Is The Gold Market Manipulated? Part 3: The Beginning Of Modern-Day Suppression

Dec. 23, 2013 9:36 AM ET

In part 1 I introduced the reader to the concept of market manipulation. I exposed the nonsensical definition offered by the CFTC and proposed my own alternative as follows:

Manipulation occurs when:

A: A market participant buys and/or sells an asset or a derivative contract related to that asset in order to control its price.

B: The participant does so in order to achieve some agenda other than directly profiting from the aforementioned trading activity.

I then provided irrefutable evidence, given these conditions, of manipulation of the gold market from 1961 through 1968 by a consortium of eight central banks through what is called the London Gold Pool (LGP, here on). I provided the reader with statements from central bankers, most notably Arthur Coombs, that show that there was an intent to manipulate the gold price so that it remained at $35/ounce despite upward pressures, and that show that there was, in fact, market activity designed to maintain the $35/ounce price level.

In part 2 I showed that gold market manipulation did not end with the LGP. While there was no direct effort to peg the market at a fixed dollar level, I demonstrate that top U.S. officials, both from economic and political realms, were concerned with the price of gold, and they feared losing their control over the gold market and ultimately their dominant role on the global political and monetary stages.

American officials were acutely aware that the "golden rule" (i.e. he who has the gold makes the rules) was in effect, and since the U.S. lost most of its gold attempting to maintain the price at $35/ounce in the 1950s and 1960s, these officials acted upon a corollary of the golden rule: if you don't have the gold but want to make the rules, then undermine the golden rule. Documentation links this perspective to top officials at the CIA and the State Department. As a result the Federal Reserve, led by Arthur Burns, put forward a de-monetization agenda, whereby it convinced the most important global central banks (predominantly in continental Europe) not to buy gold, and to in fact sell gold in an attempt to undermine its importance in the global monetary system. The IMF also sold gold in this de-monetization effort.

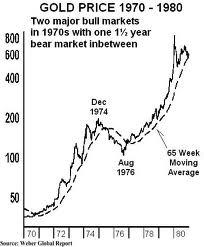

Nevertheless the gold price rose dramatically, having gone from about $40/ounce at the beginning of the decade (despite the "official" price of $35/ounce) to a peak of $850/ounce in 1980.

One can conclude from this that while central banks attempted to undermine gold's monetary significance through policy maneuvers and market intervention, this significance was not lost in the market, as it revealed the incredible de-valuation of the dollar that had taken place since the price of gold was first fixed at $35/ounce in 1933.

Here I look at the bear market era in gold, and in particular the latter stages of this era. During the latter stages of this era we see signs of price suppression similar to those found during the LGP era and during the de-monetization efforts of the 1970s. We see new signs such as acute price drops going into the London PM Fix on a regular basis.

Furthermore, we see a rise in the use of gold-related derivatives and we find central banker statements that effectively admit that such derivatives are being used to clandestinely suppress or manage the gold price. Beyond this admission we see transparent attempts to underplay the role of derivatives in affecting the gold price through dissemination and propaganda. Finally, in what appears to be a last resort effort to keep gold prices from rising we find gold sales announced prior to the actual sales, which implicitly means that the sellers were motivated by reasons other than profit.

In all there are no clear-cut documents such as the Coombs' article that give a step-by-step road map of market activity and its justification in the context of the broader agenda of suppressing the gold price. This makes demonstrating gold price suppression that much more difficult, and where there is room for "reasonable doubt" I will point this out to the reader.

However, in the context of what we have seen in parts 1 and 2, what we find as evidence of manipulation in the 1990's comes across as more of the same, and not an anomaly that can be explained away as a series of coincidences. Thus in what follows I make what appear to be extraordinary claims based upon seemingly flippant mentions of gold and related derivatives; and given the well-established history of gold price suppression, gold price pegging, and the importance of gold in the developments of politics and money in the 20th century, it should be clear to the reader that I am justified in doing so.

The Fundamental Bear Market In Gold

Comments made in response to my previous two articles have insinuated that my outcries of manipulation were spurned by frustration in the wake of gold's ongoing cyclical bear market, and that I was equating a sinking market with manipulation. However throughout much of the yellow metal's secular bear market, there was likely little to no intervention--intervention over the past 50 years or so has occurred mostly in flat and rising markets. While the bear market begins in 1980 and ends in 1999, there is no clear evidence of price suppression until the early to mid 1990's. Furthermore it seems that political authorities and central bankers had forgotten about gold as there is conspicuously little mention of it in documents where gold was a common topic of discussion in prior years (e.g. FOMC minutes).

The truth of the matter is that there was no need for central bankers to intervene in the gold market in order to drive its price lower--there were many fundamental factors that came into play that led to a substantial bear market.

Let us look briefly at the bear market in gold.

After the 1970's bull market gold began a lengthy bear market that lasted until 1999. As with all assets, in this bear market the gold price went from an overvalued $850/ounce to a state of undervaluation at $255/ounce in 1999. While the bear market reflects a 70% nominal decline in the gold price, one has to bear in mind that the money supply using all possible measures continued to rise while U.S. gold reserves remained constant at roughly 8,100 tons.

