Golden Autumn For Gold Mining Stocks

May 27 2013, 13:35

By: Daniel Gschwend

.

Calling the gold bull market over seems to be premature. Aren't the same fundamental drivers in place as some months ago?

- Massive QE programs

- Negative real interest rates (but admittedly at least officially less negative)

- Debt overhang and deflationary forces

The only thing different is the belief central banks have everything under control and a desperate move into risky assets, predominantly stocks. What makes me think that gold mining stocks have now fallen far too much? For the first time ever, and I've tracked this sector since 2004, I see management changes taking place and statements such as focus on earnings and payouts for shareholders! Nice, well at least they came to the same conclusion as most managers decades ago…..(sorry about being sarcastic). To keep the story short, I think gold mining stocks have fallen too far and are now extremely cheap. Additionally, market allocators are either completely out of this sector or massively underweighted.

These are structural situations from a contrarian point of view that have the potential to trigger a bounce in the magnitude of 20% to 30%. I find it hard to believe that the S&P 500 will surge another 30% from here until year end, but can easily imagine that bombed out gold mining stocks could recover by 30%. That makes the sector relatively attractive and for the first time in many years, I'm optimistic about gold mining stocks because real changes at the top management levels are taking place.

I expect that gold mining stocks will bottom out in the next couple of months - I also expect the next substantial rally will start between summer and autumn 2013. I expect gold will fluctuate between $1,300 and $1,500 before the next move up starts. Gold topping $2,000 within the next two years is not if, it's when.

Fundamentally, nothing has changed for gold: central banks are printing money (watch out when the money multiplier starts to work!), real interest rates are negative and will remain negative for many years (if nominal yields would start to rise the recovery would be killed instantly), besides, official inflation numbers are (let's say it this way) imperfectly measured - real inflation for the man on the street is much higher than official numbers. Currency war is a reality and will intensify. I think that after the German election this fall, Germany will have a "Grosse Koalition", which means the parties from the left (SPD) and from the center-right (CDU/CSU) will form a combined government. The left-wing party (SPD) is much more EU friendly and will greet more aggressive actions from the ECB to support the European recovery. This means: massive QE in Europe; please remember, so far the ECB has not done any comparable QE. Europe needs a weaker Euro to boost exports. That will start towards the end of this year or early 2014.

Should the USD appreciate against the EUR (because of this QE program), the USA will also start to weaken the USD. So far the US QE has been mostly currency neutral: the USA did not buy foreign currencies to weaken the USD, it funded its fiscal deficit.

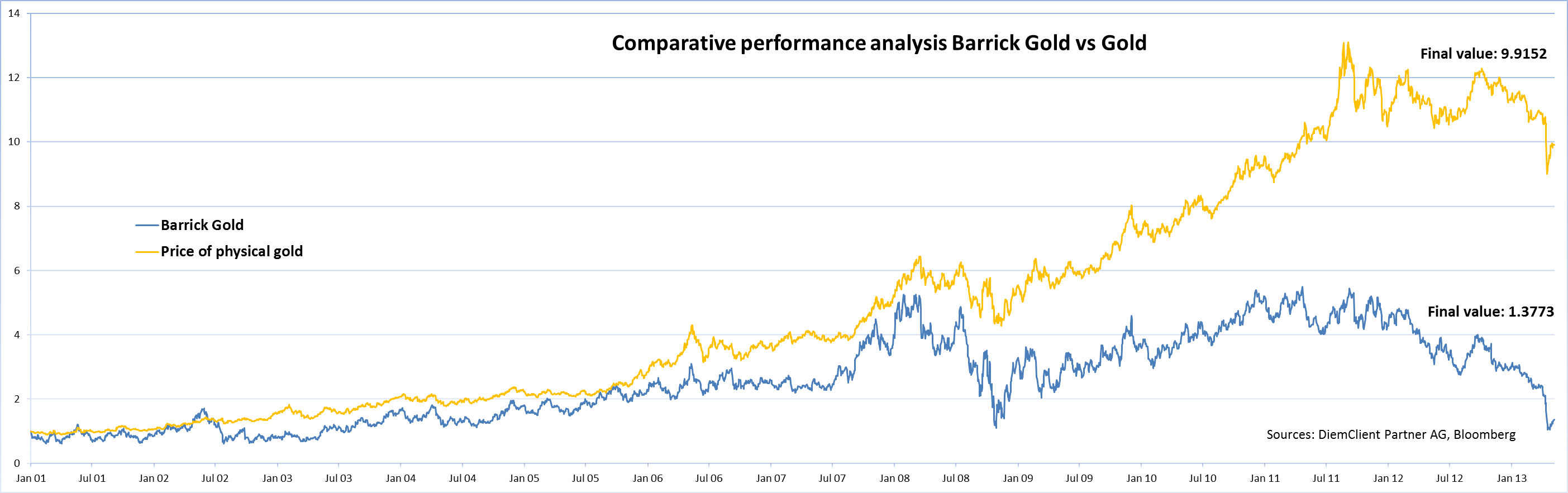

Gold will start to massively outperform once the USA enters the real phase of currency wars: selling (printing) USD and buying foreign currencies to weaken the USD. This is a storybook and happened before, why should it be any different this time? If I had to pick some names, I like New Gold (NGD), Yamana Gold (AUY) and Barrick Gold (ABX) (because the stock has fallen now far too much, here we have the situation of not buying good things but buying things well…).

Sell-Off in gold (4/12/2013):

The sell-off in gold didn't happen initially by gold ETF or investors getting rid of physical gold. The avalanche was triggered in the paper gold market (futures). Huge volume hit gold as you can see in the chart:

(click to enlarge)

.

Allegedly, the equivalent of 200 tons of gold were sold within minutes (as comparison Cyprus has 14 tons of gold….) and over 2,000 tons within two days. That's pretty much, considering a yearly production of approx. 2'700 tons of gold. In the aftermath, lots of buyers took the opportunity to buy physical gold even though gold ETF and future positions were further reduced. Commercials are covering their shorts while speculators have massively reduced their net long positions. Historically, commercials had a good record in catching bottoms and speculators were a good contrarian indicator (low levels such as now are indicating a short term bottom).

Investors are tired of earning misses. Therefore valuation multiples have collapsed and the entire sector is punished. I guess many companies will now put all the bad news into the next few quarterly reports. Just to give you an idea:

EPS GAAP Quarterly Numbers

- Goldcorp (GG): Missed 6 of 8

- Barrick Gold: Missed 5 of 8

- Newmont Mining (NEM): Missed 5 of 8

- Kinross Gold (KGC): Missed 5 of 8

Reality is, that most gold mining companies miss constantly earnings estimates. If you compare the same numbers, Microsoft (MSFT) beat 7 of 8, GE (GE) beat 4 of 8, Pepsi (PEP) beat 4 of 8, Cisco (CSCO) beat 6 of 8.

Investors have every right to be disappointed. Taking equity risk has not been rewarded:

(click to enlarge)

.

But finally, something is changing in the industry:

2) Management changes: In 2013 Newmont replaced its CEO, Barrick Gold did the same in 2012 as did Kinross Gold. I still miss to see some mining outsider to become CEO or Chairman. I also wonder why private equity companies are not taking over some of the big names or activist investors such as Carl Icahn, etc. There is huge value to unlock if executed properly.

Concluding, smart money has gone back into gold mining stocks: Soros Fund Management, SAC Capital Partners LP and Paulson & Co. bought over $183 million in new call options on gold mining equities. I'd recommend accumulating gold mining stocks into weakness for a substantial rebound into autumn.

0 comments:

Publicar un comentario