Albert Edwards' Bleak Crystal Ball Reveals Gold Above $10,000; S&P At 450 ; And Sub-1% Bond Yield

Thu, 04/25/2013 - 07:55 EDT - Zero Hedge

Just because some of the C-grade financial "pundits" out there may have been confused that Albert Edwards was turning bullish in recent months, this should help clear all confusion. We still forecast 450 S&P, sub-1% US 10y yields, and gold above $10,000. My working experience of the last 30 years has convinced me that policymakers’ efforts to manage the economic cycle have actually made things far more volatile.

Their repeated interventions have, much to their surprise, blown up in their faces a few years later. The current round of QE will be no different. We have written previously, quoting Marc Faber, that “The Fed Will Destroy the World” through their money printing. Rapid inflation surely beckons. But that will not occur without firstly a Japanese-style loss of confidence in policymakers as we dive back into recession and produce dislocative market moves.

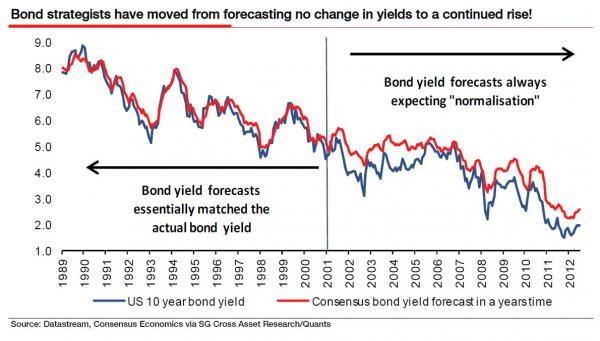

Andrew Lapthorne passed me a great chart the other day of bond strategists´ forecasts. It reminded me of similar charts for analysts earnings forecasts from my former colleague, James Montier. There are some ever-present truths in this business. Economists usually forecast a return to trend growth and will never forecast a recession.

Equity strategists tend to forecast the market will rise 10% each year and will never forecast bear markets. And since the equity bubble burst in 2000, bond strategists, in a discernible break in behaviour, now only ever forecast that bond yields will rise (see chart below). I agree that bond yields will indeed be heading higher in the next 3-5 years, much, much higher.

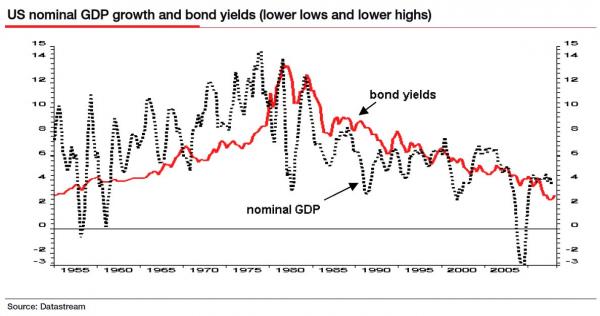

But the consensus has still not accepted that we remain locked in an Ice Age environment that will see US (and UK and German) yields converge to Japanese sub-1%. The late Margaret Thatcher had a strong view about consensus. She called it: “The process of abandoning all beliefs, principles, values, and policies in search of something in which no one believes, but to which no one objects.” The same applies to most market forecasts. With some rare exceptions (like our commodity analysts? recent prescient call for a slump in the gold price), analysts don´t like to stand out from the crowd. It is dangerous and career-challenging. In that vein, we repeat our key forecasts of the S&P Composite to bottom around 450, accompanied by sub-1% US 10y yields and gold above $10,000.

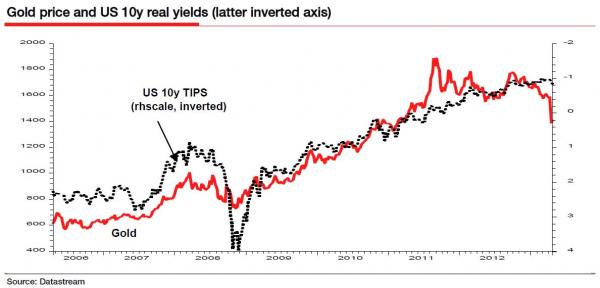

Some other thoughts from Albert on 10 Year bonds: US 10y nominal yields have been edging down recently to 1.70% and the gap with real yields has closed ever so slightly, but the gap itself (implied inflation expectations) remains high.