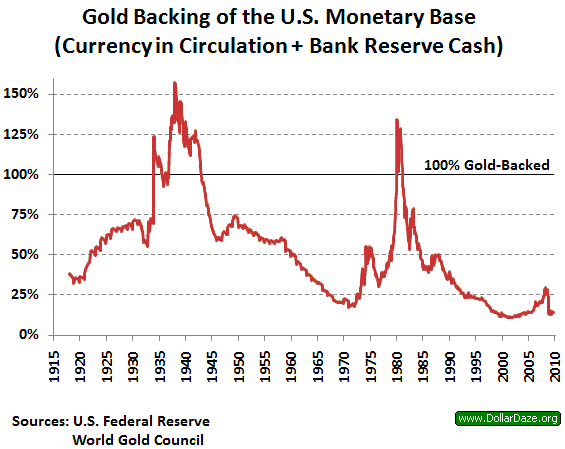

To see the real damage of the bear market it is useful to look at U.S. gold reserves vs. the money supply. If we look at the market value of U.S. gold reserves in terms of the monetary base, we see that the market peaked at around the same level that it reached when the price was first set at $35/ounce in 1933--about 125%.

(click to enlarge)

Support was first found at about 20% - 25% of the base money supply in the early 1990's. This level was also support in the era prior to the beginning of the 1970's bull market. From the chart we see another down-leg that lasted until the turn of the century, and this took gold down to an even lower level relative to the base money supply, and about 90% down from the 1980 peak.

A similar observation can be made if we look at the value of the U.S. gold reserves in terms of the M3 money supply. This measure is officially called the Fear Index among those in the gold (bug) community.

In order to measure gold's valuation and to determine if gold offers good value or not James Turk came up with the Fear Index, which is calculated by multiplying the gold price by U.S. gold reserves and dividing it by the M3 money supply.

The Fear Index reached a 1980 peak of roughly 9.5% and at its bear market trough it sank as low as about 1%, which is nearly a 90% decline.

(click to enlarge)

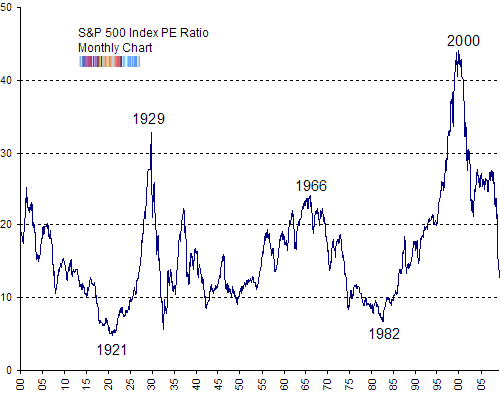

These two measures of gold suggest that the yellow metal was overvalued in 1980. But there were other factors that indicated in 1980 that gold did not offer good value. Dollars and dollar denominated assets were far more attractive than they were earlier in the decade because out-sized yields were prevalent. Stocks were extremely attractive on an earnings yield (aka p/e) basis, having reached what has historically been a very attractive long-term entry point of >10% (<10-times earnings).

(click to enlarge)

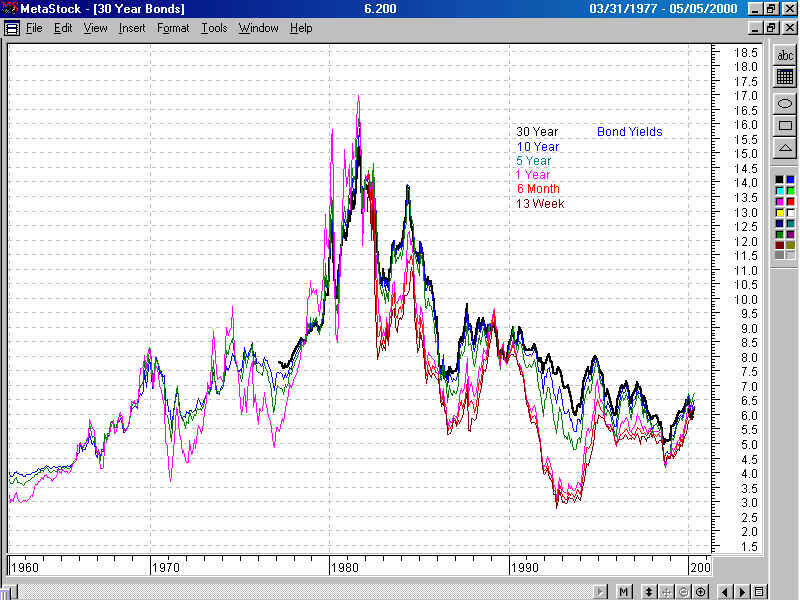

The same can be said about U.S. Treasuries, which offered very attractive yields (again >10%) throughout the curve.

(click to enlarge)

With yields on financial assets being so high and inflation fears peaking, gold was decidedly unattractive, and while in all likelihood monetary authorities and politicians wanted the gold price to fall (based on what we have seen in the two previous articles, especially part two) they did not have to intervene to make it happen.

