Silver: The King Of Monetary Stimulus

August 18, 2012

by: Eric Parnell

.

The stock market is boldly signaling that a new round of balance sheet expanding monetary stimulus may soon be on its way. Having advanced virtually uninterrupted since the day after the latest ECB meeting in early August, stocks as measured by the S&P 500 Index (SPY) are already demonstrating that daily melt up pattern that we have come to know all too well from past rounds of stimulus.

Whether this next round of stimulus actually arrives is still subject to extensive debate, as many other key asset classes such as gold (GLD) are not yet confirming this outcome in any meaningful way. But given that the stock market has already begun aggressively pricing in more stimulus, this implies that better opportunities to capitalize likely reside elsewhere if this potential outcome were to come to pass. And nowhere is the possible upside more attractive than in silver, the undisputed king of balance sheet expanding monetary stimulus.

For the purposes of this analysis, I will focus on the iShares Silver Trust (SLV). However, the same price principles apply to the ETFS Physical Silver Shares (SIVR), the PowerShares DB Silver ETF (DBS), the UBS E-TRACS CMCI Silver Total Return (USV) and the Sprott Physical Silver Trust (PSLV).

Silver represents an attractive investment opportunity in the current environment for several key fundamental reasons. First, it provides hard asset protection against aggressive monetary stimulus, competitive currency devaluations, asset inflation and crisis. Also, if the global economy actually resumes a sustained growth phase at some point in the future, it also offers appeal for its industrial uses. Thus, the fundamental case for owning silver remains attractive despite the fact that the price has languished over much of the past year.

Silver has enjoyed its best performance since the outbreak of the financial crisis during periods when major central banks have been engaged in balance sheet expanding monetary stimulus. A look back over past stimulus programs highlights how dramatic this positive performance has been.

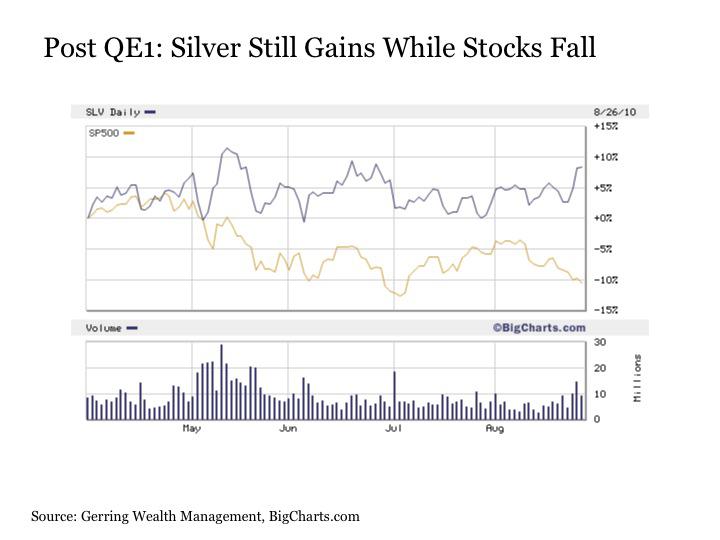

During QE1 in the aftermath of the financial crisis through the end of this program on March 31, 2010, silver posted returns that doubled the performance of the stock market.

Click to enlarge

.

The performance of silver was even more impressive during QE2. From the moment that the program was effectively announced at Jackson Hole on August 26, 2010, silver exploded into a speculative bubble with gains in excess of +150% through the end of April 2011. Even after the silver bubble burst, it still posted gains that were quadruple those of stocks by the end of QE2 on June 30, 2011.

.

