November 14, 2012

by: Eric Parnell

.

.

(click images to enlarge).

.

.

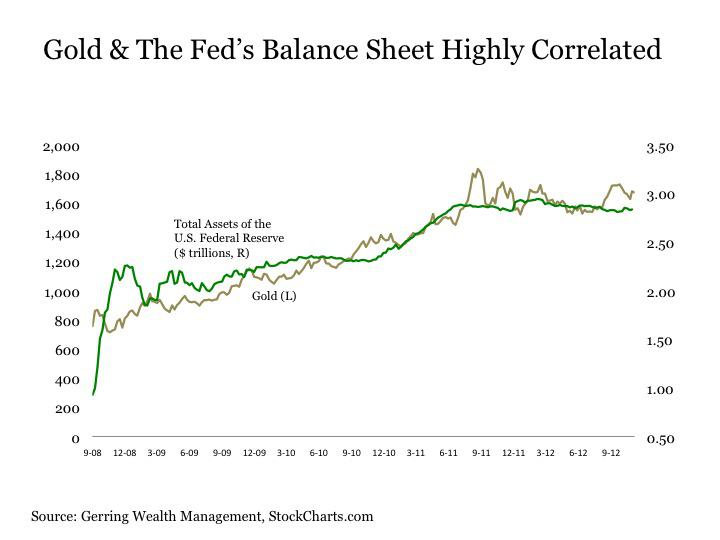

Balance sheet expanding monetary stimulus programs like QE3 are particularly supportive of gold. This is due to the fact that such programs result in the Fed printing money, which serves to devalue the U.S. dollar and induces investors to seek a store of value in hard assets such as gold (GLD). And gold has performed exceptionally well in recent years when the Fed is actively engaged in QE. In short, when the Fed is expanding its balance sheet during QE, gold rises along with it. And when the Fed steps away from a QE program, the increase in gold ebbs unless concerns over a potential crisis take over.

.

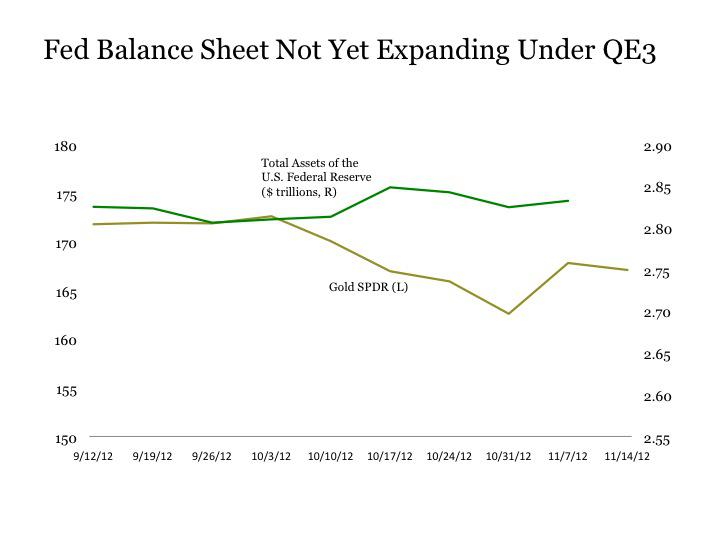

So why has gold not responded thus far under the latest QE3 program launched in September? This is because the Fed's balance sheet has yet to start expanding under the current stimulus program.

.

.

Unlike past QE programs that included the purchase of U.S. Treasuries, the Fed is focused only on purchasing Mortgage Backed Securities (MBS). Although the Fed is pledging to purchase $40 billion in MBS each month, the final settlement for these Fed purchases is not immediate.

Instead, it can take up to 180 days for the Fed to complete the transaction on these purchases. As a result, the initial phases of the current QE program have been marked by a slow and uneven expansion of the Fed's balance sheet that has also been offset by accelerated prepayment of existing MBS in the Fed's portfolio. Over time as this program builds momentum, the Fed's balance sheet is likely to smooth into a more consistent expansion. A recent article in The Wall Street Journal provides more details on this point.

Looking ahead, if the Fed seeks to expand its current QE program by opting to buy U.S. Treasuries outright once its current Operation Twist program concludes at the end of the year, the expansion of the Fed's balance sheet could pick up pace in an even more meaningful way.

All of this bodes well for gold in the months ahead. As the expansion of the Fed's balance sheet picks up pace, the tailwind behind gold should increase accordingly.

Moreover, gold has the potential to receive additional upside support if the European Central Bank and/or the People's Bank of China end up resuming balance sheet expanding monetary stimulus programs of their own in the coming months. Lastly, the financial risks and potential crisis points facing the global economy remain as pronounced as ever, which would also support the appeal for gold as a hard asset safe haven investment.

In maintaining exposures to gold, the Central GoldTrust (GTU) provides an ideal choice. And for those seeking exposure to both gold and silver (SLV), which offers a higher-octane exposure to these same themes, the Central Fund of Canada (CEF) is also a suitable alternative.

0 comments:

Publicar un comentario