Was There Intervention During the Early Bear-Market Stages?

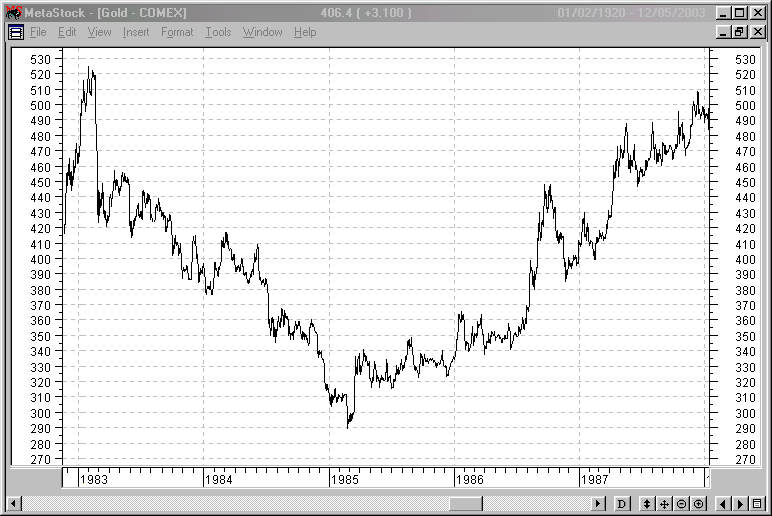

That doesn't mean that there was no intervention in the gold market during the 1980's. While there is no way to prove it, there is some suspicious price action that might raise some red flags. For example on April 27, 1987 the gold price fell by $20/ounce in just 4 minutes. $20/ounce was a lot, as the London fix on the 27th was $474.75 (the drop is more or less equivalent to a $50-$60/ounce move lower in 4 minutes in today's market). But in the context of the mini bull market in gold in 1987 (illustrated below) one could easily argue that there was simply a large seller unloading a position in an uptrend in a larger bear market.

(click to enlarge)

I should also mention that gold leasing begins in the 1980's, albeit on a small scale. There probably wasn't enough gold leasing in the 1980's (<1,000 tons had been leased out by 1990) to link it to a concerted effort to suppress the price, although the fact that gold leasing is thought to be a primary means of gold price suppression from the 1990's to the modern day breeds suspicion.

But ultimately it is hardly worth nit-picking to determine whether such meager evidence points to a concerted effort to suppress the gold price when there is no strong evidence, and when a bear market in gold was justified.

Gold Price Suppression: The Modern Regime (From the Early 1990's to Brown's Bottom)

1: Introductory Remarks

An all-too familiar story once again began to play out in the 1990's: the money supply of the United States had been rising along with bonds and stocks, making the yields on these assets far less appealing than they were in 1980. As a result, upward pressure was once again coming into the gold market. While there are no "incriminating" statements such as those found in the aforementioned Coombs' article, we once again see, as we did in the 1970's, concerned central bankers and monetary authorities opening up the possibility that interventions in the gold market can/should be made in order to keep the price from rising, or to force it lower.

We also see suspicious price action that defies probability: there are strong downward price spikes on a regular basis just before the London PM Fix (10:00 am Eastern Time).

Finally we begin to see a surge in gold leasing, a process whereby central banks would lease gold to commercial bullion banks for the purpose of running a gold carry trade. By borrowing gold at a low interest rate and buying higher yielding assets, bullion banks could make enormous profits, especially by leveraging this trade. Since gold prices were falling, this trade was especially appealing to bullion banks, and central banks benefited by earning a small amount of interest on what would otherwise have been a "non-performing asset." Gold leasing is accompanied by gold swaps, whereby an institution gives gold to another institution in exchange for currency. This differs from an outright sale of gold in that the transaction will be reversed at an agreed upon date at the same exchange rate. In leasing and swapping gold, central banks utilized unorthodox accounting practices by lumping gold reserves and gold receivables (i.e. claims on previously leased/swapped out gold) into one balance sheet item.

As a result gold was entering the market without a visible source, and this generated the appearance of a gold supply that was rising far more rapidly than it actually was. In effect gold derivatives were used in order to create a fractional reserve expansion of existing gold supplies.

2: The Modern Suppression Regime

A: What Changed In 1993?

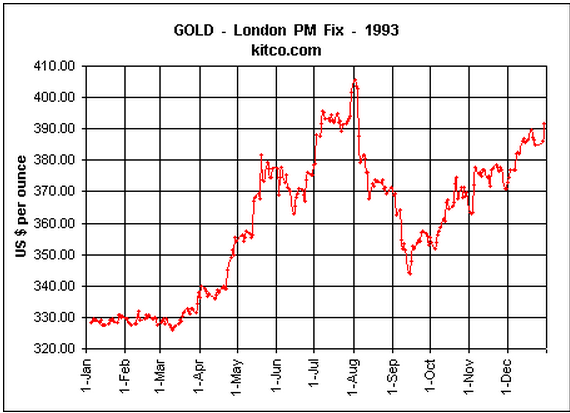

Proponents of the gold price suppression thesis argue that the modern effort to suppress the gold price (or to manage its ascent more recently) began back in 1993. Dimitri Speck, author of The Gold Cartel: Government Intervention on Gold, the Mega Bubble in Paper, and What This Means for Your Future pinpoints August 5th of that year as the beginning of the modern effort to suppress gold prices.