There is much more, but the most amusing is where SocGen (Edwards) disagrees with SocGen (Legland) on gold: We have been asked extensively about the slump in the gold price, especially in the context of our commodity strategist´s prescient report calling for just such a decline link. My own view is that the reasons for owning gold have not changed. I expect imminent recession to be more likely than imminent takeoff and hence the real yield (a key gold driver) should remain low.

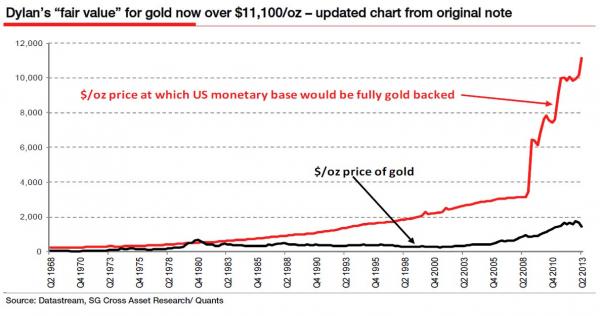

Gold corrected 47% from 1974-1976 before rising more than 8x to US$887/oz in 1980. A steep correction is normal before the parabolic move. As Dylan said in his note of Sept.

2011, The market for honesty: is $10,000 gold fair value?, holding gold is a bet against central banks competency and given their track record that´s certainly a bet I´d be happy to still take.

Their repeated interventions have, much to their surprise, blown up in their faces a few years later. The current round of QE will be no different. We have written previously, quoting Marc Faber, that “The Fed Will Destroy the World” through their money printing. Rapid inflation surely beckons. But that will not occur without firstly a Japanese-style loss of confidence in policymakers as we dive back into recession and produce dislocative market moves.

Andrew Lapthorne passed me a great chart the other day of bond strategists´ forecasts. It reminded me of similar charts for analysts earnings forecasts from my former colleague, James Montier. There are some ever-present truths in this business. Economists usually forecast a return to trend growth and will never forecast a recession.

Equity strategists tend to forecast the market will rise 10% each year and will never forecast bear markets. And since the equity bubble burst in 2000, bond strategists, in a discernible break in behaviour, now only ever forecast that bond yields will rise (see chart below). I agree that bond yields will indeed be heading higher in the next 3-5 years, much, much higher.

But the consensus has still not accepted that we remain locked in an Ice Age environment that will see US (and UK and German) yields converge to Japanese sub-1%. The late Margaret Thatcher had a strong view about consensus. She called it: “The process of abandoning all beliefs, principles, values, and policies in search of something in which no one believes, but to which no one objects.” The same applies to most market forecasts. With some rare exceptions (like our commodity analysts? recent prescient call for a slump in the gold price), analysts don´t like to stand out from the crowd. It is dangerous and career-challenging. In that vein, we repeat our key forecasts of the S&P Composite to bottom around 450, accompanied by sub-1% US 10y yields and gold above $10,000.

Some other thoughts from Albert on 10 Year bonds: US 10y nominal yields have been edging down recently to 1.70% and the gap with real yields has closed ever so slightly, but the gap itself (implied inflation expectations) remains high.

There is much more, but the most amusing is where SocGen (Edwards) disagrees with SocGen (Legland) on gold: We have been asked extensively about the slump in the gold price, especially in the context of our commodity strategist´s prescient report calling for just such a decline link. My own view is that the reasons for owning gold have not changed. I expect imminent recession to be more likely than imminent takeoff and hence the real yield (a key gold driver) should remain low.

Gold corrected 47% from 1974-1976 before rising more than 8x to US$887/oz in 1980. A steep correction is normal before the parabolic move. As Dylan said in his note of Sept.

2011, The market for honesty: is $10,000 gold fair value?, holding gold is a bet against central banks competency and given their track record that´s certainly a bet I´d be happy to still take.

0 comments:

Publicar un comentario