Central Bank Gold Demand Is Not What It Seems

Nov 12 2013, 17:24

In September 2011, the Turkish central bank introduced a new monetary tool called the 'Reserve Option Mechanism'. This mechanism gave commercial banks the option to use gold they were holding in unallocated customer accounts to meet a portion of their Turkish lira reserve requirements.

The central bank has been accounting for these gold transfers on its balance sheet as monetary reserves since then, given the impression to those who did not understand the program that the Turkish central bank was buying or otherwise increasing its actual gold reserves. This policy was part of a broader effort to boost liquidity at lower costs within the Turkish banking system, to free lira in the banking system for lending at a time of severe economic stress in neighboring Greece and the rest of Europe, and to reduce volatility caused by capital flows in and out of the country.

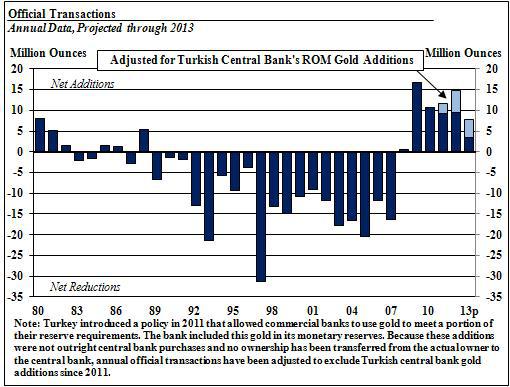

Turkey had not adjusted its actual central bank gold reserves since 1995. Turkey's central bank added 2.5 million ounces of gold to its reported reserves in 2011, 5.3 million ounces in 2012, and 4.1 million ounces during the first eight months of 2013. These recent additions to Turkey's official reserves were the result of this new monetary tool, introduced in September 2011 and should not be included in central bank purchases.

Although these additions have been raising the central bank's officially reported gold reserves, they should not necessarily be considered central bank reserves and they do not represent central bank purchases. This is gold ultimately owned by investors. Some of it may have been purchased recently, but much of it may have been in these investors' holdings for years. To count this investor gold, now being used as reserves, as central bank gold acquisitions would be to double-count this metal and would give a false impression of the pace of central bank gold acquisitions. This gold could disappear from the central bank's reported monetary reserves should the original individual owners withdraw their metal from the commercial bank unallocated deposits, or merely shift the metal to allocated accounts.

(click to enlarge)

Since the launch of the reserve option mechanism as it relates to gold, the portion of Turkish lira reserve requirements allowed to be denominated in gold increased from 10% to 30%. Gold holdings for the purpose of meeting reserve requirements have risen from 1.6 million ounces to 8.4 million ounces between March 2012 and March 2013.

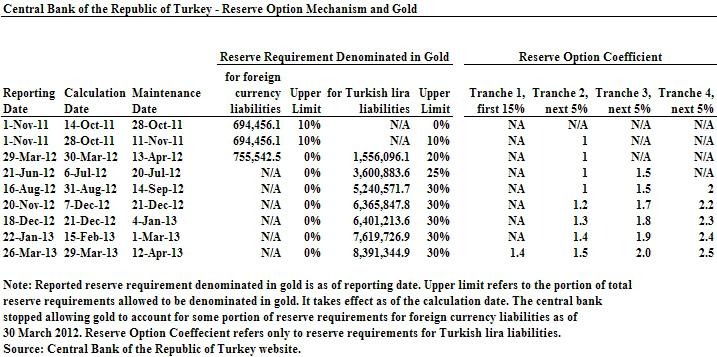

In addition to raising the upper limit for gold's optional share of Turkish lira reserve requirements, the central bank employed a 'Reserve Option Coefficient' tool, which is a multiplier used to determine the amount of gold to be held per unit of Turkish lira reserve requirements. The larger the coefficient, the more gold that is required to meet the equivalence of one Turkish lira reserve requirement. It essentially is a discount applied to the value of gold off of the market value. Such discounts are common in gold financial transactions. This tool provides even greater monetary policy flexibility.

The table below shows the evolution of these tools as they pertain to the increase in the Turkish central bank's reported gold holdings. The gold used as reserves against the central bank's reserve requirements remains in the commercial bank vaults and are not physically transferred to the custody of the central bank.

(click to enlarge)

Another factor that has been inflating the reported level of central bank demand is related to the mis-labeling of gold purchased by sovereign wealth funds (SWFs) as being central bank additions to monetary reserves. SWFs are investment entities, with radically different rationales for buying and holding gold. They have investment holding horizons of three to five years, as opposed to the longer term, open-ended programs of central banks buying gold as monetary reserves.

In conclusion it can be said that net purchases by central banks is a positive development for the gold market and would continue to provide support to the price of gold. Investors should however have a realistic understanding of how large reported central bank gold purchases are before investing in the metal.

0 comments:

Publicar un comentario