During the first half of 1993 the gold price began a meaningful ascension that threatened the bear market on a technical basis--as the following chart shows, had the price appreciation continued it would have begun a long-term pattern of higher lows and higher highs beginning in 1985.

(click to enlarge)

The price spike is more pronounced on a shorter term chart.

(click to enlarge)

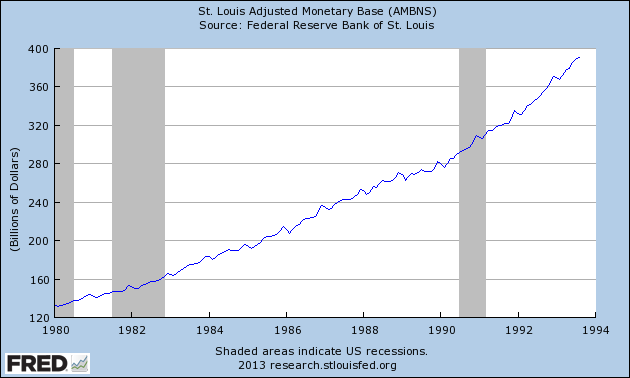

Not only was there strong price action that threatened to reverse the long-term bear trend, but by 1993 gold was once again becoming good value while at the same time stocks traded at nearly 20-times earnings, and bond yields were not much higher than the CPI's rate of increase. As we saw in the 1950's and 1960's the gold price was not rising, but the money supply certainly was. The following money supply charts illustrate this point. All charts look at data from 1980 through August, 1993.

M0

(click to enlarge)

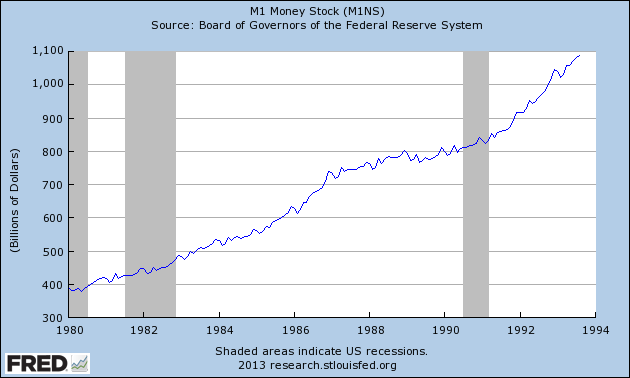

M1

(click to enlarge)

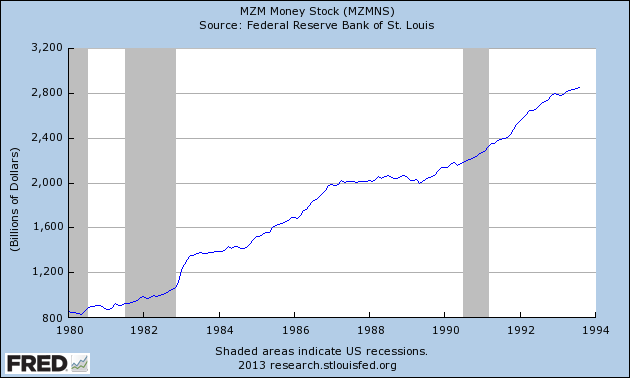

MZM

(click to enlarge)

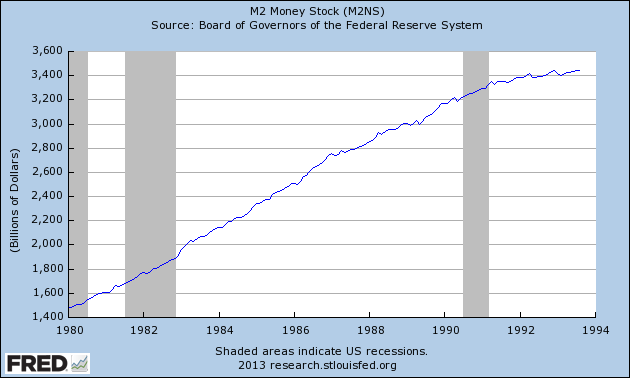

M2

(click to enlarge)

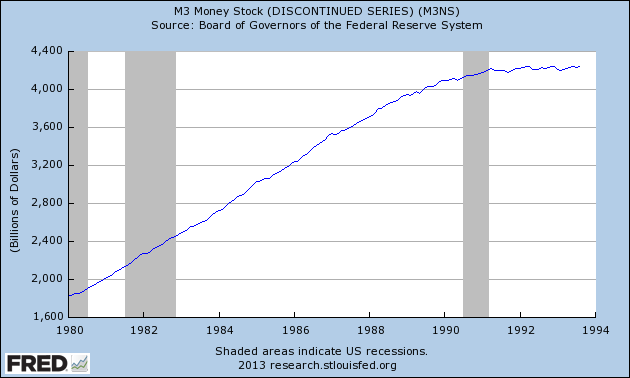

M3

(click to enlarge)

Thus depending upon your preferred method of measuring the money supply, throughout the bear market in gold from 1980 to 1993 there was an increase of roughly 2.5-3 times while the gold price lost more than half of its value. As a result gold once again offered good value relative to the money supply and there is a good possibility that the price increase in the first part of 1993 would have marked the beginning of a new bull market in gold if measures weren't taken to prevent this.

