessions that followed the subprime mess may be over. But the economists gathered in Philadelphia insisted on pointing out that its legacy remains, in the form of huge debt loads, uncompetitive economies and high levels of unemployment.

Across advanced economies debts stand at post-war highs, according to—presumably triple-checked—figures presented by Carmen Reinhart and Kenneth Rogoff of Harvard University. Those debts, they say, appear to be constraining recovery, blunting monetary expansion and limiting the political appeal of fiscal stimulus. And stubborn economic weakness has turned the European periphery’s woes into one of the most miserable episodes in modern economic history.

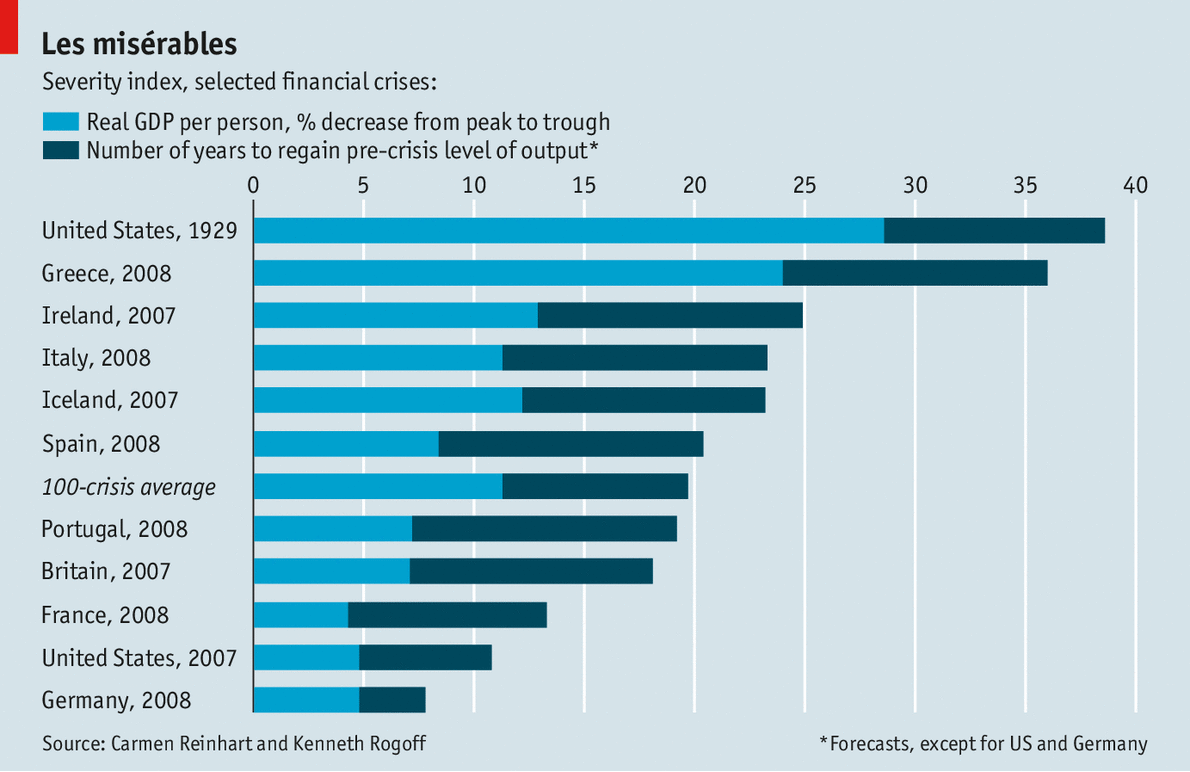

Before the latest crisis Ms Reinhart and Mr Rogoff began building a database of financial crashes and their aftermath. Their work, gathered in “This Time Is Different” (2009), concluded that recoveries after financial crises are commonly weaker and more protracted than those after other recessions. Even so, the post-subprime era stands out.

Ms Reinhart and Mr Rogoff considered 100 of the most severe crises of the past 200 years. For each recovery they calculated the depth of the drop in output per person, adjusted for inflation, from the pre-crisis peak to its lowest point. They also totted up the time it took for output per person to return to the previous peak. They define this point as full “recovery”, even though qualifying economies may then produce well below the level of output per person expected before the crisis. America’s real output per person, for instance, is back above the pre-crisis peak, meeting the standard for recovery. Yet it remains about 9% (or roughly $5,000 per person) below the trendline expected in 2001.

Adding together the depth of the downturn and time until recovery, Ms Reinhart and Mr Rogoff calculate a “severity index”. Across the 100 cases the average decline in output per person from the pre-crisis level is 11.3% and recovery takes an average of 8.4 years, resulting in a severity score of 19.7 (see chart).

America’s Depression of the 1930s had a severity score of 38.6—the 13th-worst of the 100 in the sample. Crisis gold goes to Chile in 1926 with a score of 62.6, silver to Spain in 1931 with 60.6 and bronze to Peru in 1983 with 57. As for Greece, if one assumes, somewhat optimistically, that 2013 marked the absolute bottom for real output per person and that output will recover to the pre-crisis level by 2019, then its severity score will come in at 36.

In Europe the recent crises in Ireland, Italy, Iceland and Ukraine were also among the 35 worst, and could become even more egregious if output takes longer than expected to return to the pre-crisis level. Europe’s double-dip downturn, in which close to half of its economies fell back into contraction before recovering fully, did not help.

America’s crisis was mild by comparison. With a drop in output of 4.8% and a time of six years to recovery, its severity score is 10.8. Together with Germany, it is the only country that in the Reinhart-Rogoff sense has officially recovered. Still, America experienced easily its worst downturn since the second world war.

Ms Reinhart and Mr Rogoff argue that, in overall severity, the rich world’s recent round of crises more closely resembles the economic downturns of the 19th and early 20th centuries. For that reason, they say, governments should consider taking a more eclectic range of economic measures than have been the norm over the past generation or two. The policies put in place so far, such as budgetary austerity, are little match for the size of the problem, they argue, and may make things worse.

Instead, governments should take stronger action, much as rich economies did in past crises up to and including the immediate aftermath of the second world war and as, more recently, developing countries have done. Ms Reinhart and Mr Rogoff suggest debt write-downs and “financial repression”, meaning the use of a combination of moderate inflation and constraints on the flow of capital to reduce debt burdens.

The Great U-turn

Hans-Werner Sinn of the University of Munich reckoned that since Germans will not consent to the use of higher inflation to ease European rebalancing, several euro-area economies need to leave the single currency, at least temporarily. And Larry Summers of Harvard University acknowledged that higher inflation might propel the American economy out of “secular stagnation”, but suggested that an ambitious five-year programme of public investment would be better.

In short, a huge U-turn was in evidence amid the snow of Philadelphia. Before the crisis the talk among macroeconomists was all about the Great Moderation and the primacy of keeping inflation low. Now it is all about the Great Recession—and the possibility that a bit more inflation might just help.

0 comments:

Publicar un comentario