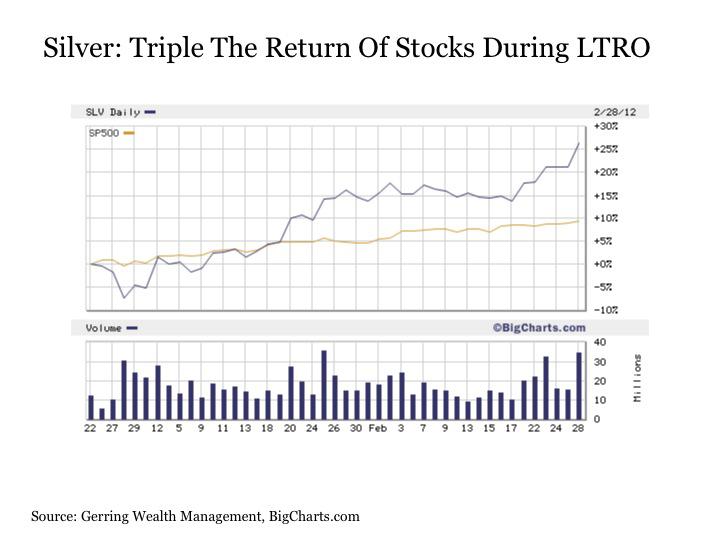

And the major stimulus program from the ECB had similar effects. During the ECB's LTRO program, silver posted returns that were triple those of stocks.

.

.

Thus, silver offers the potential for explosive returns during periods of balance sheet expanding monetary stimulus.

But what are the risks associated with silver going forward if the Fed and the ECB both opt to withhold further stimulus? The good news is that the performance has also traditionally been much better than stocks. Following the end of QE1, silver continued to post solid gains at a time when stocks began plunging lower.

.

.

And following the end of QE2, silver continued to post double-digit gains for the first several months. It was only after the Fed's announcement of balance sheet neutral Operation Twist in late September that Silver gave up its gains. But even with this pullback, it still managed to perform on par with stocks through most of the remainder of this post QE2 period.

.

.

Only over the last few months since the end of the ECB's LTRO program in February 2012 has silver posted poor results that have vastly underperformed stocks.

.

Silver represents a particularly attractive investment opportunity at present in light of recent developments. The white metal has a demonstrated track record of outperforming stocks by multiples during periods of balance sheet expanding monetary stimulus. As a result, if policy makers deliver on their seemingly endless promises that such an outcome is soon to arrive, silver is likely to once again explode to the upside. And the potential upside may prove particularly pronounced this time around, given silver's recently stark underperformance relative to stocks. Conversely, with the exception of the last few months, silver has also demonstrated itself to be a solid performer without the support of monetary stimulus. So given the fact that silver has trailed stocks by such a significant margin recently implies even greater downside protection if it turns out that the Fed and the ECB disappoint markets with no further stimulus in the months ahead.

With all of these positives for silver in mind, it is important to emphasize a final key point. Investing in silver is not for the faint of heart. The price movement of the metal is highly volatile, with the average daily price movement of 1.8% in either direction on any given day over the last five years.

Moreover, it has moved as much as +14% to the upside and -18% to the downside on single trading days during this time period. For these reasons, the allocation to silver as a percentage of an overall portfolio should be considered carefully and managed with care.

I recently added to overall allocations to silver, given the opportunities in the current environment. Given that I am also long gold, the allocation to silver is captured through holdings in the Central Fund of Canada (CEF), which contains both gold and silver. Incorporating this investment in complement with the Central Gold Trust (GTU) allows for the ability to maintain targeted exposures to both metals in the context of the overall portfolio strategy. It should be noted that I am selectively long stocks within a similar context through positions such as the S&P 500 Low Volatility ETF (SPLV), as well as individual names such as Occidental Petroleum (OXY), McDonald's (MCD), Nike (NKE) and Hormel Foods (HRL).

.

This post is for information purposes only. There are risks involved with investing including loss of principal. Gerring Wealth Management (GWM) makes no explicit or implicit guarantee with respect to performance or the outcome of any investment or projections made by GWM. There is no guarantee that the goals of the strategies discussed by GWM will be met.

0 comments:

Publicar un comentario