Central bankers, who had more or less ignored the topic of gold in their discussions throughout the 1980's, were once again faced with the threat it posed to U.S. Dollar hegemony. Fed Governor Wayne Angell addresses the (then) recent 20% rise in the price of gold in the first part of 1993 during the July 6-7 FOMC meeting. He suggests that Fed policy should be used to control the rising price of gold in order to reinstate confidence in the U.S. Dollar (p. 40-41).

What he suggests is not outright manipulation because he wants rather to hike the Fed Funds rate. Angell was alone on the issue of rates, but it appears that he had company on the issue of gold as a "thermometer" for the Dollar's value.

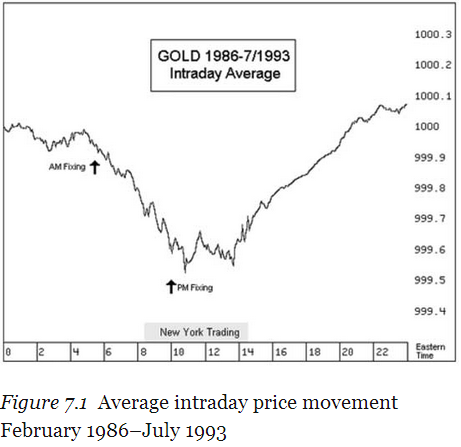

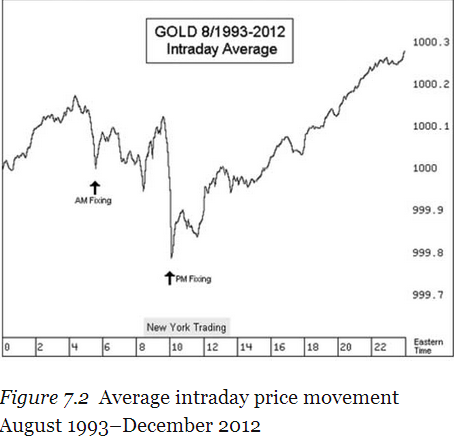

The rise in the price of gold reversed violently in August. However, Speck's "smoking gun" comes from an abrupt change to the intraday price patterns in the gold market. Speck looks at the average price action on any given day in the gold market prior to August 1993 and the same data for after 1993. A comparison of the two charts does reveal an abrupt change.

We see that throughout (from 1986 - 2012) there is general weakness in the morning (Eastern Time) and then strength going into the afternoon and evening trading sessions. However, even with thousands of trading days averaged together, there is still a sharp decline going into the London PM fix starting in August 1993.

This is a glaring red flag that prompts Speck to assert that this statistical aberration is "proof" of a concerted effort to suppress the gold price. This is "proof" in the same way that we would say that there is proof of foul play in a coin toss game that shows heads 60% of the time after a million tosses. It is so improbable that, at least in my mind, and in the mind of other rational individuals, that there is no doubt that there is unusual market activity--in this case a concerted effort to lower the London PM fix.

What is so unusual about this averaged price action is that it implies that there are commonly individual days on which there are sharp declines in the price of gold going into the London PM fix, and this reflects irrational trading behavior from the point of view of a trader who wants to maximize his or her profit by realizing the maximum price through gradual selling that doesn't overwhelm the market. The downward price spike reveals that large, sophisticated sellers are in the market on a regular basis for reasons other than maximizing profits from a trade--this fits my second condition for market manipulation.

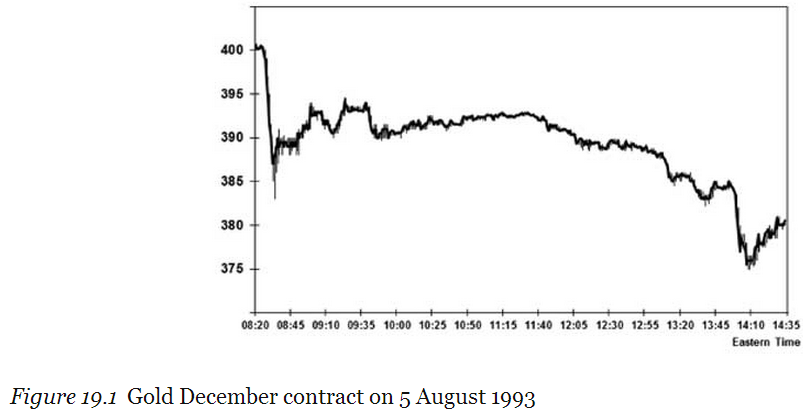

Speck picks August 5th, 1993 (he actually picks a moment in time--8:27 AM Eastern Time) because this is the first day on which we see one of the tremendous price declines that the statistical data hints at since the aforementioned July FOMC meeting.

