Buttonwood

Here we go again

Governments don’t like strong currencies

Nov 16th 2013

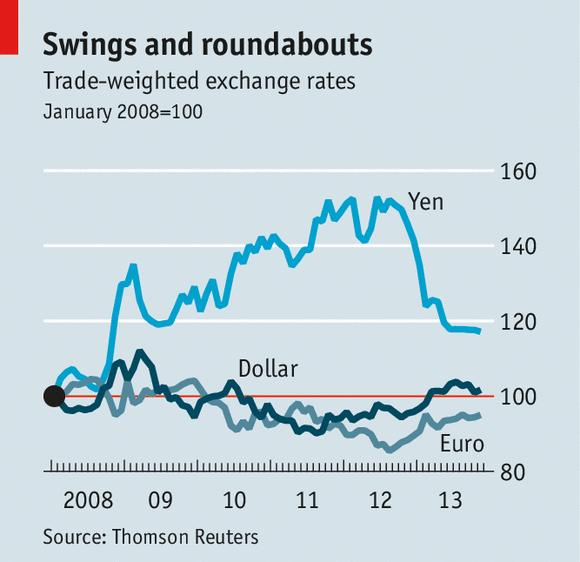

THE game of “pass the parcel” is enjoying another round. The yen has fallen by nearly 17% against the dollar since Shinzo Abe became prime minister of Japan at the end of December last year. That may be a boost to the competitiveness of Japanese exports but foreign-exchange markets are a zero-sum game: if one currency weakens, another must strengthen.

America, with its relatively robust economy, can probably cope the best with a stronger currency. But the euro zone is barely emerging from recession, and its currency has risen even more against the yen than the dollar has over the past year. Worse still, the debate at the Federal Reserve during the summer about reducing monetary stimulus caused many emerging-market currencies to decline as capital started to flow back to the developed world in anticipation of higher yields and in response to slower growth in emerging markets. All this has pushed up the trade-weighted value of the euro by almost 9% since last November.

.

Some might have little sympathy for the euro zone. In aggregate it has a current-account surplus and its currency has been the weakest of the big three since the financial crisis (see chart). At a time when trade growth has slowed significantly—the World Trade Organisation forecasts a rise of just 2.5% this year—no country wants its exporters to lose market share. It would be tricky for any of the big economies to adopt an open policy of competitive devaluation; its trading partners would complain.

According to Mario Draghi, the president of the European Central Bank (ECB), the euro’s strength was not even discussed at the meeting on November 7th when it cut rates by a quarter of a point. If so, the irony was that the euro dropped fairly sharply on the news, while most economists thought the rate reduction would otherwise have little economic impact. Some analysts think the euro could keep falling if the ECB and the Fed head in opposite directions, with the Fed starting to “taper” its expansive policies next year.

Openly calling for a decline is one thing. But currency weakness as the side-effect of a different policy—quantitative easing, for example—is another matter. The Bank of England did nothing to stem sterling’s slide in 2008 and 2009, and did not face any international complaints.

Smaller economies have the latitude to indulge in open currency manipulation. The Swiss franc has long been the favoured currency of nervous investors at times of crisis, and the Swiss National Bank intervened to cap the currency’s rise in 2011. The Czech National Bank has just followed the Swiss example, declaring it will attempt to cap the koruna at a rate of 27 to the euro. It cannot lower interest rates: they are already at zero.

From a central bank’s point of view, intervention to drive a currency down is a lot easier than propping it up. Supporting a currency involves selling foreign-currency reserves and buying domestic assets; in the face of determined speculation, the reserves usually run out. The central bank can increase interest rates to support the currency, but this usually inflicts collateral damage on the domestic economy, as Britain discovered during its ill-fated membership of Europe’s Exchange-Rate Mechanism in the early 1990s.

Weakening a currency involves the creation of domestic money to buy foreign assets, giving the central bank virtually unlimited scope to pursue the policy. Over the long run, of course, such an approach might lead to high inflation. But since both the Swiss and the Czechs have been facing deflationary pressures, that is not a problem at the moment. Indeed, to the extent that a weaker currency means higher import prices, this may prevent deflation from becoming entrenched.

It is worth remembering that a devaluation is a reduction in a nation’s standard of living: it costs more for domestic consumers to buy foreign goods. That is why governments tended to resist them. By the same token, however, a devaluation is akin to a wage cut, a way of making a nation’s goods more competitive in global markets. And it is a lot easier than asking workers to accept actual cuts in wages.

What does it all mean at the aggregate level? To the extent that surreptitious attempts at devaluation lead to easier monetary policies across the developed world, this may be supportive for the global economy.

The danger lies in the longer run. If countries believe their competitors are stealing a march via their weaker currencies, they may resort to more protectionist measures, especially at a time when voters are dissatisfied and angry.

0 comments:

Publicar un comentario