(click to enlarge)

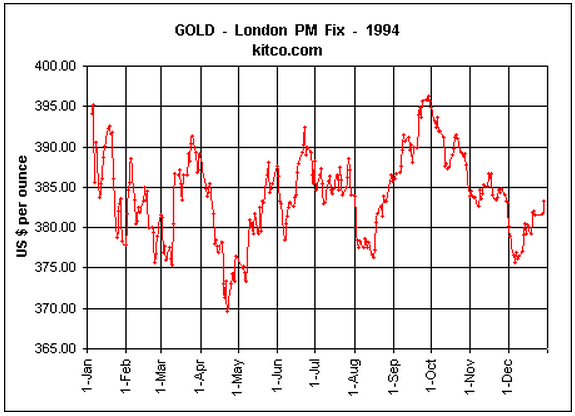

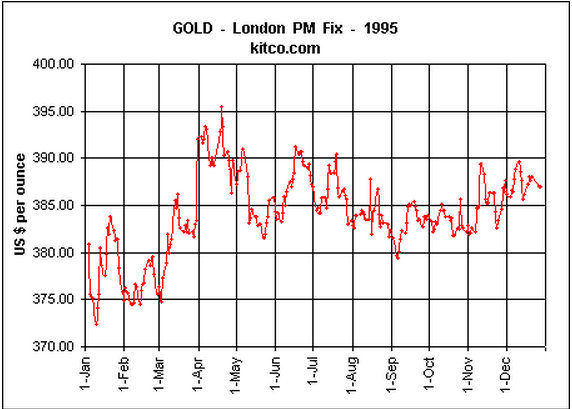

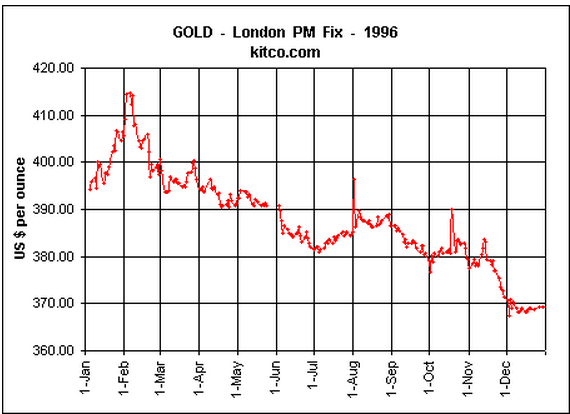

As the chart illustrates, the price falls over 4% in a matter of minutes. We also see that the price fell from the psychologically important number of $400/ounce. While the notion that round-number resistance levels are important in trading might seem puerile this is hardly the case, and charts from the mid 1990's show that this resistance level is approached regularly, only to be rebuffed, except for one breach for a few days in 1996.

(click to enlarge)

(click to enlarge)

(click to enlarge)

Speck's choice of the particular date--August 5th, 1993--is intriguing and convincing, but it is circumstantial. From my perspective, it is more important to demonstrate intent to manipulate and evidence that there is actually market activity. The statistical data provides this to a certain extent. However, an unusual and telling arrangement of seemingly random events makes far more sense in the context of a narrative, as we saw in the case of the LGP and in the 1970s political discourse that involved gold.

B: Gold Swaps and Gold Leasing

As I hinted at with the Angell comment, the mid 1990's mark a resurrection of gold-related discussions at the Fed and other powerful monetary institutions. We find nothing like the Coombs' article in which a step-by-step historical disclosure is provided of a manipulation scheme. However we do find some very telling statements--mentions of gold and related derivatives where introducing gold appears to be an unusual, or perhaps coincidental choice on behalf of the speaker. However mentions of gold appear to be strangely deliberate, and their significance is corroborated by market activity.

Let us look at a couple examples.

Virgil Mattingly and The ESF's Gold Swaps

In the January, 1995 FOMC minutes, Virgil Mattingly, the Fed's chief counsel, discusses the legality of some loans made by the Exchange Stabilization Fund.

MR. MATTINGLY: It's pretty clear that these ESF operations are authorized. I don't think there is a legal problem in terms of the authority. The statute is very broadly worded in terms of words like "credit"--it has covered things like the gold swaps--and it confers broad authority. Counsel at the White House called the Treasury's General Counsel today and asked "Are you sure?" And the Treasury's General Counsel said "I am sure." Everyone is satisfied that a legal issue is not involved, if that helps. (p. 69, my emphasis)

This is the one mention of "gold" in this lengthy 145 page document, and furthermore "gold swaps" are the only financial instrument mentioned here with any specificity. There is, of course, no implication here that gold swaps are being used by the ESF. Still, the possibility that Mattingly opens up is incredible.

Prima facie it says that the ESF can engage in gold swap transactions. The ESF is a reserve fund of the Treasury Department, which holds the U.S.'s gold. Since a gold swap is an agreement whereby gold is exchanged for cash (in whichever currency) this basically means that the U.S. government's gold can legally be sold into the market so long as it retains a piece of paper stipulating who owes it gold and when it is owed.

Of course these are just words, and we remember fondly how in 12 Angry Men Henry Fonda explains to his fellow jurors that uttering the phrase "I'm going to kill you." doesn't implicate the defendant of his father's murder. The smoking gun comes to light when we notice that the ESF showed losses in currency trading, which, according to Reginald Howe, were related to gold positions that lost value during time-periods in which the yellow metal's price appreciated.

They [ESF profits and losses] become even more suspicious when plotted against gold prices over the past two years, where on a quarterly basis and allowing for shorts lags in realizing profits or losses, firm or rising gold prices tend to correspond with ESF losses and falling prices with ESF profits. This relationship does not hold true for the last calendar quarter of 1997 (first quarter of fiscal 1998 for the ESF), but then declining gold prices reflected concern about lower demand and even dishoarding as a result of the Asian financial crisis, which may have impacted the ESF's results adversely as well. Thereafter, rising gold prices in the first four months of 1998 correspond with ESF losses in the second and third fiscal quarters, and falling gold prices to September with a small recovery that month with ESF profits. From October 1998 through the end of the year gold prices remained weak and in declining mode, and the ESF had one of its most profitable quarters.

The observation that the ESF was active in the gold market is corroborated by James Turk, who finds a "smoking gun" (the title of his article) in discrepancies between gold stocks listed by the Treasury and the Fed that could only be explained by ESF activity in the gold market.

If you have ever visited the Gold vault buried deep below the basement of the Federal Reserve Bank of New York, you will see countless cubbies where the Gold is stored. Each of those cubbies is identified with a unique number that corresponds with the owner of the Gold stored in it. One of those cubbies is owned by the ESF. Reg [Reginald Howe] suggested to me, and I agree with his thinking in this regard, that apparently low level Federal Reserve staff have been dutifully recording movements of Gold into and out of that ESF cubby, and recording them in the month-end reports of US Reserve Assets, probably unbeknownst to the Treasury officials who have been denying any involvement by the ESF in the Gold market.

Whether or not this activity is related to gold swaps entered into by the ESF is not something we can prove. But we do know that it is legal, and we do know that the ESF is profiting from the decline in the gold price. Finally we know that the ESF is intended to influence the value of the Dollar and that in the past we have seen the connection between the perceived value of the dollar and the price of gold. These observations make it very clear to anybody familiar with the history that I discuss in parts 1 and 2 that the ESF was involved in suppressing the gold price.

Alan Greenspan and Central Bank Gold Leasing

The infamous statement by Greenspan from a 1998 congressional hearing that "central banks stand ready to lease gold in increasing quantities should the price rise," is another instance of a mention of gold in what seems to be a strange context but which has broad implications with substantiating market evidence. Here is the paragraph from which the above words are taken:

The vast majority of privately negotiated OTC contracts are settled in cash rather than through delivery. Cash settlement typically is based on a rate or price in a highly liquid market with a very large or virtually unlimited deliverable supply, for example, LIBOR or the spot dollar-yen exchange rate. To be sure, there are a limited number of OTC derivative contracts that apply to nonfinancial underlying assets. There is a significant business in oil-based derivatives, for example. But unlike farm crops, especially near the end of a crop season, private counterparties in oil contracts have virtually no ability to restrict the worldwide supply of this commodity. (Even OPEC has been less than successful over the years.) Nor can private counterparties restrict supplies of gold, another commodity whose derivatives are often traded over-the-counter, where central banks stand ready to lease gold in increasing quantities should the price rise.

Again gold leasing is mentioned in passing as just one of the possible applications of OTC derivatives. However we get official confirmation that gold leasing had been soaring during the 1990's from the World Gold Council's study Gold Derivatives: The Market Impact by Anthony Neuberger, who claims that gold leasing went from just under 1,000 tons to over 4,000 tons during the 1990's. Other data points to this effect are more damning. Frank Veneroso argues that this figure is significantly underestimated by the WGC: he says that by 1995 the figure is 6,000 tons vs. a 2,200 ton estimate. And his calculated number is 10,000 tons, but this number is so high relative to the official estimates that he shaves off 4,000 tons so that his figure doesn't appear to be so outlandish. If we assume with Veneroso that the shortfall of gold supply that needed to be met by central bank leasing was 1,200 tons in 1995, increasing to 1,700 tons in 2000, the total amount of gold leased out by central banks in 2000 could easily be twice the conservative 6,000 ton figure he puts out there. If the 10,000 ton figure is accurate then the actual number could be as high as 18,000 tons, which constituted more than half of the 33,000 tons estimated to be held by central banks at the time.

Such disparities imply that data on central bank gold leasing doesn't come with precision. This is no accident. As I have already mentioned there is no differentiation between gold reserves and gold receivables on most government and central bank balance sheets, which means we don't know how much gold they have actually leased out. In fact, according to the IMF in 1999, this is a standard accounting procedure given the "sensitivity" of markets to the disclosure of such information. The entirety of paragraph 15 is worth reprinting here.

Central bank officials indicated that they considered information on gold loans and swaps to be highly market-sensitive, in view of the limited number of participants in such transactions. Thus, they considered that the SDDS reserves template should not require the separate disclosure of such information but should instead treat al1 monetary gold assets, including gold on loan or subject to swap agreements, as a single data item. They also confirmed a view, taken by a number of countries (both inside and outside the G-10) at the December Board meeting, that the disclosure of the composition of reserves by individual currencies would be market-sensitive but that they would have no objection to disclosure of such information by groups of currencies. (p. 6)

Essentially this amounts to: central banks cannot disclose the specifics of their gold holdings because of the anticipated market reaction. This is more dissemination than direct price suppression, but given the timing of this statement (just before the bottom in the gold market), and given the disparity between Veneroso's numbers and the WGC numbers (even if reality is closer to the WGC numbers) it stands to reason that there is a concern amongst top monetary officials that accurate accounting of central bank gold holdings would lead to a price spike.

C: Brown's Bottom

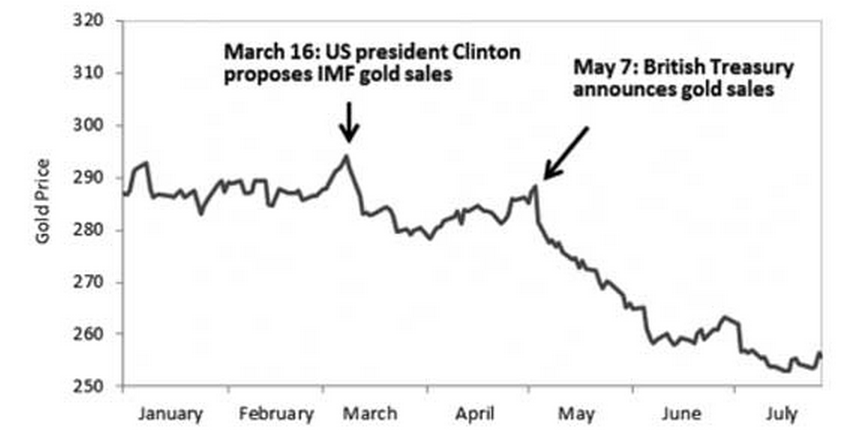

By 1999 the gold bear market was reaching 20 years in duration as well as an extreme in terms of price relative to the ever-increasing money supply. Furthermore financial assets such as stocks and bonds were reaching extreme valuations--especially stocks, which traded at more than 40-times earnings. Two events in 1999 appear to be hail Mary attempts to drive the gold price down in a fundamental environment that mandated the opposite: IMF gold sales proposed by president Clinton and BOE gold sales announced by Gordon Brown. What is suspicious about these events is not so much the sales but the announcements of the sales before-hand, which in both cases led the market to discount the gold price in anticipation of this oncoming supply.

(click to enlarge)

No rational trader would make such an announcement that reduced the price s/he received for the asset in question, and therefore these announced sales fit my manipulation condition that market activity takes place for some reason other than profiting directly from this activity. While it worked to some extent in the short term long term this marked the beginning of the end of the bear market that could have very easily ended 4-6 years earlier had we not seen an artificial surge in the supply of paper gold.

Conclusion

Ultimately what we see in the 1990's is a fairly obvious attempt to suppress the gold price in the face of improving fundamentals. While there was no one price targeted, and while there were no open announcements of a price suppression agenda, there is irrefutable evidence that there was a surge in gold-related derivatives that lead to a large increase in the perceived amount of gold available in the market. Gold derivatives created a de facto fractional reserve market in which claims on gold were not differentiated from physical gold, and the additional "supply," coming from western central banks, suppressed the price.

Furthermore, there is evidence that steps were taken to mask the exact amount of "fractional-reserve gold" that was created through gold leasing and gold swaps. Central banks didn't differentiate between gold reserves and gold receivables, and we saw that they did this in order to shield the market from the true extent to which gold receivables had replaced physical reserves.

Finally, while there are rationalizations for engaging derivatives trading that do not relate to price suppression (i.e. earning interest on a non-performing asset), there is little doubt that the explosion in the derivatives market in gold indicates that leasing and swaps were utilized in order to suppress the gold price. This becomes especially apparent when viewed in the context of the openly stated concerns from the likes of Angell and Greenspan that the gold price might rise and signal inflation or weakness in the Dollar or the U.S. economy.

When we consider the statements from monetary authorities that the gold market can and should be suppressed alongside the radical changes in the gold market as a result of derivative trading we can see clearly that there was manipulation in the 1990's. This should surprise no one who is familiar with the details pertaining to the gold market after the Bretton Woods Agreement.

If we then bring into consideration the statistical anomalies in intraday trading and the appearance of a "hidden force" selling gold into the market just before the London PM fix our suspicions become revelations, and our suppositions realities--the Federal Reserve and the Treasury Department through the Exchange Stabilization Fund (along with the Bank of England, the IMF, and possibly others) were actively engaged in the gold market in a concerted effort to cap or suppress its price.

0 comments:

Publicar un comentario